This note was originally published at 8am on August 31, 2012 for Hedgeye subscribers.

“Duration neglect is normal in a story, and the ending often defines its character.”

-Daniel Kahneman

That’s one of my favorite risk management quotes from Kahneman’s Thinking, Fast and Slow. It comes from Chapter 36 titled “Life As a Story.” After this morning’s central planning event, take some time to think this weekend. Re-read the last 30 pages of one of the most important books of the year. If there ever was a time to embrace the uncertainty of Behavioral Economics, it’s now.

Storytelling is at the core of everything we do. Storytelling can be personal and political. Storytelling can be short or long-term. But no matter what your confirmation bias or duration, storytelling, at some point, meets a fork in the road between fact and fiction. Whether or not you are proactively prepared for that moment is purely up to you.

Two weeks ago, the Bailout Bull Storytelling was that “Bernanke and Draghi are going to provide a one-two punch in Jackson Hole.” Stock were higher and bonds were lower. Since then: 1. Draghi bagged the meeting, 2. Bernanke’s boys are waffling with “it’s too close to call”, and 3. US Equity Volatility (VIX) is up +34%.

As Ray Dalio likes to say, look in the mirror and ask yourself, “what is true?”

Back to the Global Macro Grind…

The other thing Ray Dalio reminds us (from the Introduction of Ray Dalio’s Principles) is to “above all else, think for yourself.” That’s pretty important when considering what sources are credible in this profession. Many of them have not evolved since 2007.

Duration Neglect is one thing, but being unable to tell the difference between fact and fiction can bankrupt you at the poker table as fast as it can in your personal and professional life. From a Global Macro perspective, no matter what these broken sources tell you this weekend as they live large on your dime in Jackson Hole, Growth Is Slowing.

When I say Growth, I mean Global Growth Data – here it is in the last 48 hours:

- US Jobless Claims rose wk-over-wk to 374,000 vs 366,000 two weeks ago

- US Consumer Confidence fell -8% month-over-month in AUG to 60.6 vs 65.9 in JUL

- Japanese Retail Sales fell -0.8% year-over-year

- Hong Kong Retail Sales volumes dropped from +8.3% year-over-year to +1.3%

- Brazil cut interest rates as inflation ramped +100bps month-over-month to +7.7%

- Spain’s Retail Sales fell -7.3% in JULY (year-over-year) vs -5.2% JUN

- Italy’s unemployment rate ramped to 10.6% in Q2 vs 9.8% in Q1

- Italy’s inflation rate remains at +3.5% in AUG vs +3.6% in JULY (stagflation)

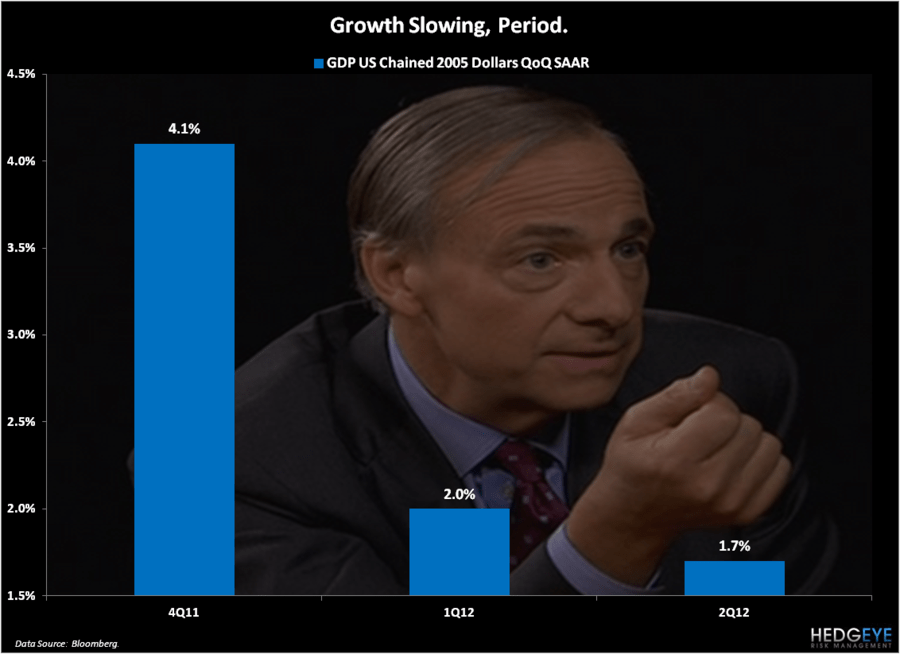

- US GDP Growth for Q212 slowed to 1.73% vs +1.97% in Q112

So, even if you’re still in the “growth is back and earnings are great camp” (Tom Lee, Ed Hyman, Laszlo Birinyi, etc.) from March of 2012 – at this point, if your storytelling is based on the USA alone – you’ve just gotta change your story to begging for bailouts.

To review, the call we made in March of 2012 was that Global Growth Slows As Inflation Accelerates. That, on the margin, is precisely what’s happened here in August versus July – primarily because of the inflation part of that statement. Food and Oil prices matter.

Now if you turn around and tell me that inflation fell in May versus where it was in March, I’ll agree with you. It did. That’s why we bought the SP500 at its long-term TAIL support line of 1283. But, to be consistent, don’t forget what central planning does: A) It Shortens Economic Cycles and B) Amplifies Market Volatility. So you have to keep moving.

Back to that US GDP Growth print this week of 1.73%:

- It implied a “Deflator” of 1.59% in Q2 versus +2.16% in Q1; therefore GDP, inflation adjusted, was overstated in Q2

- Assuming inflation is the same as the government says it was in Q1 here in Q3 (it’s higher), #GrowthSlowing continues

- Irrespective of the storytelling on what inflation rate you use, US GDP is down -57.8% from Q411 to Q2 of 2012

In this No Trust; No Volume market, one of the most neglected long-term issues remains confidence. Small business owners in America like me aren’t morons. We aren’t going to ramp Fixed Investment growth, Inventories, and Hiring into a central planning event.

That’s not me telling my own story – the only inventory I have in oversupply are tweets. That’s the story within the latest US GDP report:

- US Fixed Investment Growth was basically cut in half, sequentially, from Q1 to Q2 (+0.63% vs +1.18%)

- US Inventory Growth went from +2.53% in Q411 (when Growth was solid) to -0.23% in Q212

- US Export-Import Growth (+0.3% in Q212) remains nowhere to be found as an offset to 1 and 2

Keynesian Quacks will tell you that if you debauch the currency of a nation, “exports will ramp” and a bunch of other stuff will multiply upon that as Ben Bernanke and Larry Summers raise the oceans to escape velocity.

Not true.

Not this time. No dear Sirs; this time is not different. This story will have an ending - and your Duration Neglect will be the cross of the families bearing your name for many years to come.

My immediate-term support and resistance ranges for Gold, Oil (Brent), US Dollar, EUR/USD, 10yr UST Yield, and the SP500 are now $1627-1679, $111.12-113.74, $81.11-82.18, $1.23-1.26, 1.56-1.65%, and 1397-1409, respectively.

Enjoy your long weekend,

KM

Keith R. McCullough

Chief Executive Officer