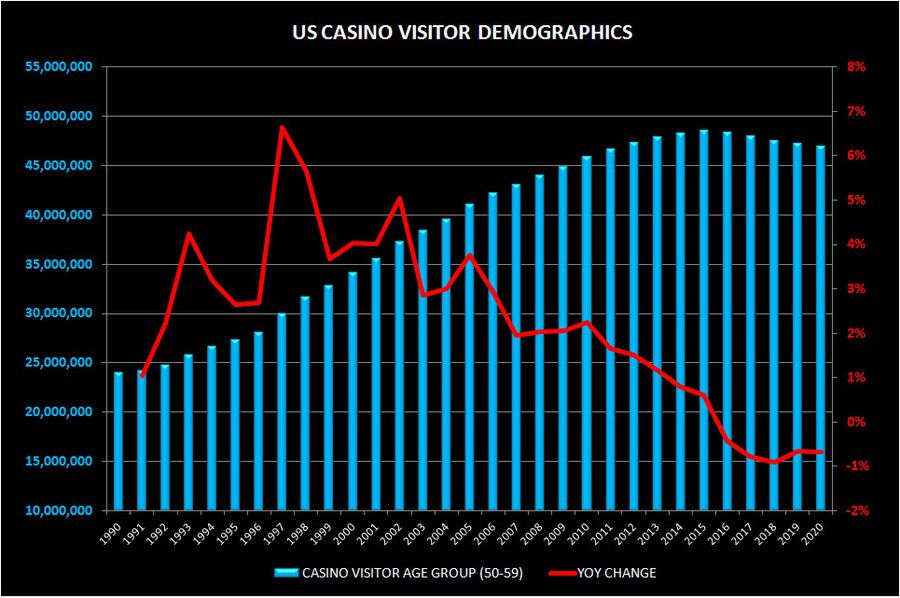

- The core age group for domestic gaming visitors has been 50 to 59 years old. The baby boomer generation caused this group to grow rapidly until 2003.

- The rate of growth was consistent between 2007 and 2010 but began a sharp downward trend. The absolute population in this segment may actually fall in 2016.

- Compounding the demographic issue is the fact that younger generations are not embracing the slot machine