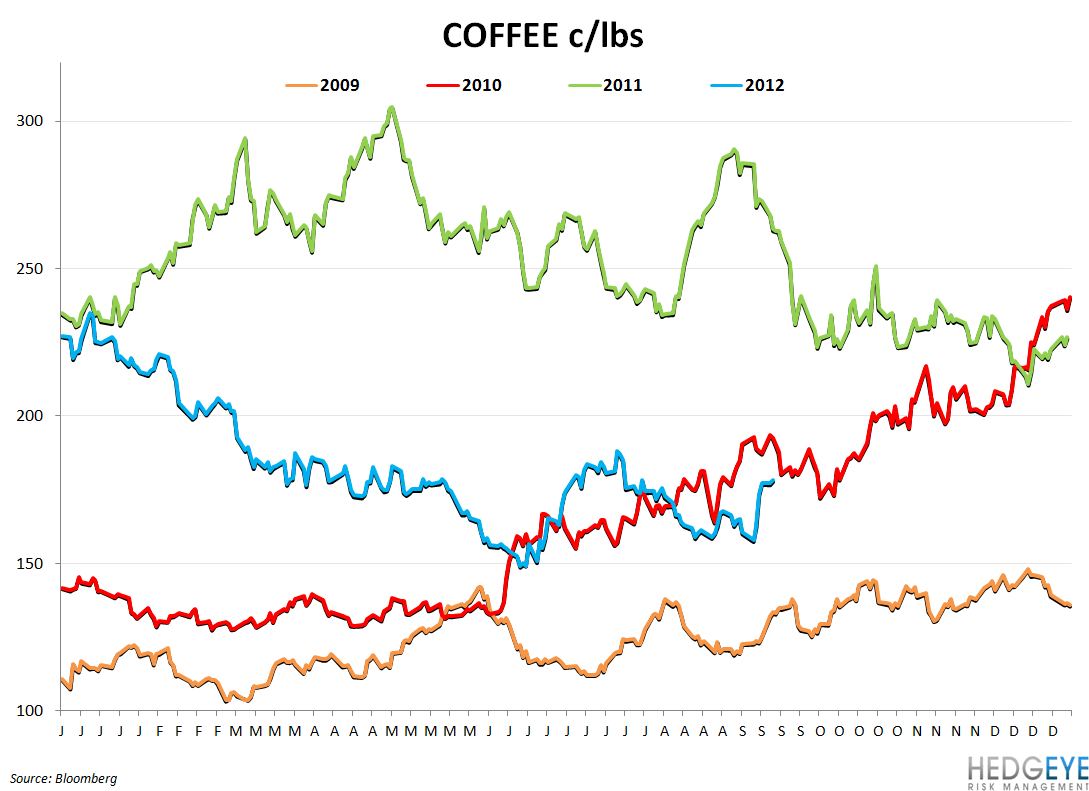

Corn dropped over the last week but beef retained the limelight as prices gained another 1.2%. Coffee prices snapped higher as speculation grew that Columbia’s Arabica harvest is likely to come up short versus growers’ expectations. We do not view this as overly material for the coffee retailer stocks given that prices are still down 33% versus last year. Chicken wings moved slightly lower to +103% year-over-year.

The last week has been mixed for commodity prices but today’s Fed announcement is likely to sustain the volatility in commodity markets that have made life difficult for investors, analysts, and company executives alike. As the chart below indicates, the CRB Foodstuffs Index turned sharply higher during the implementation of both prior rounds of quantitative easing. While there are different schools of thought on the relationship, or lack thereof, between monetary policy and commodity prices, and other factors such as drought clearly have an impact. As long as interest rates are artificially pushed lower, and QE3 seems likely to have that effect, investors will speculatively seek yield in alternative asset classes such as commodities. Joe Sanderson, CEO of SAFM, and others have noted Federal Reserve intervention have had an impact on commodity markets.

Summary View

The USDA World Agricultural Supply & Demand (WASDE) report was released yesterday and there were some surprises.

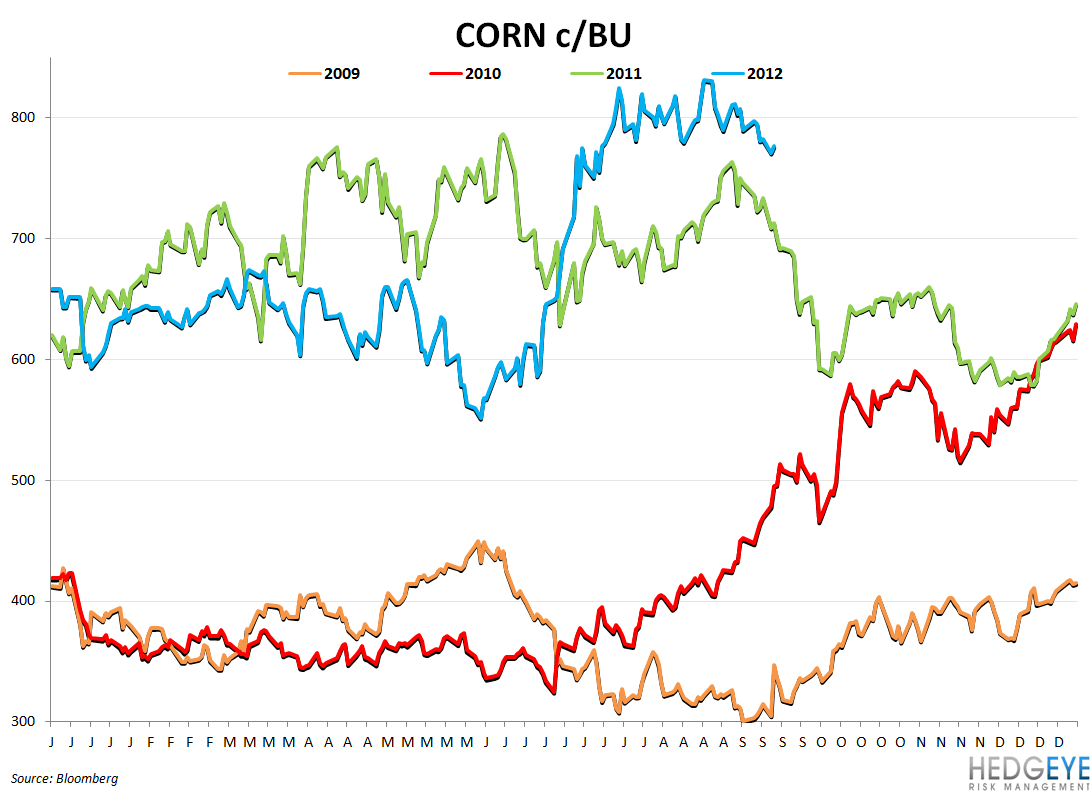

- Corn declined yesterday as the USDA unexpectedly raised its corn ending stock forecast to 733 million bushels from 650 million prior. Lower production and yield were offset by higher beginning stocks. We believe that a slowing in consumption, as well as the market anticipating more drought damage to the crop than seems to have materialized, was behind the move lower

- Wheat supply and consumption estimates were unchanged for the current U.S. marketing year.

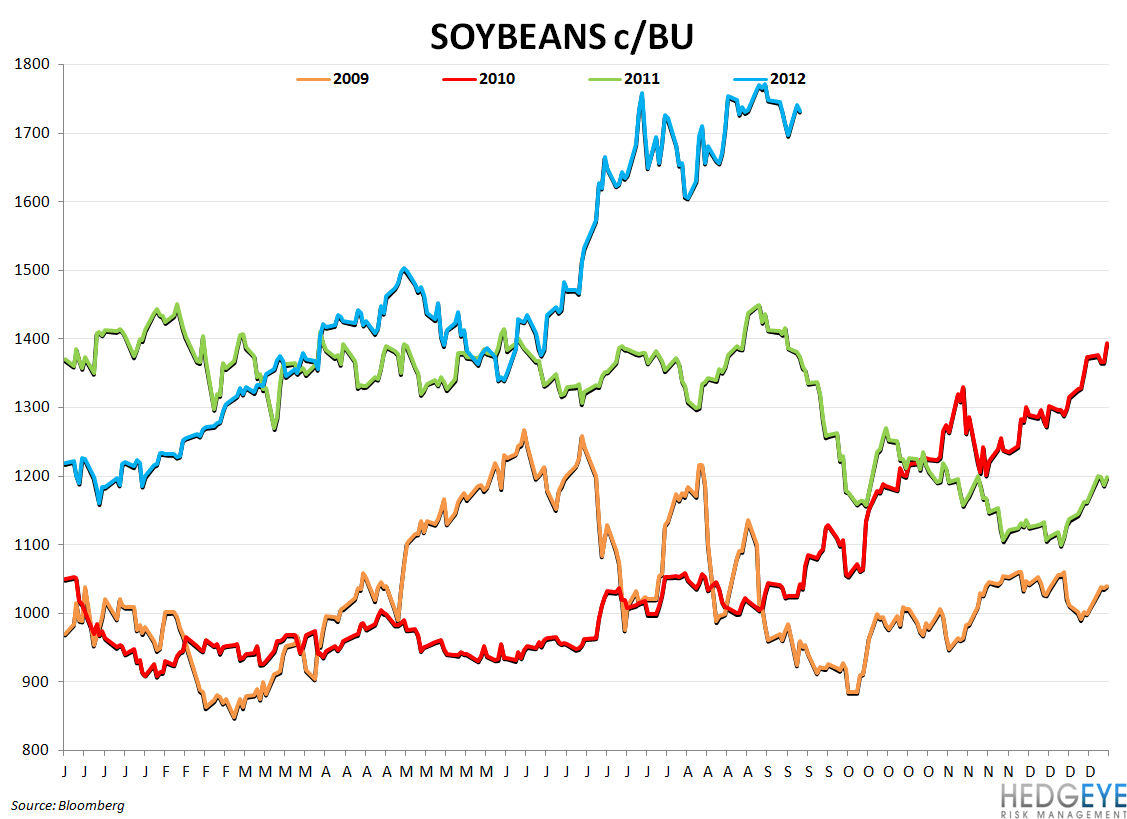

- The 2011/2012 marketing year estimate of U.S. exports of soybeans was increased by 10 million bushels

Coffee prices gained 13.1% week-over-week as speculation grew that Columbia’s Arabica harvest is likely to come up short versus growers’ expectations. Coffee prices are still down 33% from year-ago levels and the outlook remains favorable for PEET, SBUX, GMCR and other coffee retailers from a cost of sales perspective.

Beef prices gained over the last week and U.S. Meat Export Federation President and CEO Philip Seng had the following to say: “With higher operating costs, the beef sector is facing serious economic challenges. Tight beef supplies have pushed prices higher and strong demand from our international customers is helping support higher beef cutout values. With these factors in mind, it is absolutely critical that we remain aggressive with our international promotions and continue to capture the highest return possible on the products we export.” Beef price gaining is a negative for WEN (20% of spend), BLMN (30%), and JACK (20%).

Drought is undoubtedly still an issue in several areas of the world, including the U.S., but the USDA’s -1% corn output revision was much less dramatic than feared. That said, the drought is nearing its fourth month

Macro Callout

Gasoline prices continue to head higher. As Hedgeye CEO Keith McCullough has been pointing out – particularly in light of QE3 today – gas prices north of $4 have had a destructive impact on consumption (71% of U.S. GDP) in 2008, 2011, and in 1Q12.

Correlation

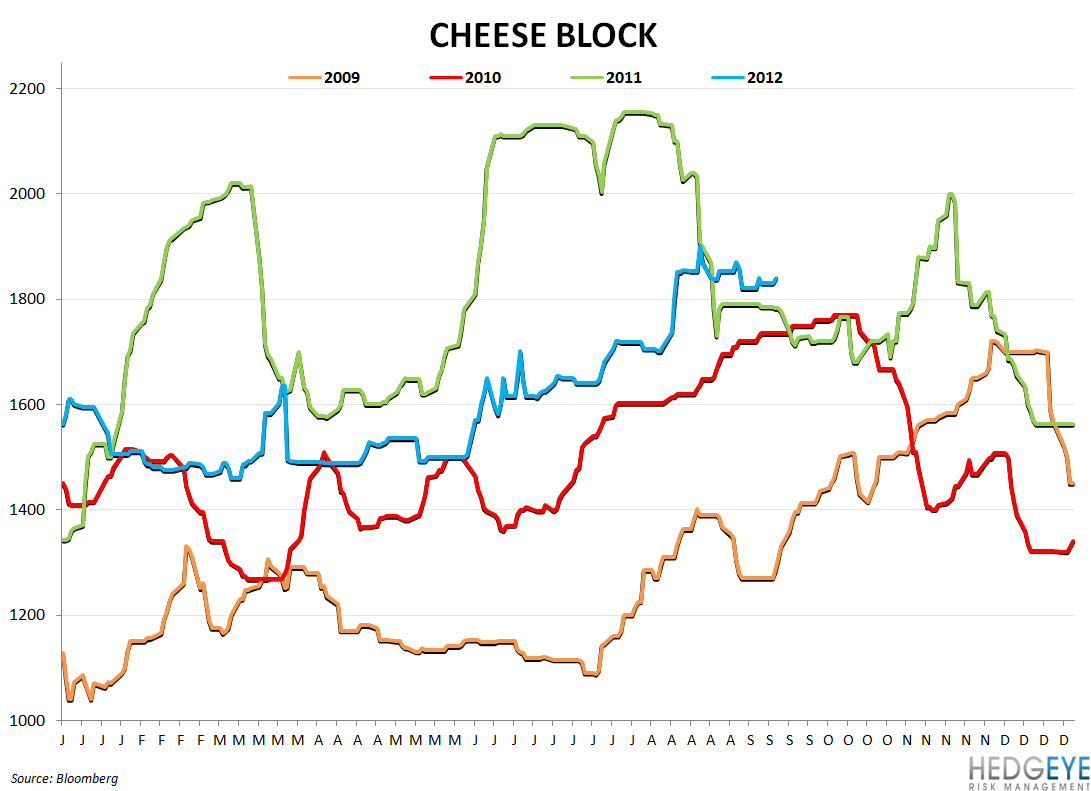

Charts

Howard Penney

Managing Director

Rory Green

Analyst