THE HEDGEYE DAILY OUTLOOK

TODAY’S S&P 500 SET-UP – September 11, 2012

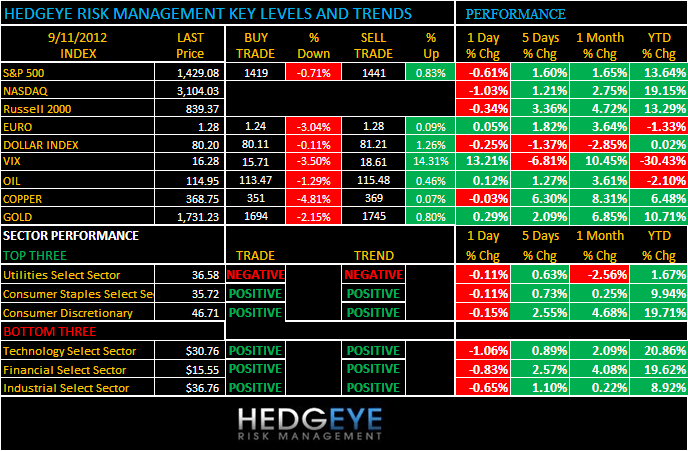

As we look at today’s set up for the S&P 500, the range is 22 points or -0.71% downside to 1419 and 0.83% upside to 1441.

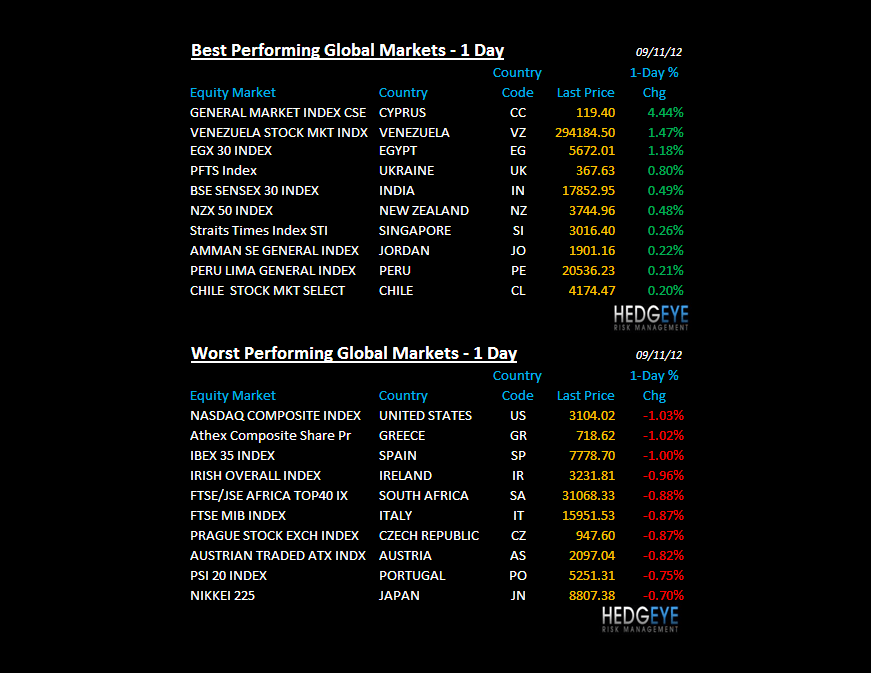

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: on 09/10 NYSE -613

- Decrease versus the prior day’s trading of 1083

- VOLUME: on 09/10 NYSE 616.08

- Decrease versus prior day’s trading of -9.39%

- VIX: as of 09/10 was at 16.28

- Increase versus most recent day’s trading of -13.21%

- Year-to-date decrease of -30.43%

- SPX PUT/CALL RATIO: as of 09/10 closed at 1.61

- Down from the day prior at 1.82

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: as of this morning 30.79

- 3-MONTH T-BILL YIELD: as of this morning 0.10%

- 10-Year: as of this morning 1.67%

- Increase from prior day’s trading of 1.65%

- YIELD CURVE: as of this morning 1.43

- Up from prior day’s trading at 1.41

MACRO DATA POINTS (Bloomberg Estimates)

- 7:30am: NFIB Small Business Optimism Index, Aug., est. 91.4 (prior 91.2)

- 7:30am/8:45am: ICSC/Redbook weekly sales

- 8:30am: Trade Balance, July, est. -$44.0b (prior -$42.9b)

- 10am: IBD/TIPP Economic Optimism, Sept., est. 46.4 (prior 45.6)

- 10am: JOLTs Job Openings, July, est. 3.740m (prior 3.762m)

- 11am: Fed to buy $1.5b-2b notes due 2/15/2036-8/15/2042

- 11:30am: U.S.to sell $40b 4-wk bills

- 1pm: U.S. to sell $32b 3-yr notes

- 4:30pm: API inventories

GOVERNMENT:

- House, Senate in session

- Senate Foreign Relations marks up bills including “Increasing American Jobs Through Greater Exports to Africa Act”

- House Oversight holds hearing on Operation Fast and Furious, 9:30am

- House Energy panel holds hearing on anti-terrorism standards for chemical facilities, 10am

- House Energy panel meets on H.R.4255, the “Accountability in Grants Act,” 10:15am

- House Natural Resources holds hearing on electricity costs, 11:30am

- House Financial Services panel holds hearing on terrorism risk insurance program, 10am

- House Ways and Means holds hearing on IRS implementation, administration of health-care law, 10am

- House Transportation holds hearing on Amtrak passenger rail service monopoly, competition with regional services, 10am

- American Institute of Certified Public Accountants holds its National Conference on Banks and Savings Institutions, with speakers including Fed Chief Accountant Steven Merriett; Office of Comptroller of the Currency Chief Accountant Kathy Murphy; and FDIC Chief Accountant Robert Storch, 9:55am

WHAT TO WATCH:

- AIG shrs valued at $18b - ~553.8m shrs at $32.50 each - sold by U.S., converting 4-year bailout into profit for taxpayers

- Morgan Stanley won dispute with Citigroup over value of Smith Barney, of which it owns 51%: N.Y. Post

- U.S. trade deficit probably grew to $44b in July from $42.9m

- Texas Instruments releases mid-qtr update post-mkt

- Samsung’s request for judge to lift prelim. ban on U.S. sales of its Galaxy Tab 10.1 tablet computer opposed by Apple

- HarperCollins reached agreement with Amazon, other e- commerce cos. that results in lower prices for electronic books

- Glencore still waiting for decision from Qatar Holding on whether it will support takeover of Xstrata

- General Growth rejected investor Bill Ackman’s call to put itself up for sale, said it plans to remain independent

- Apple may sell as many as 10m redesigned iPhones by end of Sept. according to Piper Jaffray’s Gene Munster; expected to introduce new phone tomorrow

- Burberry said full-year profit will disappoint amid more “challenging” environment; European luxury cos. drop

- Infosys unit to buy Marsh & McLennan unit in India: WSJ

- Assured Guaranty dodged downgrade as Moody’s failed to meet deadline, according to shareholder Wilbur Ross

- Hiring plans among U.S. corps in 4Q little changed from previous 3 mos, ManpowerGroup said in employment index

EARNINGS:

- United Natural Foods (UNFI) 7:30am, $0.51

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

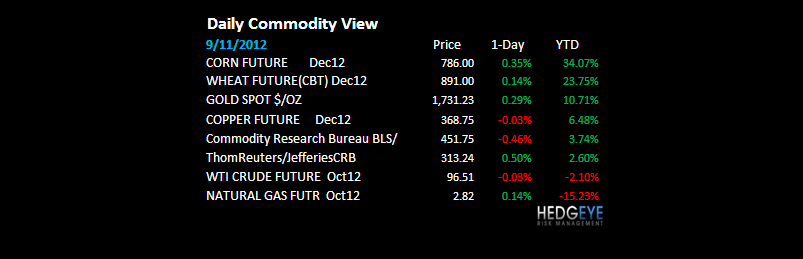

OIL – so, Oil is only up +31% in basically a straight line since mid-June, and Bernanke will say there’s no inflation this wk; w/ unemployment and median incomes remaining a disaster, this is one of the biggest tragedies of the Qe experiment; what’s good for the few (stock market) is bad for the many (real-inflation adjusted consumption growth).

- Soy Reserves Smallest in Four Decades After Drought: Commodities

- Nuclear Repairs No Easy Sale as Cheap Gas Hits Utilities: Energy

- Oil Supplies Fall to Five-Month Low in Survey: Energy Markets

- Oil Trades Near Three-Week High on Outlook for Economic Stimulus

- Corn Advances as Harvest Progress in U.S. Confirms Crop Damage

- Copper Seen Declining on Speculation Two-Day Rally Was Overdone

- Gold Advances on Outlook for Further Stimulus at Fed Meeting

- Robusta Coffee Tracks Arabica as Investors Buy; Cocoa Advances

- OPEC Sees ‘Abundant’ Oil Supply, May Cut 2013 Demand Estimates

- Qatar Holds Out on Glencore Bid as Davis Heads for Xstrata Exit

- Chemical-Tankers Seen Rallying 50% as Fleet Proves Busy: Freight

- Sugar to Pile Up as Global Demand Stays Weak, Kingsman Says

- Russia Volumes, LNG Cargoes to Weigh on Gas to 2013, SocGen Says

- Talisman CEO Switch Speeds Up Sale Speculation: Corporate Canada

- India’s Goa Bans Mining After Panel Pegs Loss at $6.3 Billion

- German Next-Month Power Falls Before Court Ruling on Euro Fund

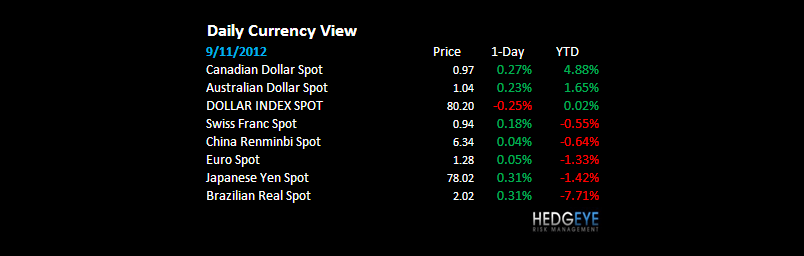

CURRENCIES

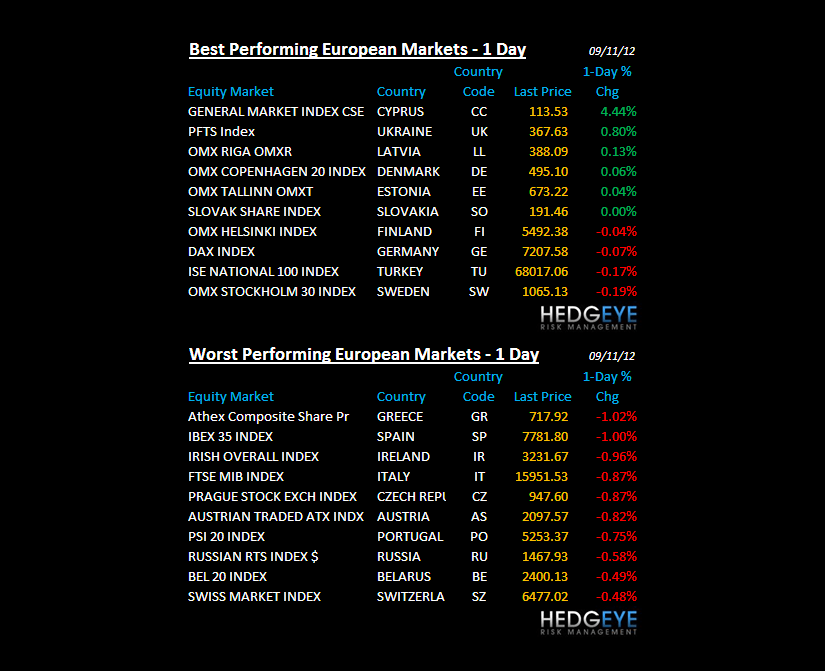

EUROPEAN MARKETS

SPAIN – not clear what Rajoy was thinking by telling the truth, but Spain is now on the tape opposing bailout conditions; that’s good for another lower-high (since March) in Spanish Equities (and the Eurostoxx50); $1.28 Euro isn’t good for German exports either.

ASIAN MARKETS

ASIA – USD down is all good and fine for short-term politics (Bush did the same using Bernanke), but it’s bad for the rest of the world via commodity inflation; this continues to slow Asian growth and you can see that in the 2 big Asian Equity markets (China and Japan) that continued lower last night (-0.7%) after their 2-day squeeze.

MIDDLE EAST

The Hedgeye Macro Team