McDonald’s reports August sales results tomorrow morning before the market open. Global growth slowing is still the primary headwind for MCD but we expect sequentially better comparable store sales, at least in the United States.

We wrote on April 24th that we saw “plenty to be concerned about” regarding the outlook for McDonald’s sales trends. Macroeconomic factors remain a headwind for the company. The company’s value proposition in the U.S., relative to the competition, is less compelling in 2012 than it was in 2011 with price – at roughly 3% – in line with Food Away from Home CPI versus last year when the spread was roughly -50 basis points. We believe that MCD is closer to the bottom than the top, but are looking for catalysts before become vocal on the long side.

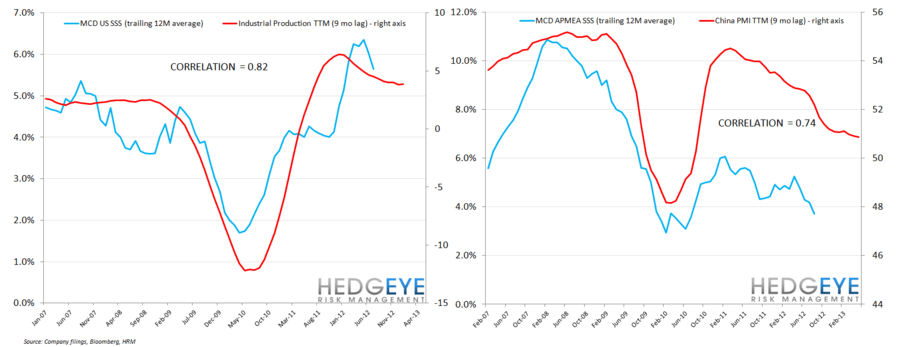

Macro Growth Slowing Matters

Growth continuing to slow in Asia, Europe, and the U.S. is a headwind for MCD sales growth. Europe is more difficult to calibrate since it is difficult to know which market will drive a beat or miss in any given month. China seems to be a decent proxy for APMEA which is not entirely surprising given its importance for global and regional growth.

Sales Preview

Below we go through what we would view as good, bad, or neutral comparable restaurant sales numbers for McDonald’s three regions. For comparison purposes, we have adjusted for historical calendar and trading day impacts (but not weather).

Compared to August 2011, August 2012 had one less Monday and Tuesday and one additional Thursday and Friday. In addition, Ramadan ended on August 18th, 2012, versus August 30th, 2011. This will have a positive impact on August 2012's numbers.

U.S. – facing a compare of 3.9%, including a calendar shift of between 0.0% and -0.7%, varying by area of the world.

GOOD: A print above 3.5% would be received as good by investors as it would imply calendar-adjusted two-year average comparable store sales above the trend in July. Last month, McDonald’s traffic was negative and investors will be looking for a clear signal that this was merely a one-off and not part of a trend. We are anticipating a print of 3% for MCD U.S. in August.

NEUTRAL: Same-restaurant sales growth of between 2.5% and 3.5% would be received as neutral by investors as it would imply calendar-adjusted two-year average comparable restaurant sales growth roughly level with trends in July. This is a difficult quarter to measure on a sequential basis given the Ramadan shift but we believe that investors are not anticipating a sequentially worse headline, even excluding the benefit in August from Ramadan.

BAD: A print below 2.5% would imply calendar-adjusted two-year average comparable restaurant sales growth below the trend from July. Given the disappointment that July’s results brought for McDonald’s investors, a deceleration in underlying trends on a sequential basis would be decidedly negative for the stock.

Europe – facing a compare of 2.7%, including a calendar shift of between 0.0% and -0.7%, varying by area of the world.

GOOD: A same-restaurant sales number in excess of 4% would be considered a strong result because it would imply, on a calendar-adjusted basis, two-year average trends showing stabilization after several months of volatility. We are expecting a print of 3.6% for MCD Europe in August. We expect the Olympics to have provided a year-over-year boost to sales in some markets like the U.K., which have been driving the Europe division in recent months.

NEUTRAL: 3-4% would be a neutral result for Europe as it would imply trends roughly in line with expectations and, following a negative print in July, would provide some reassurance of MCD’s ability to take share on an ongoing basis.

BAD: A print below 3% would imply a significant sequential deceleration in calendar-adjusted, two year average trends and, possibly, negative calendar-adjusted comparable sales growth.

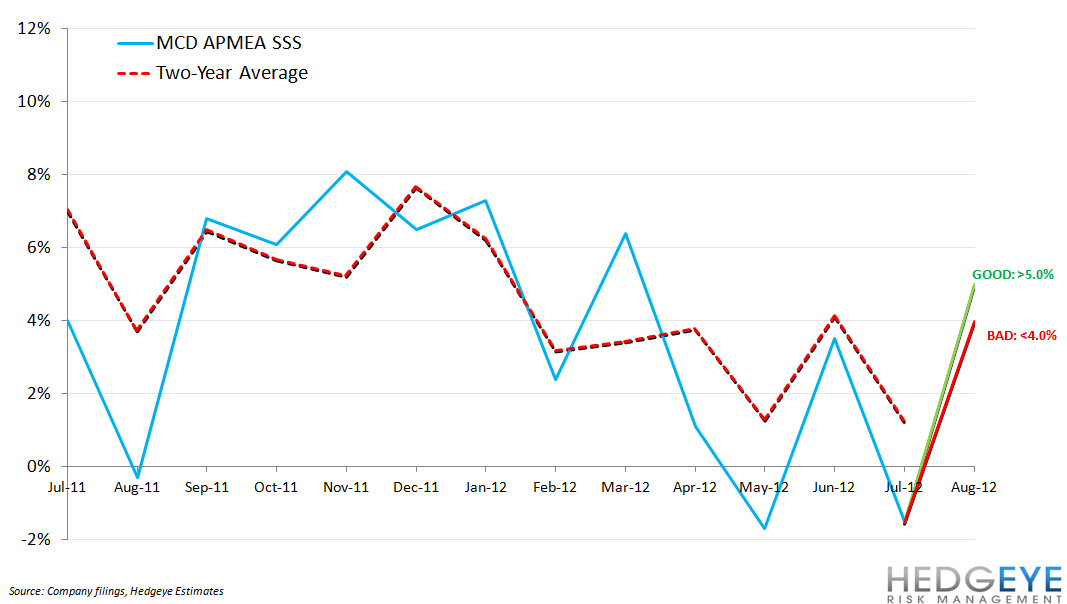

APMEA – facing a compare of -0.3%, including a calendar shift of between 0.0% and -0.7%, varying by area of the world.

GOOD: Same-restaurants sales growth of 5% or more would be received as a good result as it would imply calendar-adjusted two-year average trends roughly flat versus July. The trend in APMEA comps has been bearish over the last few months and any stabilization would likely be well-received. On July 23rd, management cited weakness in Japan and consumer caution in China, particularly in tier-one cities where McDonald’s stores are most heavily concentrated.

NEUTRAL: A print between 4% and 5% would be considered neutral for investors as it would be roughly in line with consensus, per Consensus Metrix.

BAD: Below 4% would imply a sequential deceleration in calendar-adjusted two-year average trends from June to July. This would be severely bearish as it would imply a sharper deceleration from July to August than there was from June to July.

Howard Penney

Managing Director

Rory Green

Analyst