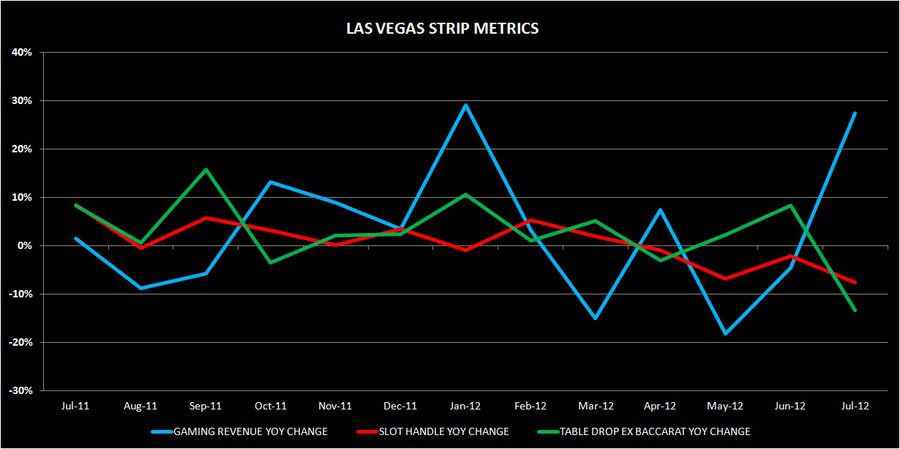

- In our 9/4/12 note, “LV STRIP: JULY DECEPTION” we had projected a strong headline revenue growth rate of high teens for July due to low slot and table hold last year – actual Strip gaming revenues grew 27% with an additional boost from very high baccarat hold and better baccarat volume

- The important metrics – slot volume and ex baccarat table drop – fell 7% and 13%, respectively. This was actually worse than our projection of -3% and -2%, respectively. Two fewer weekend days versus last year did play a role but the numbers were still bad.

- July represented the 4th consecutive month of slot volume declines. For tables, July was the worst monthly decline for non-baccarat drop since August 2009.