“The first definition of victory is survival.”

-Hampton Sides

Tops are processes, not points. From both an intermediate and long-term perspective, at least that’s what we have learned in the last 5 years. Big Central Planning in what used to be “free-markets” continues to A) shorten economic cycles and B) amplify price volatility.

“But, Keith, the market is up year-to-date.” Yep. And the SP500 was up double-digits for the year-to-date on October 9th, 2007 too (1565 for those of you who still remember that cost basis and the people who told you to buy there). Just think, only 18 months later you could have bought Starbucks $SBUX at $11 (i.e. 78% lower). That’s when stocks were “cheap.”

Cheap is as cheap does. People get that. How else can you explain money flowing out of Equity funds in the latest Lipper data (-$6.8B in outflows last week)? People also remember late 2007 and all the storytelling about growth recovering via centrally planned “shock and awe” rate cuts back then too. I never thought we’d get back to that same sell-side narrative. Never say never, I guess.

Back to the Global Macro Grind…

The aforementioned quote is the last one I wanted to highlight from this summer’s reading about the founding of the 19th century American West (page 469 in Blood and Thunder). It was a creed Kit Carson lived by. And it’s one I’ve embraced as a Risk Manager of my own capital too. Spending 5 years of your life trying to get your investors’ capital back to break-even is no life to live.

Getting back to break-even is another way to think about why I am constantly measuring LOWER-HIGHS across intermediate to long-term investing cycles. Those define memory, losses, and pain. If you have a friend who bought the 2007 top in the SP500, he only has another +10% higher to go (from here) to get back to his high-water mark. I hope he didn’t use leverage.

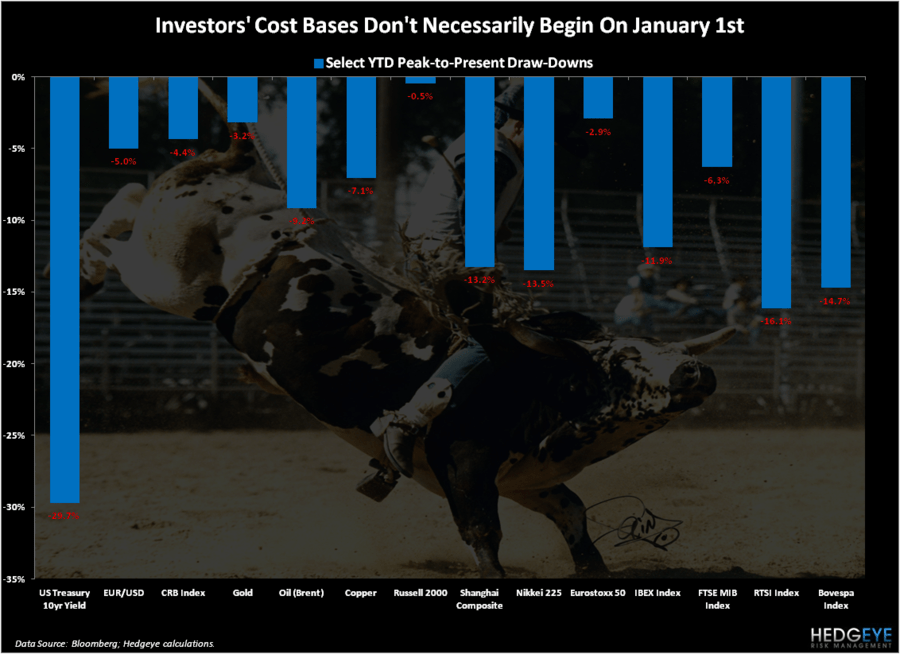

Across intermediate-term durations (since February-March 2012), here are some LOWER-HIGHS to think about (across asset classes):

- US Treasury Bond Yields (10yr) = 1.66% (down from 2.4% in March 2012)

- EUR/USD = $1.27 (down -5.2% from March 2012)

- CRB Commodities Index = 311 (down -4.4% from March 2012)

- Gold = $1736 (down -3.2% from February 2012)

- Oil (Brent) = $115 (down -9.2% from March 2012)

- Copper = $3.69 (down -7.1% from February 2012)

- Russell2000 = 842 (down from 846 on March 26th,2012)

- Chinese Stocks (Shanghai Composite) = 2134 (down -13.2% from March 2012)

- Japanese Stocks (Nikkei225) = 8869 (down -13.5% from March 2012)

- European Stocks (Eurostoxx50) = 2533 (down -2.9% from March 2012)

- Spanish Stocks (IBEX) = 7861 (down -11.9% from March 2012)

- Italian Stocks (MIB) = 16,050 (down -6.3% from March 2012)

- Russian Stocks (RTSI) = 1468 (down -16.2% from March 2012)

- Brazilian Stocks (Bovespa) = 58,321 (down -14.7% from March 2012)

In other words, if you bought any of these asset classes and went short and/or “underweight” Treasury Bonds, you are underwater since Growth Slowing began to be obvious, globally in March of 2012. That side of the research call has been dead on.

Are there any outliers?

- SP500 = 1437 (up +1.3% from March 2012)

- German Stocks (DAX) = 7217 (up +0.8% from March 2012)

- US Equity Volatility (VIX) = 14.38 (up +0.8% from March 2012)

Hoowah, what a return versus the risk you had to take! (*note: SPX and RUT had 10 and 13% draw-downs from March to June)

To be fair to the “growth is back, earnings are great, and stocks are cheap” bull crowd of economists (rewind the tapes and/or read their Feb/Mar 2012 research), Venezuelan, Egyptian, and Pakistani stocks are right ripping since March 2012. So bullish.

But let’s not fuss about the details on why “the market is up-year-to-date” (Bernanke doing Qe3 on January 25th, pushing 0% rates to 2014; and the market baking in a Qe4 or push for 0% rates to 2015 now)…

Let’s not talk about the real-time P&L impact of this little detail called timing in anything pro-cyclical since March. The very same economists and Old Wall Street strategists weren’t fussing about it in September-October of 2007 either.

This isn’t my 1st rodeo with perma-bulls. They are loud and they change their thesis to suit last market price. That’s why Surviving Tops isn’t easy. Particularly when the storytelling, groupthink, and performance chasing is coming on thick.

My immediate-term support and resistance risk ranges for Gold, Oil (Brent), US Dollar Index, EUR/USD, 10yr US Treasury Yield, and SP500 are now $1, $113.39-115.02, $80.11-81.29, $1.24-1.28, 1.56-1.70%, and 1, respectively.

Best of luck out there this week,

KM

Keith R. McCullough

Chief Executive Officer