-- For specific questions on anything Europe, please contact me at to set up a call.

Positions in Europe: Long German Bonds (BUNL); Short EUR/USD (FXE); Short Greece (GREK)

Asset Class Performance:

- Equities: The STOXX Europe 600 closed up +2.3% week-over-week vs -0.7% last week. Top performers: Cyprus +10.8%; Greece +7.2%; Italy +6.7%; Spain +6.2%; Portugal +5.6%; Austria +5.0%; Russia (RTSI) +4.6%. Bottom performers: Ukraine -3.3%; Slovakia -0.5% [Other: Germany +3.5%; France +3.1%; UK +1.5%].

- FX: The EUR/USD is up +1.72% week-over-week versus +0.56% last week. W/W Divergences: PLN/EUR +1.75%; CZK/EUR +1.21%; RUB/EUR +0.37%; DKK/EUR 0.00%; HUF/EUR -0.25%; TRY/EUR -0.54%; SEK/EUR -1.49%.

- Fixed Income: The 10YR yield for sovereigns fell dramatically across the board for peripheral countries, while the core gained on the week. Greece saw the largest decline, -181bps to 21.62%, followed by Portugal’s -116bps move to 8.25% and Spain fell -95bps to 5.75bps. Germany was up +23bps to 1.62% and France gained +5bps to 2.24%.

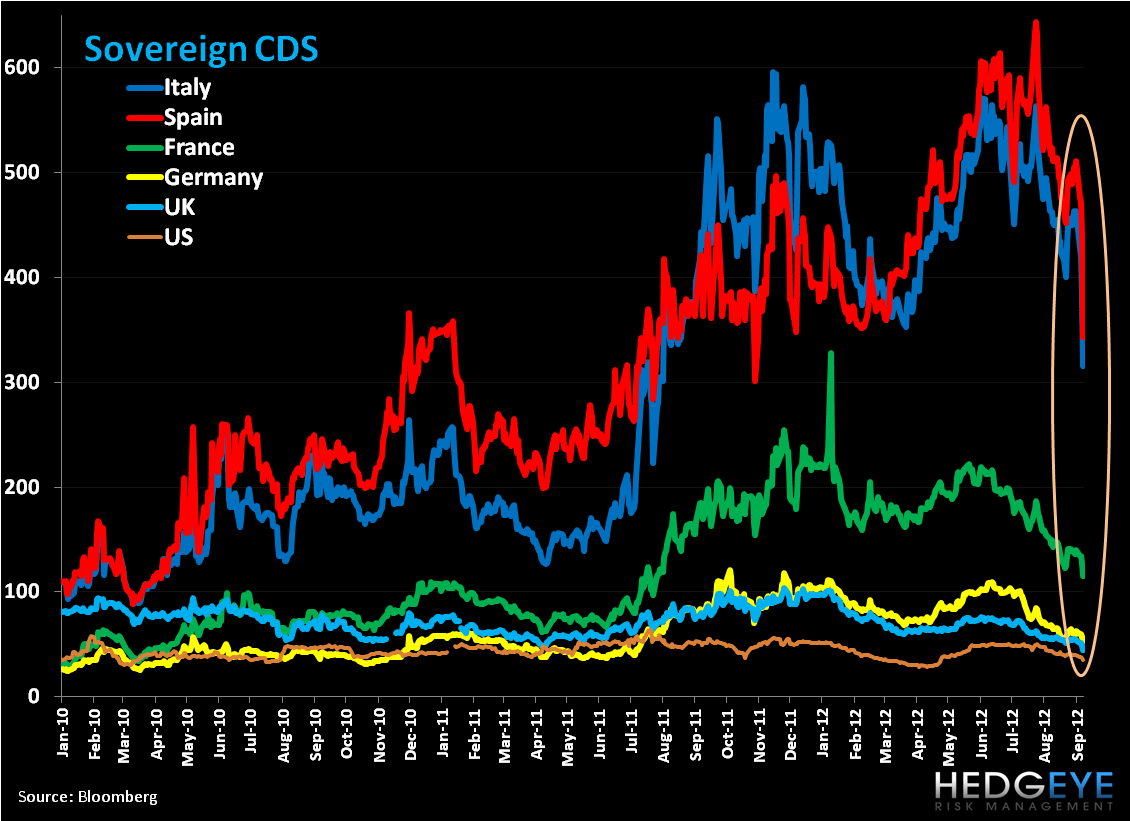

- Sovereign CDS: Sovereign CDS followed yields with all main countries we track down on the week. On a week-over-week basis Spain fell the most, down -168bps to 343bps, followed by Italy -148bps to 315bps, Portugal -133bps to 536bps, Ireland -97bps to 343bps, and France -25bps to 115bps.

Buying Time

This week was all about Draghi’s issuance of the newly invented Outright Monetary Transactions (OMTs) program to buy unlimited bonds on the secondary market of Eurozone member states, targeting maturities of 1-3 years. He announced OMTs Thursday morning following the ECB’s decision to keep the main rates on hold, however, most of the details of OMT were leaked on Wednesday during the trading session, so the back half of the week saw significant gains across European capital markets, with positive divergence from the periphery.

Sizing up Draghi’s newest “Blank Check” is difficult – while the market continues to beg for more central bank and state-backed interventions and bailouts, fundamentals remain severely challenged and the feasibility of a Union of uneven states is still very much in question. Spain and Italy, which we’re previously written about, remain hot spots of sovereign and banking risk that we believe will take wind out of the short term optimism sails of this week’s OMTs announcement.

Of note is that Spain has a hefty level of debt maturing in October, namely €35.316B of principal and interest coming due, or 59% of the €59.212B in principal and interest due into the remainder of the year. As PM Mariano Rajoy struggles to issue austerity and cut the deficit (which we expect Spain to miss rather dramatically versus 8.9% of GDP last year) and the means by which its banking system is bailed out (ESM or EFSF and through the FBOR or not) remain unclear, a powder keg of risk is developing on already bombed out fundamentals: GDP in firmly negative territory (-1.3% in Q2 Y/Y); unemployment rate is near 25% (over 50% for youth); we expect rising debt levels; and there are potentially more downgrades from the main ratings agencies to come (for more see our note titled “Idea Alert: Shorting Spain” from 9/4).

Our two grave concerns in Europe broadly are the lack of growth and inability of Eurocrats to construct a functional fiscal union. On growth we’re worried that the periphery will have to continue to revise down its estimates [note that the ECB revised down its GDP estimate in Thursday’s meeting—versus staff projections in June—to -0.6% and -0.2% for 2012 (versus -0.5% and 0.3%) and -0.4% and 1.4% for 2013 (versus 0.0% and 2.0%)] and the core (namely Germany) will not be able to pick up the slack and/or will also underperform estimates.

On a fiscal union, we continue to reiterate that Europe must have a fiscal union alongside its current monetary union to reign in and regulate budgets as well manage the imbalance that has resulted from highly uneven economies (or differentials by way export/import; infrastructure; population size; natural resources; and know how). However, getting to a fiscal union will take a huge step given the inability of member states to relinquish their sovereignty to Brussels (and/or Frankfurt). To be sure, getting to a fiscal union is complicated by the cultural differences (language in particular) that divide nations and prevent loose conditions to work in states outside of one’s home country.

In short, while the OMTs will “benefit” yields, especially from the periphery and towards the shorter end of the curve, artificial support (sovereign buying) and flooding the system with liquidity is not going to solve Europe’s problems. And growth, for sure, will remain under pressure (see PMIs for August below under Data Dump).

The week ahead offers two big catalysts, namely the German Constitutional Court’s decision on the ESM (with a banking license) and the Fiscal Union. Interestingly, Reuters reported that all 20 public and constitutional law professors it surveyed predicted that the court will approve the ESM and fiscal compact. However, twelve professors noted that approval is likely to come with tough conditions limiting the government's flexibility on any new rescues. In addition, five said that the court is likely to signal that Eurozone integration has reached the limits permitted by the constitution, suggesting the potential for a public referendum.

A second catalyst to watch is the Dutch General Election. Currently two pro-European political parties lead polls: Prime Minister Mark Rutte's Liberal Party followed closely by the Labor Party, which is pro-euro but unlike the Liberal Party, opposes tough austerity measures. The two parties could form a center-right coalition with the support of just one other party, potentially the socially liberal D66 Party. Worth noting is the waning support for the Socialists who were previously polling high and who oppose deeper Eurozone integration, as well as the decline in the Freedom Party, which has pushed for an exit from the euro and a return to the guilder.

Call Outs:

Spain - even after the ECB unveiled the details of its new intervention plan, Spanish Prime Minister Rajoy continued to push back against calls to make an official request for support. He also signaled his reluctance to accept new conditions that could be attached to additional external support, pointing out that he had no intention of touching Spanish pensions. One senior EU official said he saw a Spanish aid request around the time of the October 18-19 leaders' summit as a "best-case scenario".

France - CAC 40 changes: Peugeot to be replaced by Solvay (changes to take effect on September 24)

Moody’s - cut its EU outlook to negative to reflect risks to Aaa of Germany, France, UK, and Netherlands.

France - LVMH chairman being hauled in front of the French PM to defend their decision to move 200 top managers to New York due to the new 75% top tax rate on pay > €1 million.

Germany - missed its target of €5B and only sold €3.61B of new 1.5% 10YR bonds, average yield 1.42% [Bid-cover ratio 1.1 vs previous 1.8]

Germany - A poll from Forsa for Stern magazine (a German publication) found 30% of respondents said that they had little trust in ECB President Draghi, while 12% noted that they had none at all. Roughly 18% said that they held him in esteem, while 31% said that they did not know him and 9% had no opinion at all. Recall that German Chancellor Merkel has blessed the ECB's intervention plan as a bridge to her preferred longer-term solution to address the debt crisis: deeper fiscal and political integration.

EUR/USD:

Our immediate term TRADE range for the cross is $1.24 to $1.26. The move above our resistance level is a reflection of optimism around the OMTs program. We expect the cross to come in after this initial optimism. Please see my colleague Daryl Jones’ note today titled “Is the Move in the Euro More Than A Short Squeeze?” for more thoughts on the cross.

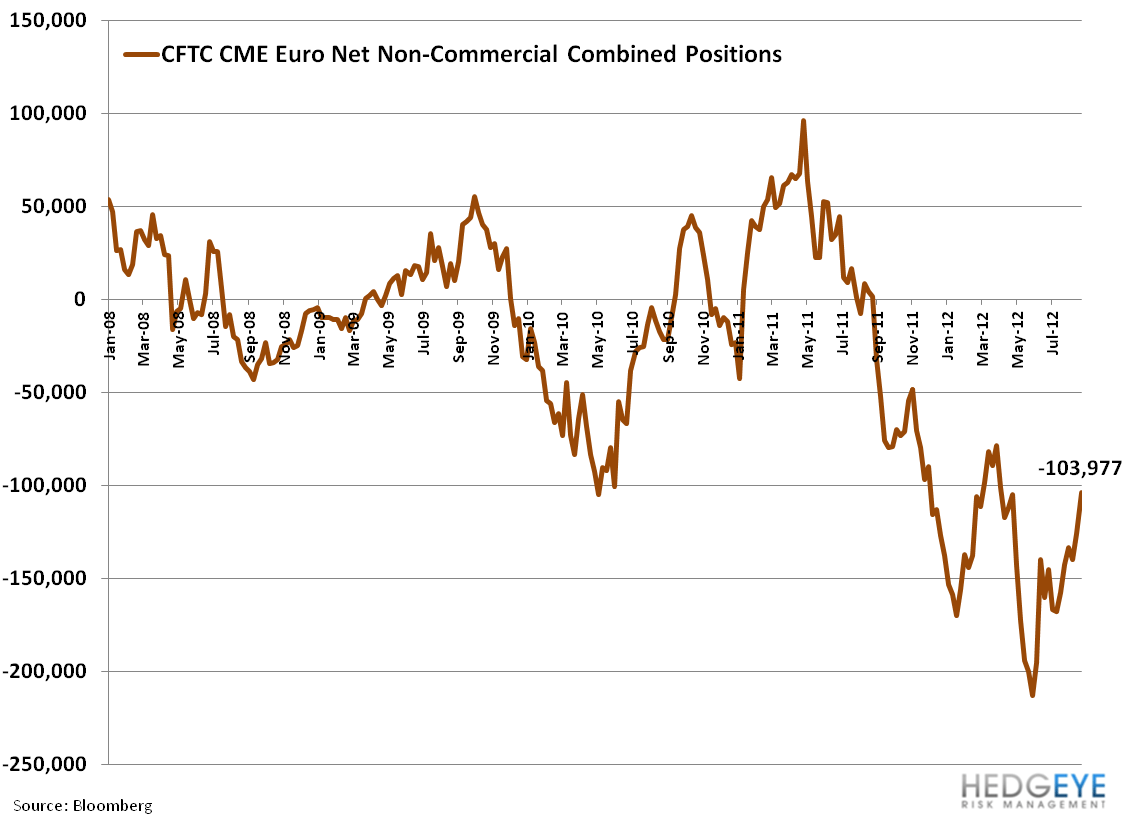

In the second chart below we look at CFTC data for net contracts of Euro non-commercial positions. Interestingly, since a high in short position in the Euro on 6/5/12 (-213.060 contracts), investors have been less bearish (and covering). Week over week, contracts are 17% less bearish, -125.817 to -103,977 as of 8/28.

Data Dump:

Eurozone Q2 GDP Preliminary -0.2% Q/Q (inline) [-0.5% Y/Y vs previous est. -0.4%]

Eurozone PPI 1.8% JUL Y/Y (exp. 1.6%) vs 1.8% JUN [0.4% JUL M/M vs -0.5% JUN]

Eurozone Retail Sales -1.7% JUL Y/Y (exp. -1.7%) vs -0.9% JUN [-0.2% M/M (exp. -0.2%) vs 0.1% JUN]

Germany Factory Orders -4.5% JUL Y/Y (exp. -4.5%) vs -7.6% JUN [0.5% JUL M/M (exp. 0.3%) vs -1.6% JUN]

Germany Exports 0.5% JUL M/M (exp. -0.5%) vs -1.4% JUN

Germany Imports 0.9% JUL M/M (exp. -0.3%) vs -2.9% JUN

Germany Labor Costs (Seasonally Adjusted) 1.5% in Q2 Q/Q vs 0.2% in Q1

Germany Labor Costs (Workday Adjusted) 2.5% in Q2 Y/Y vs 1.8% in Q1

Germany Industrial Production -1.4% JUL Y/Y (exp. -3.0%) vs 0.3% JUN

France ILO Unemployment Rate 10.2% in Q2 vs 10% in Q1

UK Halifax House Prices -0.9% AUG Y/Y vs -0.6% JUL

UK PMI Construction 49 AUG (exp. 50) vs 50.9 JUL

UK New Car Registrations 0.1% AUG Y/Y vs 9.3% JUL

UK Industrial Production -0.8% JUL Y/Y (exp. -2.7%) vs -3.8% JUN

UK PPI Input 2.0% AUG M/M (exp. 1.7%) vs 0.4% JUL [1.4% AUG Y/Y (exp. 1.4%) vs -2.4%]

UK PPI Output 0.5% AUG M/M (exp. 0.2%) vs 0.1% JUL [2.2% AUG Y/Y (exp. 1.9%) vs 1.8% JUL]

Italy New Car Registrations -20.23% AUG Y/Y vs -21.39% JUL

Spain Unemployment Change +38.2K AUG (= first increase in 5 months) vs -27.8K JUL

Spain Industrial Output -5.4% JUL Y/Y vs -6.1% JUN

Switzerland Q2 GDP -0.1% Q/Q (exp. 0.2%) vs 0.5% in Q1 [0.5% Y/Y (exp. 1.6%) vs 1.2% in Q1]

Switzerland Retail Sales 3.2% JUL Y/Y vs 3.3% JUN

Switzerland CPI -0.5% AUG Y/Y vs -0.8% JUL

Switzerland Unemployment Rate 2.9% AUG vs 2.9% JUL

Netherlands CPI 2.3% AUG Y/Y vs 2.3% JUL

Netherlands Industrial Production 0.1% JUL (exp. -2.3%) vs -2.0% JUN

Finland Q2 GDP -0.1% Y/Y vs 2.2% in Q1 [-1.1% Q/Q vs 0.9% in Q1]

Norway Credit Indicator Growth 6.9% JUL Y/Y vs 7.1%

Norway Industrial Production 2.6% JUL Y/Y vs 7.7% JUN

Iceland Q2 GDP -6.5% Q/Q vs 0.3% in Q1 [0.5% Y/Y vs 4.2% in Q1]

Greece Unemployment Rate 24.4% JUN vs 23.1% MAY

Greece Q2 GDP Final -6.3% Y/Y

Malta Q2 GDP 3.0% Y/Y vs 1.0% in Q1

Portugal Industrial Sales -3.8% JUL Y/Y vs -2.3% JUN

Portugal Q2 GDP Final -1.2% Q/Q (inline) [-3.3% Y/Y (inline)]

Ireland Industrial Production 4.8% JUL Y/Y vs 4.9% JUN

Ireland Unemployment Rate 14.7% AUG vs 14.7% JUL

Czech Republic Retail Sales 0.3% JUL vs -0.8% JUN

Czech Republic Q2 GDP Final -0.2% Q/Q (inline) [-1.0% Y/Y (initial -1.2%)]

Hungary Q2 GDP Final -0.2% Q/Q (inline) [-1.3% Y/Y (initial -1.2%)]

Hungary Industrial Production -2.2% JUL Y/Y vs 0.6% JUN

Romania Retail Sales 4.4% JUL Y/Y vs 4.0% JUN

Romania Producer Prices 5.7% JUL Y/Y vs 5.8% JUN

Romania Q2 GDP Preliminary 0.5% Q/Q (inline) [1.2% Y/Y (inline)]

Estonia CPI 3.8% AUG Y/Y vs 3.6% JUL

Estonia Q2 GDP Final 0.5% Q/Q (initial 0.4%) [2.2% Y/Y (initial 2.0%)]

Latvia Q2 GDP Final 1.3% Q/Q (initial 1.0%) [5.0% Y/Y (initial 5.1%)]

Russia Consumer Prices 5.9% AUG Y/Y vs 5.6% JUL

Russia Q2 GDP Preliminary 4.0% Y/Y vs 4.9% in Q1

Turkey CPI 8.88% AUG Y/Y vs 9.07% JUL

Turkey PPI 4.56% AUG Y/Y vs 6.13% JUL

Interest Rate Decisions:

(9/5) Poland Base Interest Rate UNCH at 4.75%

(9/6) BOE Interest Rate UNCH at 0.50%

(9/6) BOE Asset Purchase Target UNCH at 375B GBP

(9/6) ECB Interest Rate UNCH at 0.75%

(9/6) Riksbank Interest Rate CUT 25bps to 1.25% [consensus was for no change]

(9/6) Serbia Interest Rate UNCH at 10.50%

The European Week Ahead

Monday: Sep. Eurozone Sentix Investor Confidence; 4Q Germany Manpower Employment Outlook; Aug. Germany Wholesale Price Index (Sep 10-12); Aug. UK RICS House Price Balance; Aug. France BoF Business Sentiment; Jul. France Industrial Production, Manufacturing Production; 2Q Italy GDP – Final; Aug. Greece CPI, Industrial Production

Tuesday: Jul. UK. Trade Balance; 2Q France Non-Farm Payrolls – Final; Jul. Spain House Transactions

Wednesday: Jul. Eurozone Industrial Production; Germany’s Constitutional Court will rule on the ESM & Fiscal Pact; Aug. Germany CPI – Final; Aug. UK Claimant Count, Jobless Claims Change; Jul. UK Average Weekly Earnings, Unemployment Rate, Employment Change; Aug. France CPI; Jul. France Current Account; Aug. Spain CPI – Final; Jul. Italy Industrial Production; Dutch General Election

Thursday: 2Q Eurozone Labour Costs; Aug. Italy CPI - Final; Jul. Italy General Government Debt; 2Q Greece Unemployment Rate

Friday: Aug. Eurozone CPI; 2Q Eurozone Employment; 2Q Spain Labour Costs, House Prices ToT Homes; Jul. Italy Current Account

Matthew Hedrick

Senior Analyst