In January 2011, we published a Black Book outlining our concerns about McDonald’s direction as a company. The beverage strategy, in particular, was something we saw as having negative implications for the stock over the intermediate-to-long-term.

At the time, we wrote that the much-vaunted McDonald’s “Plan-to-Win” strategy has always been centered on “better, not bigger. Instead of building more restaurants, McDonald's increased profitability by squeezing more from its existing store base and from its franchisees. Over the past three years, however, the mantra has seemingly become beverages, not burgers.”

As the company has shifted its focus away from its core business, the restaurants’ have gradually become less operationally efficient. Additionally, resources are spread more thinly across the company as the menu grows. The core business, on a relative basis versus peer QSR burger concepts, suffers under this scenario. While we cannot summarily state it as fact, it is possible that the company’s core business has been declining in the U.S. and, if true, this would support the idea that Five Guys, Shake Shack and other players in the category are taking share from McDonald’s.

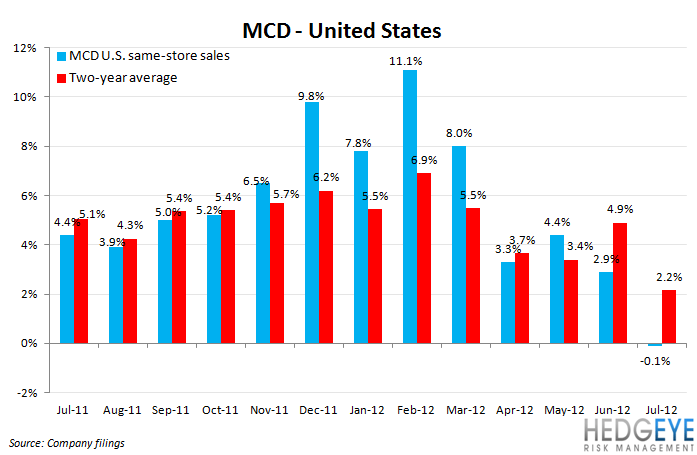

As we changed our view, from positive to negative, on McDonald’s on 5/8/12, our conviction was that sales were slowing globally and, in the U.S., there was a dearth of new menu items to “comp the comps” versus the 2011 and 2010 beverage successes. Almost exactly a year prior, on 5/9/11, we capitulated on our bearish view and accepted that changed facts, at that time, dictated a positive outlook for the company. What we missed in 2011 was how much of a success beverages could be for a second year running. In 2012, global growth slowing combined with the lack of new product momentum and an eroded value advantage versus the rest of the restaurant industry has clipped MCD’s wings.

The core tenets of our thesis has remained unchanged, however: the company needs to renew its focus on its core business. The words of Jim Skinner come to mind. He said, “We had lost our focus. We had taken our eyes off the fries."

A great article in QSR Magazine, written by former McDonald’s marketing executive Roy Bergold, discusses menu expansion and the impact it has on business and profitability. In the article, titled, “Addition by Subtraction”, Bergold advocates the simple versus complex strategy and we believe his thoughts are highly salient for McDonald’s investors today.

Clearly, a significant component of MCD’s difficulty is rooted in the macroeconomic environment but there are some self-inflicted wounds, also. In 2011, we were wary of the shift in focus from burgers to beverages and that is still the case today. From here, for us to become more constructive on the long side of MCD, we will be looking for management to reverse course and simplify, rather than complicate, the menu so that the company can refocus on its core menu. We are not expecting any such announcement soon, however, given that it would effectively be a mea culpa on the part of CEO Don Thompson, the man behind McCafé.

August sales will be released on the 11th and we will have a note out in advance. Sequentially, we are expecting a better result than July’s, but from there the outlook suggests a difficult top-line environment potentially through February 2013.

Howard Penney

Managing Director

Rory Green

Analyst