CAT’s Deep Cycle Dive - Why Not to Own CAT Here

Summary

Caterpillar is a company we would love to love. It competes well in a number of very good industries, meeting the second criteria in our investment process. It has great products and a well-established dealer network. The stock is trading well off its highs. Unfortunately, it is also a deep cyclical. The resources investment cycle appears to be turning against CAT from a very, very high peak. An upswing in construction equipment appears some years away. CAT has a unionized workforce and other significant fixed costs. Importantly, CAT does not seem prepared for the resources investment cycle to move against them. If anything, management has directed the company towards further resources exposure. Finally, the current valuation does not reflect these risks, in our view. Investors stuck on the long side in CAT could be in for a long period of volatile underperformance.

End-markets Near Peaks and Appear to be Heading Lower

- Resources: Mining companies like Vale and BHP are CAT’s largest customers. Resources capital investment appears set to decline. Coal prices have been very weak in relevant markets and mining capital spending is coming off of bubble-like levels. Resources investment has been the key driver of CAT’s growth over the last five years.

- Construction: The bulge in construction equipment purchases from 2004-2007 should not see a replacement cycle until the second half of this decade.

- Power: Oil & gas capital investment, a significant market for CAT, is expected to see growth slow to a stand-still by year-end.

CAT Appears Unprepared for Weakening End-Market Growth

- Increasing Exposure: CAT has made significant acquisitions in mining equipment, a business with end-markets near a cyclical peak, in our view.

- Working Capital & Capacity: CAT’s inventories are excessive and the company’s efforts to add capacity have been misplaced, in our opinion.

- Challenging Problems: Excess inventory and misdirected capital investment are not problems that are resolved quickly.

Cyclically Adjusted Valuation Lower Than Share Price

- Further Downside Risk: We see CAT’s fair value in the $50-$70 range.

- Not Reconciled: CAT is still well-liked, with about 60% Buy ratings. It is broadly owned and is frequently miscategorized as a construction equipment company.

- Not a Growth Business: CAT serves mature, GDP-type markets that have been growing faster than GDP for some time. That is a red flag.

Overview

When we launched Industrials coverage at Hedgeye, we noted that CAT was exposed to resources related equipment and that resources investment was extremely elevated. CAT, Komatsu and other mining exposed names were a place we would avoid on the long side, even though those businesses generally had strong franchises. We have received a number of questions on that view, many of them quite good. Below, we expand our discussion of why CAT is a name to avoid on the long side. We focus on the impact of more recent data on end market exposures, though there are many additional matters, both positive and negative, that could be addressed at CAT.

CAT is less exposed to construction equipment than many investors believe, in our view. The outperformance in the shares has been driven by what we see as a bubble in resources investment. CAT has dramatically outperformed the Industrials sector over a period in which key construction markets have fallen significantly.

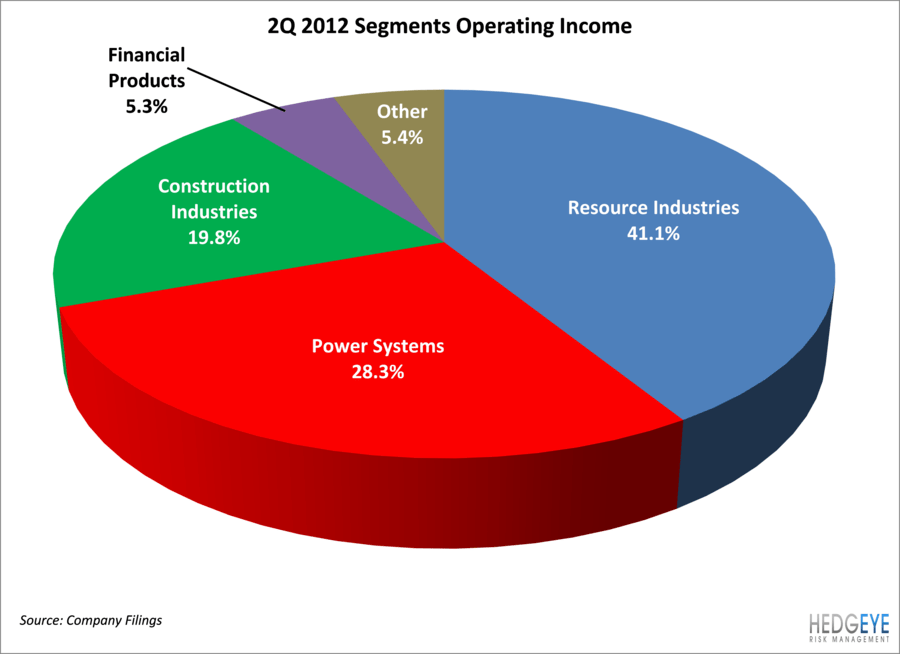

Following the acquisition of Bucyrus and moves into other commodity exposed product lines, Resource Industries has become CAT’s largest and most profitable business. The construction equipment business is smaller and lower margin.

End Market Exposures: Resource Industries

“And if you look at our company inside, you would see a higher concentration in mining than construction. And it just so happens that much of the growth over the past five years for us has been mining.” - Michael DeWalt 8/11/12

Dominant Exposures: Coal, iron ore and copper make up 70%-75% of CAT’s largest division, Resource Industries.

Coal is Roughly a Third of Resource Industries; Coal Capital Investment Prospects Look Poor

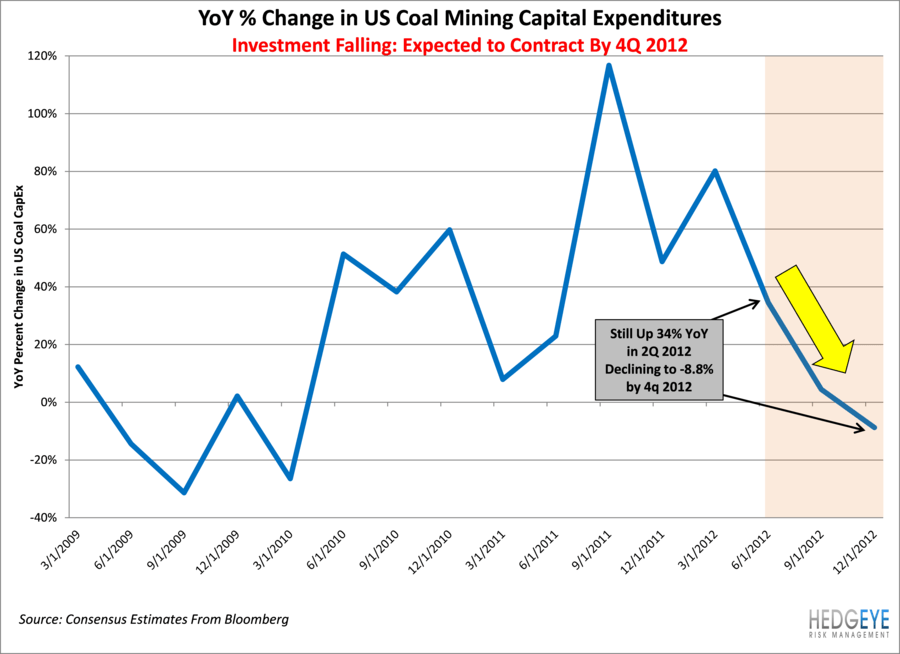

US Coal: CAT has said that about 30% of equipment sales in its Resource Industries segment are tied to coal mining, with about half of that in the United States. Low natural gas prices have resulted in what is likely to be a sustained slowdown in US coal capital spending. While this outlook may not be surprising, what may be is that declines in coal capital investment have not happened yet. Consensus estimates suggest that capital spending reductions will bite this quarter and next.

Ex-US Coal: Since about 2/3s of global coal consumption is in Asia, it is probably fair to assume that a good portion of the ~$5 billion in resources revenue from that region is coal related. China is the dominant Asian coal consumer. Recent declines in coal prices in China may slow capital investment in this industry. Note that these are very large and very recent declines.

Steam Coal, Too

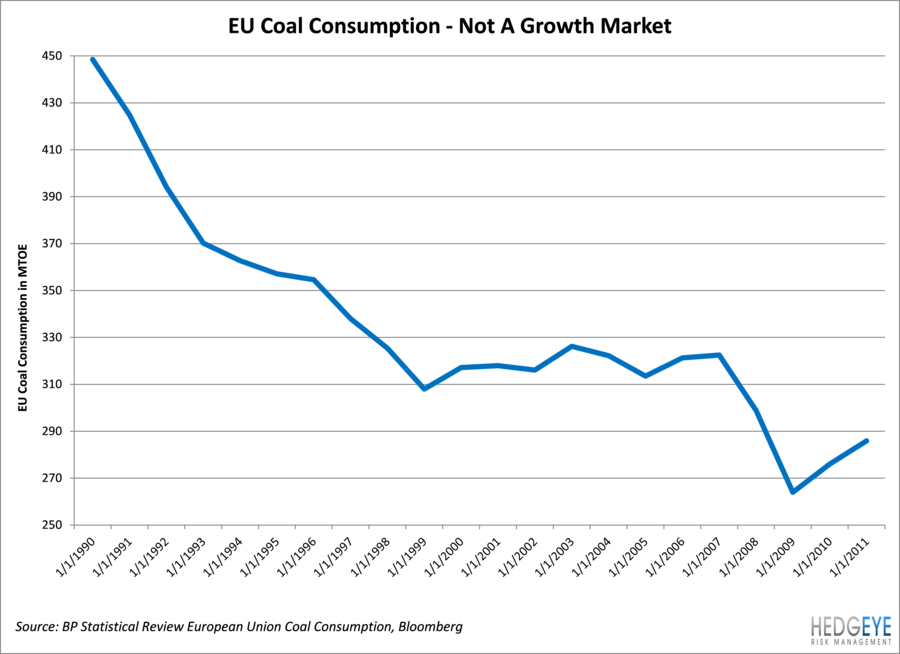

Finally, Europe is a declining market for coal.

Mining: The Major Resource Industries Exposure

Long-term, mining is a sub-GDP growth industry that goes through investment cycles. Below, we chart CAT’s long-term performance to resources investment.

Mining Investment Slowing: The view that mining capital expenditures are under pressure is no longer a forecast. This spending is well over half of Resource Industries, by our estimates, and is dominated by copper and iron ore. Recent capital investment cuts by BHP and Fortescue suggest that this part of CAT’s Resource Industries segment is likely to weaken. The decline in mining capital investment has a long way to go, in our view. We have published the graph below on mining capital expenditures, which seems pretty self-explanatory. The most important concept to take away from this chart is that mining capacity could continue to expand even if this graph were cut in half. It is capital investment above depreciation, not just capital investment. This is a graph approximating growth capital spending. We expect 2012 to be the peak in spending, with spending levels noticeably lower by 2014. Our macro team shares a similar outlook (https://app.hedgeye.com/feed_items/22937).

Chinese Metal Demand: We have previously noted the decline in construction related Chinese metal prices. Below, we present the chart of real Chinese rebar prices, which has fallen significantly in August and is currently below its financial crisis lows. Vale and BHP have both spent significantly on iron ore capacity.

Oil Sands: Some have suggested that Oil Sands are a major driver for CAT. Finning, a public CAT dealer, has given some useful insights into the Canadian oil sands equipment market. By our estimates, it looks like Canadian Oil Sands will represent at most a few percentage points of total CAT sales on the equipment side. Although capital spending by these companies is expected to ramp in 2H 2012, growth in this smaller end market is likely to be overwhelmed by weakness in coal and metal/mineral markets.

Cancellations: CAT has shifted its tone to “modest cancellations” when describing mining-related orders, but it seems clear to us that cancellation activity will increase. It would be reasonable for miners to first push out orders the contractually allowed 6 months rather than canceling the order immediately and negotiating terms on the typical 5% deposit. Moving into year-end, we may see increased cancellation activity. CAT’s stock may not react well to increased cancellations.

End Market Exposures: Power Systems

CAT’s Power Systems segment contains a number of different businesses, from locomotives and generator sets to fracking equipment and industrial turbines. Locomotives, certain gen sets and turbine applications are also related to mining and coal capital investment. However, one of the division’s key exposures is oil and gas extraction and transportation/compression.

Oil & Gas: While the dynamics of oil and gas investment seems more robust than mining investment, it also appears to be slowing. Below, we present a chart showing capital spending growth for large energy companies, including consensus estimates through year end. By 4Q 2012, current estimates for these companies show no growth in year-over-year capital investment. While those estimates may change depending on commodity prices and other factors, it does not suggest that there will be enough energy investment growth to offset the slowdown in other markets. Our firm’s long-term view is bearish on oil prices (see work by our energy analyst Kevin Kaiser) and the weak capital investment outlook suggests that this exposure could become its own problem area for CAT.

Pre-Buy Boosting Current Results? There is the potential that Tier IV emissions regulations, which impact different engines at different times until 2015, are causing higher than normal sales for Caterpillar. For example, Toro has noted some Tier IV driven activity in its commercial products. The Gen Set compliance deadline is for model year 2015. Certain other CAT product lines will need to comply by 2013 and 2014. It is very hard to determine the aggregate impact, but it is worth noting. We are hosting a conference call this Wednesday, September 12, with an EPA emissions regulations expert where we will explore the impact of Tier IV and other regulations.

End Market Exposures: Construction Industries

Construction equipment sales in developed markets are currently depressed. Expectations for a rebound are a reason we frequently hear that people own CAT shares. However, we note two reasons why this optimism is likely misplaced.

Emerging Markets: China is the largest market for construction equipment globally. The declines in equipment sales in China are well-known. The prospects for a developed market rebound are held back by large government deficits that may keep infrastructure spending weak.

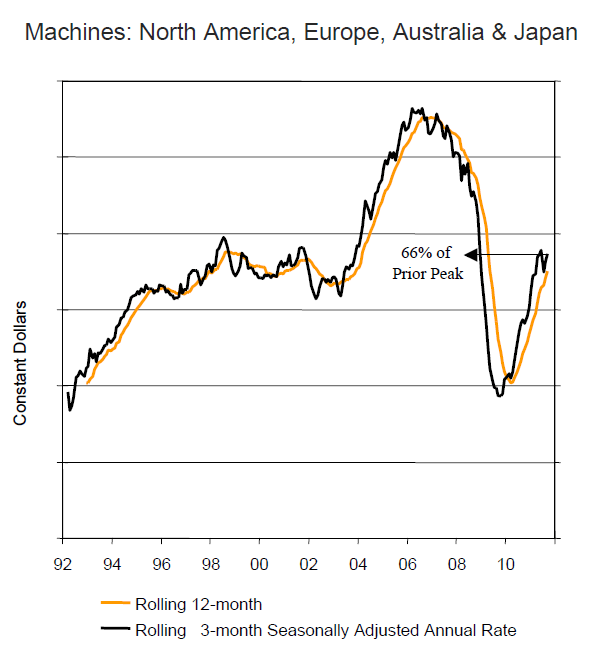

Construction Equipment Generally Last 10-15 Years: The bubble in construction equipment purchases from 2004 to 2007 will probably not need to be replaced until the second half of this decade. Utilization of construction equipment has been lower during the financial crisis, which may actually push out that replacement cycle. There is little reason to expect an up cycle in new construction equipment in the next few years.

(Source: Caterpillar Company Presentation)

URI Fleet Utilization: Because of difficulty in finding construction equipment utilization data, many analysts present the United Rentals fleet utilization data. URI is a sophisticated operator that manages fleet utilization, selling excess equipment and buying when utilization is too high. As a result, URI utilization is not a useful indicator.

CAT Not Prepared for Slowdown

CAT has been acquiring mining-related companies, adding capacity, and building inventories. With resource capital investment apparently reversing, changing course will take a long time and be very costly. Wait for impairment charges.

Acquisitions: CAT has been on a commodity related buying spree in the last couple of years. Bucyrus was purchased for about $9 billion – a company (with most of the same businesses) that had an enterprise value of less than a billion dollars in 2004. In our view, that is buying into the mining bubble – aftermarket sales or not. ERA Mining is another near billion-dollar commitment. These acquisitions do not suggest that CAT takes the risk of a decline in mining capital investment seriously.

Inventories: CAT has excessive inventories, which they have acknowledged. They have said it is mostly in China, which seems odd since they have also said that sales in China are only 3% of the total. This may take a while to resolve or may involve charges/discounting. Mining equipment is more inventory intensive, which further demonstrates the shift in mix toward resources equipment.

Capacity Additions: CAT has added significant capacity in the past few years and continues to do so, perhaps driven by the memories of pre-financial crisis bottlenecks. A capital equipment manufacturer should generally remove capacity as the cycle turns. For example, mining truck capacity at CAT’s Decatur plant doubled since 2010. Capacity continues to be added in China, where CAT probably has half the revenues that it expected when it committed to those capacity addition projects. A few plants are still under construction in China. While the many expansions in the US have probably made production more flexible, the costs of these expansions have been significant and the demand may not materialize.

Backlogs Dropping: We have noted declining backlogs before, but it bears repeating, that CAT “beat” last quarter by drawing down backlogs. Historically, backlogs are one of the best correlates for CAT’s relative performance.

Aftermarket & Service: Mining and Utilization Key

CAT does not pin down traditional aftermarket parts revenue, but groups it together with a number of other businesses, including financial services. This is unhelpful. That said, it might represent around a quarter of sales after Bucyrus, which was very parts intensive.

Aftermarket parts sales are not always recurring. Small changes in utilization can lead to big changes in aftermarket parts revenue. When commodity prices are high and equipment is being used around the clock, the revenue stream is healthy. However, when equipment can be idled, maintenance may improve and unused equipment can provide parts. Recent commodity price declines may well presage lower utilization. We have recently heard of coal miners in the US redeploying and parting out idled equipment to save money.

“Another area that we've been very active in is on our capital. We've lowered our capital spending, tried to match it up with the lower volumes. We're trying to match up our maintenance capital with the lower volumes. With the idling of some coal mines, we've actually redeployed some of our idle equipment to productive mines, saving us probably $30 million to $40 million of capital a year over the next several years, so we think we've done a good job” - John Eaves, Arch Coal 9/6/2012

Disconfirming Evidence

There is the behavioral bias to overly scrutinize disconfirming evidence, which we want to avoid. Highlighting disconfirming evidence can be helpful.

Chinese Property Prices: We have seen recent improvements in Chinese property prices. This represents a significant disconfirming data point to the bearish thesis outlined above. That said, here is why we would be cautious on calling a turn in the Chinese housing market (our Macro team can give additional detail and color here).

- Price increases have been very small (~20bps)

- Generally, only new homes are in the data

- The data looks at average prices instead of median prices

- The data runs counter to the stated intention of policy officials

- Residential construction spending is only about half the size of nonresidential spending

Hedgeye hosted a conference call with global macro expert Jim Rickards last week. He made the point that any party official with the clout to get economic stimulus implemented is probably using that clout to position themselves for the power transition. The likely result is political stagnation. It is our sense that CAT management expects stimulus later this year and that they may well be disappointed.

CAT Order Activity: CAT’s order activity improved in July, particularly in Asia/Pacific. This bears watching, but we do not think that the data represent a change in direction. Falling Chinese rebar prices and spending cuts by mining companies like BHP and Fortescue should provide a more forward looking indicator than these order metrics. However, if the monthly retail sales data continues to improve, we would reevaluate our view.

Asia Pacific data for July was strong, but the data is noisy.

Backlogs & Manufacturing Efficiency May Help: CAT has pointed out that, in addition to increasing capacity, recent capital expenditures have improved the flexibility of their plants. We do not doubt that this is true, but we still expect reduced utilization to rub against high fixed costs. The company also has a healthy backlog, but the order backlog may drop if end markets weaken. Backlogs are usually a major driver of the stock. Cancellations, as noted above, are likely to follow order delays. It is hard to extract significant cancellation penalties out of large customers, in our view.

Valuation: Getting There…

Fair Value: We currently see CAT’s fair value in the $50 – $70 range, below the present share price. We use a scenario-based DCF approach and there is significant ambiguity with respect to the company’s cyclical exposures. This ambiguity leads to a relatively wide valuation range.

Sentiment: CAT is better liked than most of the Industrials sector.

P/E Low?: Importantly, P/Es do not work in highly cyclical stocks. In fact, a low P/E is frequently a sell signal and a high P/E a buy signal. To the extent that resources related capital investment declines, we would expect to see relative underperformance and multiple expansion.

Conclusion: We see clear evidence of a down swing in resource capital spending. We do not see CAT bracing for a change of direction in their key end markets. Until very recently, we have actually seen them acquiring more rope. At present levels, we do not think that the market has fully priced in the risks. Perhaps most importantly, well-informed players like BHP and Fortescue are signaling that they see less opportunity for mining investment. Investors that stay in CAT are ignoring that signal.