“No man can properly command an army from the rear; he must be at its front.”

-General William Tecumseh Sherman

I don’t force myself to write every morning. I have a passion to find the truth. I want to be on the front lines of that daily search.

On the Research Front, that doesn’t mean I’ll always find the truth; it just means I expect to. On the Risk Management Front, that doesn’t mean I am certain of anything markets will do; I am constantly humbled by their uncertainty.

That’s my life At the Front. Research (Growth Slowing) and Risk Management (market moves) are 2 very different things. Long-term, I think you are best prepared to have a process that embraces both. Winning and losing battles happens in every position, everyday. The war, however, is far from over.

Back to the Global Macro Grind…

Hats off to them. I have no problem giving credit to my competition where it is due. The last 48 hours of global equity market trading has provided for one of the more impressive Keynesian Central Planning performances in at least the last 40 years.

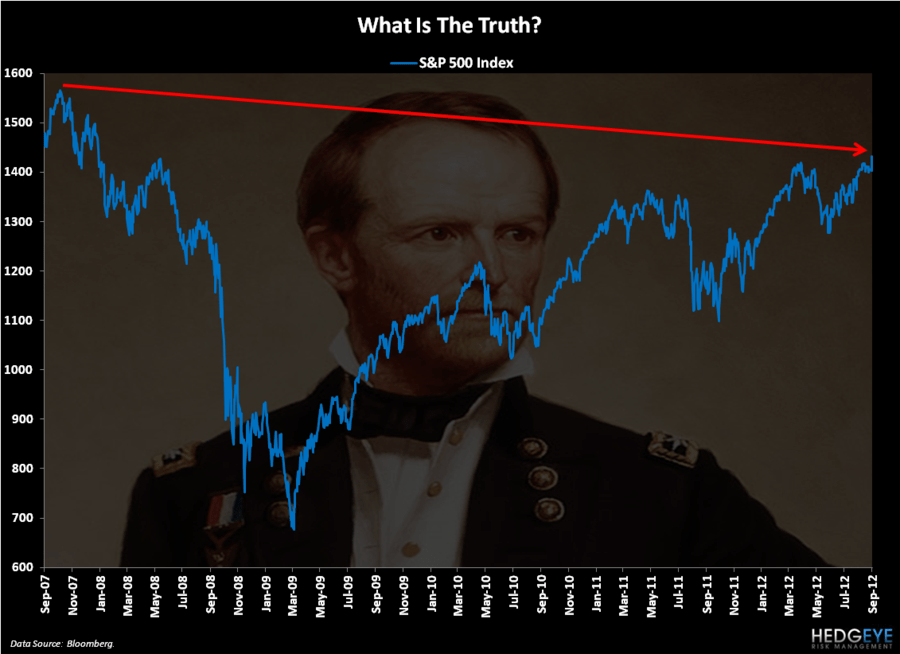

Just think, it was only January of 2008 when you could have bought the SP500 at this very same price. You’d have had to have taken a very “long-term investor” view from that price… and mostly everything the buy-high bulls told you to buy on would have changed at least once every 3 months during the next 5 years… but now, after a little volatility, you are back to break-even, right?

Back to reality…

At The Front of real-time risk management this morning, yesterday is over. Now, what we really need to ask ourselves is what I have been borrowing from Ray Dalio’s Principles as of late, “What Is True?”

This usually happens when I am short-term wrong – I have more questions than answers:

- Is the US bond or stock market right on growth?

- What is the US stock market? the SP500 (higher-highs yesterday) or Russell2000 (lower-highs yesterday)?

- Is the European bond or stock market right on growth?

- Are German stocks (higher highs vs March this morning!) or the Eurostoxx600 (lower-highs) right?

- Is the Asian bond or stock market right on growth?

- Was the 1-day +3.7% rip off the YTD low in Chinese stocks the bottom or another lower-high?

If you have all the answers to these questions nailed down, across immediate to long-term durations, give me a buzz. On growth, the answer isn’t what the SP500 is “up year-to-date.” That’s just a short-term proxy for how less and less people get paid.

If that was the answer in Weimar Germany in 1923 or, say today in Venezuela’s IBVC Index (+155% YTD post currency debauchery), that would have been good and fine until revised as a very wrong answer. I guess they needed “more time.”

To review: stock and commodity market inflation is not economic growth.

The former is helpful to some, the latter is hurtful to many. I didn’t hear that coming out of either the RNC or DNC in the last few weeks. Why? Because both parties are Keynesian in their economic policy. Sadly, Obama and Romney look a lot more like Carter and Nixon, than they do Reagan or Clinton to me.

At this point, maybe I can appeal to both the far left and right of each party. Political strategists, you will love this storyline: when I came to this country (mid-1990s), I was an immigrant… son of a teacher and firefighter…

I had no money… I was the beneficiary of two US Administrations (Reagan and Clinton) who had the three things that someone like me could believe in – Strong Dollar, Low Oil Prices, and Free-Market Capitalism. I worked 3 jobs; I took risks; got married, had 2 beautiful American children, and hired 50 people – a Made In America exporter of ideas…

Enough of the storytelling drama already. I didn’t earn any of this kissing anyone’s rear at the 2007 September-October stock market highs. I didn’t beg for bailout money at the 2008-2009 lows either. I sucked it up; I took my losses; and I carried on.

So don’t expect me to fade and not face the front lines this morning. From the top, to the bottom, and back again - it’s been a long 5 years writing to you – and there is still a war to be won.

My immediate-term support and resistance risk ranges for Gold, Oil (Brent), US Dollar, EUR/USD, UST 10yr Yield, and the SP500 are now $1, $112.21-114.92, $80.98-81.61, $1.24-1.26, 1.56-1.72%, and 1, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer