Mixed feelings about August

As we already knew, August GGR grew 6.1% (in US$), in-line with our expectations and above the 1.9% growth in July. After looking through the data, it appears that August was softer than the headline as VIP volumes were worse than we expected but VIP hold was higher. We continue to think that September growth will be better than August, likely to grow in the low double-digits YoY. Indeed, we are already hearing that the first weekend in September was very strong.

We estimate that total direct play this month accounted for 6.6% of the market, compared with 6.8% in August 2011. The total VIP market held at 3.10% vs. 2.91% in August 2011. Adjusting for direct play and theoretical hold of 2.85% in both months, August revenues would have only increased 1.7% YoY.

The good news is that Mass and slot revenues continue to come in strong, posting 27% and 16% YoY growth, respectively. The bad news, which should come as no surprise, is that VIP volume was down 6.6% YoY, marking the 3rd consecutive month of YoY declines. LVS was the only concessionaire to produce YoY growth in Junket RC volume and VIP revenue.

Company-specific Takeaways:

LVS

- LVS led the market in GGR growth, up 42% due in part to the April opening of SCC and the VIP push at Four Seasons

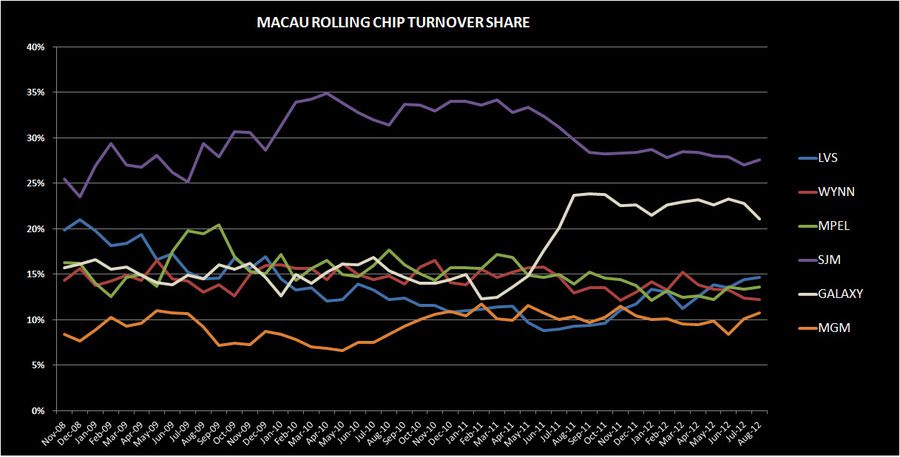

- LVS held a little below its 12-month average but its VIP volume share of 14.7% was the company’s best share since January 2010

- LVS posted its second highest Mass share (behind July) since SCC opened

- Overall, a better month than the headline 19.0% market share would suggest

Wynn Macau

- Wynn’s share accelerated in August but that was entirely due to high VIP hold

- Mass share is holding its own since SCC opened but Junket RC share fell 10bps to 12.2%, the property’s second lowest share since October 2007

- Despite the high hold, Wynn recorded its 5th straight GGR decline due to slot revs falling 20%

MPEL

- MPEL’s GGR fell for the 4th time of the last 5 months. However, all the losses have been driven by Altira. CoD has yet to see a month of YoY declines.

- However, Mass had another strong quarter, up 27%

MGM

- MGM’s strong market share gains this month were driven mainly by VIP volumes

- Hold was just a bit above its 12-month average

- GGR was up 1% YoY

Galaxy

- Galaxy generated the 2nd highest growth of any concessionaire, up 7%

- YoY growth was once again driven by Mass – up 77%

- VIP hold percentage was well above normal. VIP volume dropped 17% YoY – the first decline since February 2009.

- We think it’s interesting to note that Galaxy Macau’s VIP market share is equivalent to WYNN’s, higher than MPEL’s and not far behind LVS’s portfolio share of 15.9%

Y-O-Y TABLE OBSERVATIONS

Total table revenue growth accelerated from just 1% in July to 6% in August. Mass revenue growth was healthy at 27%, but lower than the 38% growth rate we’ve seen over the trailing twelve months. VIP revenues fell 1%, while Junket RC declined 7%, marking the 3rd consecutive month of declines. As a point of reference, there were 7 consecutive months of decline in VIP RC volume from December 2008 through June 2009; although the dip was more severe than the single digit declines we’ve witnessed to-date. We expect growth to resume with the opening of Ph2 of Sands Cotai Central.

LVS

Table revenues grew 43% YoY, garnering the best growth in the market by a mile. Sands China’s strong performance in the month of August was aided by an easy hold comparison in 2011. We estimate that the Sands portfolio of properties held at 2.94%, vs 2.62% last August, adjusted for direct play. Sands was the only concessionaire to produce YoY growth in Junket RC volume and VIP revenue.

- Sands table revenues fell 24% YoY, marking the 5th consecutive month of declines. The good news is that almost the entire YoY decline came out of the lower yielding VIP segment.

- Mass fell 1% YoY, the propertys’ first decline since Jan 2011

- VIP declined 35% YoY. Hold was low and the comparison was difficult. We estimate that Sands held at 2.61% in August compared to 3.51% in the same period last year. We assume 9% direct play in August vs. 15% in August 2011 (in-line with what we saw in 2Q12 and 3Q11).

- Junket RC was down 10%. This was the 9th consecutive month of YoY declines in VIP RC at the property.

- Venetian table grew 30% YoY. Strong August performance was driven by strong Mass win, high hold and a very easy comp on the VIP side.

- Mass increased 21%

- VIP grew 39%

- Junket VIP RC fell 21%, marking the 7th consecutive month of declines at Venetian. In the 12 month period spanning from September 2008-2009, Venetian saw 10 months where junket RC volumes fell.

- Assuming 28% direct play, hold was 3.87% compared to 2.22% in August 2011, assuming 24% direct play (in-line with 3Q11)

- Four Seasons continued to perform well, growing 87% YoY

- Mass revenues dropped 33%

- VIP soared 135% and Junket VIP RC rose 139% YoY

- If we assume direct play of 16%, in-line with 1Q12 and 2Q12, hold in August was 2.81% vs. 2.21% in August 2011 when direct play was 38% (in-line with 3Q11)

- Sands Cotai Central produced $106MM in August, compared with $135MM in July, $117MM in June, and May's $135MM. The drop MoM drop off is a result of bad luck in August.

- Mass revenue expanded to $40MM, $3MM higher MoM

- VIP revenue of $66MM was the lowest VIP output, post opening

- Junket RC volume of $2,682MM, increased 2.3% MoM, setting a record for the property

- If we assume that direct play was 12%, hold would have been just 2.17% - the lowest since the property opened in April

WYNN

Wynn table revenues eked out 0.4% growth in August, breaking a 4 month streak of YoY declines. The slight growth produced in August was aided by high hold.

- Mass growth grew 12%

- VIP revenues fell 2%

- Junket RC declined 12%, marking the 4th consecutive month of declines

- Assuming 8% of total VIP play was direct (in-line with 2Q12), we estimate that hold was 3.39% compared to 3.07% last year (assuming 10% direct play – in-line with 3Q11)

MPEL

MPEL table revenue fell 5%, winning the prize of worst concessionaire performance. Although hold across MPEL’s 2 properties was normal at 2.86%, last year's comparison was tougher at 3.00%.

- Altira revenues fell 41%, due to a 45% decrease in VIP. Mass fell 1%. Results were negatively impacted by low hold and a difficult comparison.

- VIP RC decreased 17%, marking the 9th consecutive month of declines which have averaged -19%

- We estimate that hold was just 2.06%, compared to 3.15% in the prior year

- CoD table revenue grew 16%, aided by high hold

- Mass revenue grew an impressive 32%, while VIP revenue grew 10%

- RC declined 3%

- Assuming a 15% direct play level, hold was 3.30% in August compared to 2.91% last year (assuming 15.7% direct play levels in-line with 3Q11)

SJM

Table revenue fell 3%, the 4rd consecutive month of declines

- Mass revs was up 8% offset by a 8% drop-off in VIP revs

- Junket RC was down 13%. This was the 7th month of consecutive declines for VIP volume across SJM’s portfolio.

- Hold was 2.83%, compared with 2.65% last August

GALAXY

Galaxy’s table revenue grew just 7%, but that was enough to win the spot of 2nd best growth amongst the 6 concessionaires. Mass growth still led the market with growth of 77% which was offset by a 4% decline in VIP growth. Galaxy's hold was 3.51% vs. 3.05% in August 2011.

- StarWorld table revenues fell 28%

- Mass grew 35%, offset by a 33% drop in VIP

- Junket RC fell 28%, marking the 3rd month of consecutive declines

- Hold was 2.87%, compared with last August’s hold of 3.12%

- Galaxy Macau's table revenues grew 21%.

- Mass grew 84%

- VIP grew 7%, while RC increased 34%

- Hold was very high at 4.04% vs. 2.98% last year

MGM

MGM’s table revenue fell 1% in August.

- Mass revenue grew 46%

- VIP revenue fell 9% and VIP RC declined 3%.

- If direct play was 9%, then August hold was 3.12% compared to 3.32% in August 2011

SEQUENTIAL MARKET SHARE

LVS

Despite producing the best YoY growth, LVS was the biggest share loser in August, closing the month at 19.0%, -2.5% MoM. Despite the MoM drop-off, August's share was still better than its 6 month trailing market share of 18.3% and 2011 average share of 15.7%.

- Sands' share was 3.6%, down 30bps MoM. For comparison purposes, 2011 share was 4.6% and 6M trailing average share was 3.8%.

- Mass share was 5.6%

- VIP rev share was 2.8%, flat with July

- RC share was 3.1%, 40bps better than its 6M average

- Venetian’s share fell 40bps to 8.5%. 2011 share was 8.4% and 6 month trailing share was 7.6%.

- Mass share fell 40bps to 14.3%

- VIP share decreased 30bps to 6.3%

- Junket RC share increased 10bps to 3.9%

- FS decreased 70bps to 3.1%. This compares to 2011 share of 2.2% and 6M trailing average share of 4.1%.

- VIP share decreased 70bps to 3.8%.

- Mass declined 60bps to 1.1%, the lowest share since opening

- Junket RC fell 20bps to 3.7%

- Sands Cotai Central's table market share fell to 3.4% in August from 4.6% in July.

- Mass share of 4.6%, marking a property record

- VIP share of 2.9%

- Junket RC share of 3.9%, flat with July, and tied with Venetian’s share

WYNN

Wynn gained 100bps of market share in August, rising to 12.3% due to high hold. While its August share was far below Wynn’s 2011 average of 14.1%, it was better than their 6-month trailing average of 12.0%. We expect Wynn’s share to struggle in the face of a ramping Sands Cotai Central.

- Mass market share was 8.7%, up 80bps MoM

- VIP market share rose 1.2% to 13.7%

- Junket RC share fell 10bps to 12.2%, the property’s second lowest share since October 2007

MPEL

MPEL’s fell 20bps in August to 13.1%, below their 6 month trailing share of 13.4% and 2011 share of 14.8%. The good news is that the entire share drop was due to losses at Altira, which were primarily hold driven. CoD’s share expanded in August.

- Altira’s share grew 90bps to 2.8%, the property's lowest share since July 2007 and well below its 6M trailing share of 3.9% and 2011 share of 5.3%. Much of the share drop can be attributed to low hold in August.

- Mass share was flat at 1.5%

- VIP fell 1.4% to 3.3%, the property's lowest share since July 2007

- VIP RC share decreased 30bps to 5.2%

- CoD’s share grew 70bps to 10.1% aided by strong hold. August’s share was the property's best share since September 2011 and well above its 2011 and 6M trailing share of 9.3% and 9.4%, respectively.

- Mass market share increased 70bps to 10.4%

- VIP share grew 80bps to 10.0%

- Junket RC grew 60bps to 7.8%

SJM

SJM was the second largest share loser in August. SJM’s share fell 1.1% to 25.0% in August. August’s share compares to their 2011 average of 29.2% and its 6M trailing average of 26.8%.

- Mass market share fell 1.1% to 30.6%, setting a new record low

- VIP share fell 1.4% to 23.6%

- Junket RC share increased 60bps to 27.6%

GALAXY

Galaxy gained 1.3% share in August, rising to 20.2%, above its 6M trailing share average of 19.7%

- Galaxy Macau share gained 2.8% to 12.6%, aided by record hold of 4%

- Mass share was 9.7%, relatively unchanged MoM

- VIP share gained back July’s loss, growing 3.9% to 13.7%- the properties’ second best market share month since opening

- GM’s VIP market share is equivalent to Wynn’s, higher than MPEL’s and not far behind LVS’s portfolio share of 15.9%

- RC share fell 30bps to 11.2%

- Starworld share fell 160bps to 6.6%, the property's lowest share since September 2008

- Mass share declined 20bps to 3.0%

- VIP share fell 2.3% to 8.0%

- RC share fell 1.2% to 9.1%, the property's lowest share since June 2009

MGM

MGM was the biggest share gainer in August due to a 60bps increase in MoM hold. Their share increased 1.5% to 10.4%, close to its 2011 share of 10.5% and above its 6M average of 9.8%.

- Mass share increased 90bps to 7.5%

- VIP share grew 2% to 11.1%

- Junket RC grew 70bps to 10.8%

Slot Revenue

Slot revenue grew 16% YoY to $135MM in August

- MGM took the top prize for YoY growth of 48% to $22MM. Interestingly, this is the 3rd consecutive month when MGM had the best slot growth.

- SJM had the second best growth YoY at 28% to $18MM

- LVS grew 27% YoY to $38MM

- Galaxy grew 14% YoY to $17MM, just behind the record they set in January 2012

- MPEL’s slot revenue grew 8% to $23MM

- WYNN had the worst YoY performance in slots with a 20% YoY decline to $20MM: 47% below their record of $32MM set in May 2011. Part of the decrease is likely due to capacity constraints and yield management efforts that have reduced slot counts at the property by approx 7% YoY.