POSITIONS: Short Small Caps (IWM)

The storytelling out there on why the market isn’t going straight down is fascinating. It was in mid-March too. Growth is slowing, globally, at an accelerating rate (inflation policies do that) and the only big part of the bull case that’s left is bailouts.

All the while, like it did in March-April, the broader market continues to make lower-highs on lower and lower volumes. Imagine they took APPL out of the SP500; then the storytelling would get really good.

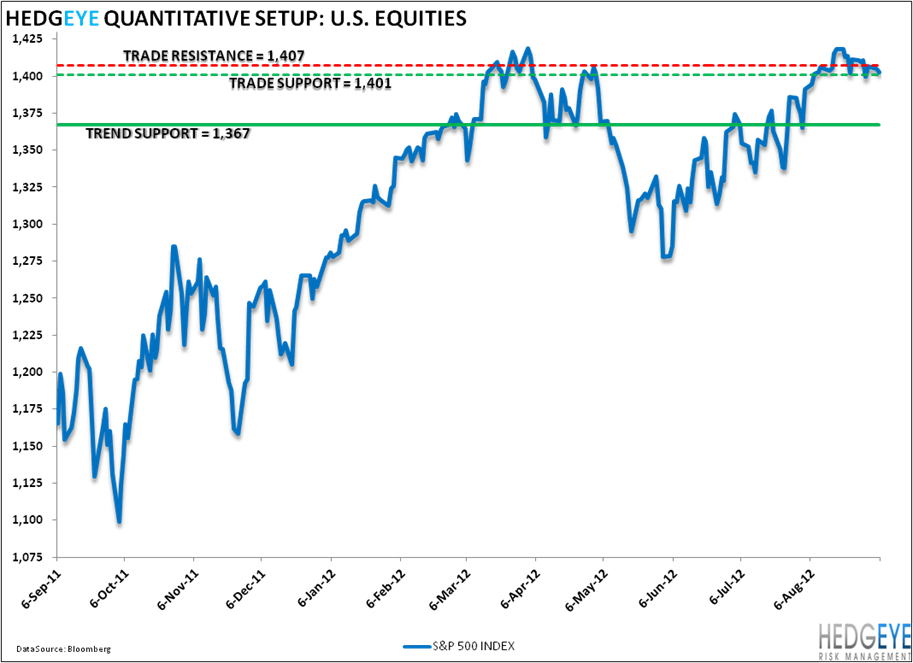

Across my core risk management durations, here are the lines that matter to me most:

- Immediate-term TRADE resistance = 1407

- Immediate-term TRADE support = 1401

- Intermediate-term TREND support = 1367

In other words, provided that 1401 holds, the market’s range can easily remain tight (1401-1418). That 17 point range is less probable on a close below 1407; and a close below 1401 puts 1367 in play, faster.

Central planning is so exciting!

Keith McCullough

Chief Executive Officer