Our statistical analysis has found that Mass gaming revenues and VIP volumes lag the Shanghai Stock Index (SSE) by 4 and 3 months, respectively. That is, the YoY change in Chinese stocks is a statistically significant driver of the YoY change in Macau gaming revenues (GGR), albeit on a lag. The upshot here is that while we still believe we are above consensus expectations for the rest of the year, based on the recent performance of the SSE, there could be 1-3% downside to our monthly YoY GGR projections.

We’ve seen and authored studies in the past that showed no correlation between the Shanghai Composite and Macau gaming revenues (GGR). An astute client of ours recently suggested that Macau could follow the same pattern as a number of US-based industrial companies that saw their China business lag the Chinese stock market. The theory is that the SSE is a discounting mechanism that leads China's economy up or down which in turn contributes to or detracts from gaming revenues in Macau.

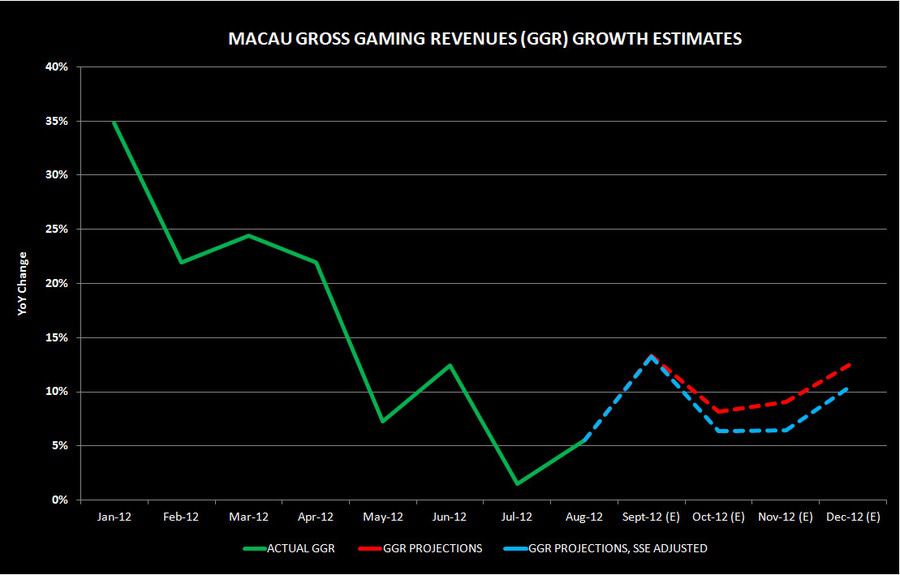

The good news is that July was such a poor month and the stocks have already taken a beating. Moreover, when we plug the SSE impact into our model, it only reduces YoY growth by 1-3% depending on the month, as can be seen in the chart below. However, we would be concerned if the SSE continues to fall. Our near-term outlook (Trade) for Macau stocks is favorable, particularly LVS, but if the SSE falls further, that would bring some uncertainty into the intermediate or Trend call. Our long term (Tail) view remains positive.