When Outback Steakhouse went private in 2006, then-Chief Executive Bill Allen extolled the virtues of a private structure, saying, “as a private company, OSI will have greater flexibility to focus on our long-term business improvement initiatives”. If Don Corleone was being pitched Bloomin’ Brands’ stock, he might say “what have I done to deserve such generosity?” Vito’s reservations, by our speculation, would be rooted in the 300 basis points of margin upside that Bain Capital and Catterton seemingly left on the table when bringing the company public again.

The prior incarnation of Outback Steakhouse, OSI, in the public markets, was a typical case of a restaurant management team attempting to maintain a growth multiple by overpaying for smaller brands. The difficulty involved in managing a portfolio of multiple brands as one company ultimately became too great (this may remind you of our thoughts on another casual dining name we are bearish on).

So, is the BLMN proposition analogous to Sollozzo’s solicitation to Don Corleone? Is there a Tattaglia family in the picture?

While the time the company spent as a private company clearly did not bring around the kind of changes that Mr. Allen suggested it would, the company is under new executive leadership that we believe has credibility with the investor community. This time around, the players are different and it will be critical that the company’s second stint as a public company does not end in a similar manner to the first. Still, as things stand, BLMN is a highly-leveraged multi-concept casual dining company that is stating its intention to be a more efficient and focused organization. There is definitely potential for this to turn out poorly.

We will be publishing more on BLMN going forward but for now, we would like to expound on three earnings drivers for the company.

1) 300 bps Adjusted EBITDA margin improvement from cost cutting and sales leverage by end FY14?

Management assured us on the earnings call that the margin improvement would be obtained primarily through Food & Labor efficiencies as well as sales leverage. Comparing BLMN to major casual dining peers it seems that the margin opportunity is sizeable. When contemplating how the gap will be narrowed, how attainable the opportunity is becomes less clear. If it were easy, surely the private operators would have taken that money off the table. The following are our two primary concerns from here:

- The industry’s outlook, along with BLMN’s mature store base, suggests to us that sustained acceleration in same-store sales is unlikely. Guidance for 2012 blended same-restaurant sales is 3%.

- Consumers are likely to face 3-4% food inflation in 2013, according to the USDA. With labor inflation running at roughly 1-2%, and Food & Labor being the primary source of margin expansion for BLMN, it seems that this goal will be difficult to achieve.

2) Unit Growth from Bonefish, Carrabba’s and the International division will drive top line

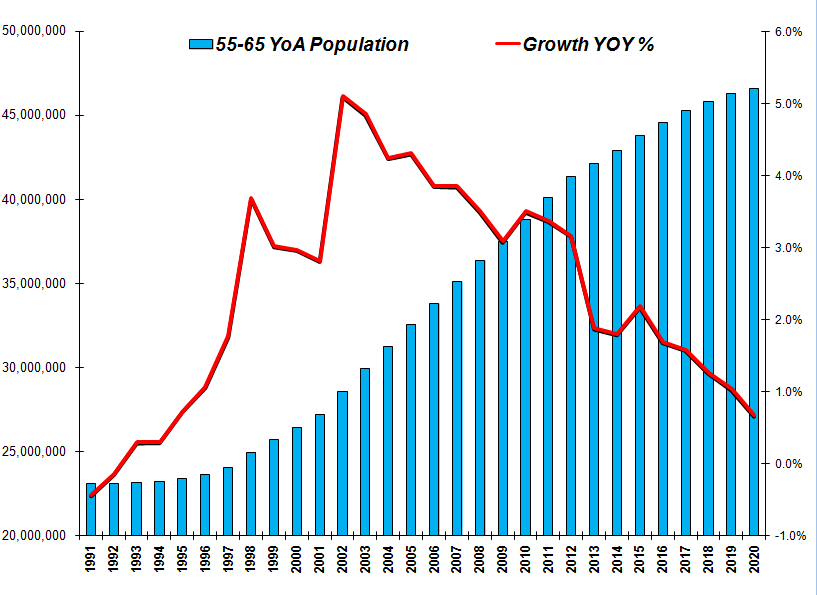

We are skeptical about aggressive unit growth within the casual dining space, particularly among mature chains, given the macro environment and the demographic outlook for key age cohorts such as those within 55-65 years of age. Our conversations with industry insiders corroborate this view; it is becoming more apparent that oversupply, stemming from years of restaurant executives being compensated to grow, has become a major issue in casual dining. With this in mind, we will be paying attention to incremental returns as an indicator of the investment worthiness of the smaller chains. Rarely, in casual dining, do multi-brand companies become bigger and better at the same time.

3) Lunch being introduced at Outback will spur same-restaurant sales growth

The company claims to have analytical support to back up its claim that lunch at Outback makes good business sense. On the surface, it seems to make sense, particularly during weekends but this day part is more competitive and performance during the day-part can often play a key role in shaping consumer perception of the brand.

The argument for attacking lunch seems to hinge on two factors: it’s better than leaving the store dark and it’s accretive to margins on an enterprise level. However, from the perspective of the Outback brand it’s dilutive to margins as lunch carries lower margin than dinner. This sales-building initiative, that lowers the margins of the overall business, may not be as beneficial for shareholders as it may first seem.

Conclusion

There has clearly not been much progress in fixing this company since it was taken private in 2006 and casual dining faces stiff headwinds from a demographic and economic perspective. It seems to us that the company is dependent on strong sales and an opportunity to implement efficiencies in the P&L. The macro environment, via a poor jobs market and accelerating food inflation, may make these goals difficult to achieve. We’re staying away from this name for now.

Howard Penney

Managing Director

Rory Green

Analyst