FedEx (FDX) slashed its quarterly outlook yesterday, citing the global economic slowdown as a catalyst for slowing growth. That made us look at the relationship between FedEx shipping volume and Thermo Fisher Scientific’s (TMO) industrial focused Analytical Instruments business. With TMO shares up +27% year-to-date and up +16% alone in the last 3 months, the company is vulnerable to a move to the downside.

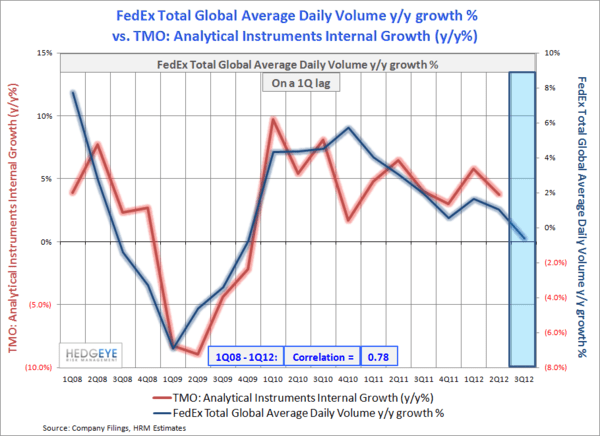

In the FedEx press release, FedEx only commented on their earnings guidance which they reduced to $1.37-$1.46 from their June guidance of $1.45-$1.60. With the off-month reporting, we looked at both FedEx as a leading indicator for TMO (0.78 correlation) and peer UPS coincidently, (0.73 correlation). Take a look at the two charts below. Both the FDX and UPS charts show a decline in both business segments from Q212 onward.

If shipping volumes are the indicator of what’s to come, things are not bright for TMO going forward. We are currently short TMO in our Healthcare position monitor.