“You can’t build a railroad from nowhere to nowhere.”

-Cornelius Vanderbilt

While I am sure some partisan politician had a rebuttal to one of America’s most successful businessman’s thoughts on the matter at the time, that remains one of the most poignant risk management quotes from 1873.

“The Panic of 1873 began shortly before 11AM on Thursday, September 18, when the Wall Street branch of the nation’s most prestigious private banking house, Jay Cooke & Associates, unexpectedly ushered its customers out and then literally closed its doors, signaling it was bankrupt.” (John Lubetkin, in Jay Cooke’s Gamble)

Yes, I know. We have centrally planned our way to never worrying about fundamentally flawed policies and business risks again in this country. Right?

Back to the Global Macro Grind…

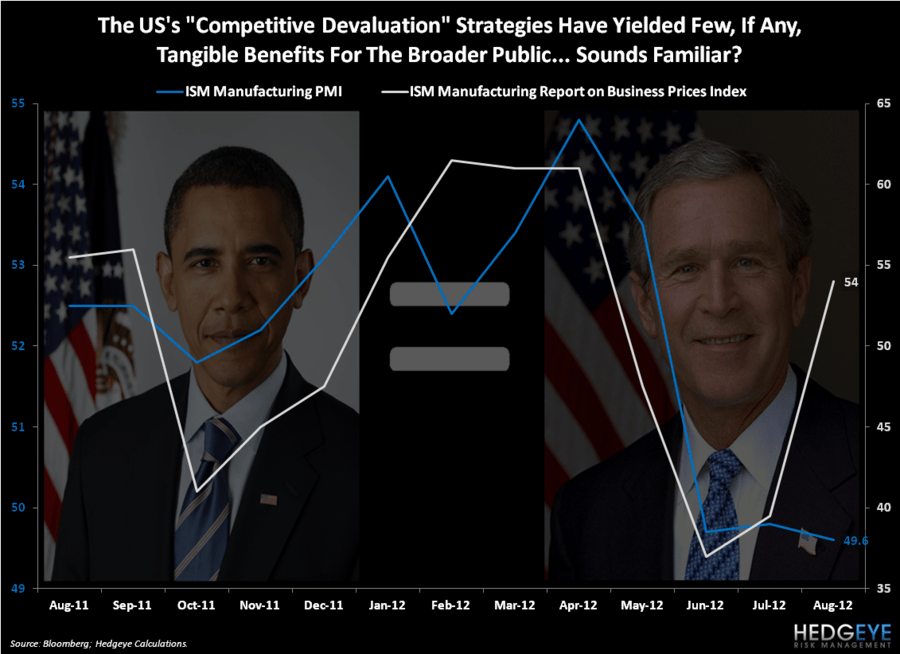

While the Keynesians are storytelling about needing “more time”, the fact remains that Policies To Inflate haven’t done a darn thing they were designed to do:

- Debauching the Dollar was supposed to generate “export and manufacturing growth”

- Economic growth slowing was supposed to be met with a “growth recovery” that lasted more than 3 months

- Corporate growth and earnings were supposed to remain at all-time highs; hiring would follow

Political theory versus economic reality: let’s fast forward to, well, yesterday:

- America’s ISM Manufacturing Survey for August slowed for the 3rd consecutive month to 49.6 (signaling economic contraction)

- The Prices Paid component of the ISM survey ripped higher month-over-month to 54 vs 39.5 in July (+37% sequentially)

- Fedex, a $28B US company, pre-announced another revenue and earnings miss after the market close

But no worries…

We need to beg for more of what has not worked – must do something – need more stimulus – need more time so that we can build elevated stock market prices, on no-volume, into the market’s risk matrix so that we can get from nowhere to nowhere, again.

To review what the aforementioned data points mean to real business people in this country in September 2012:

- Global Demand (yes, including Asia) slowed in August as inflation, on the margin, rose

- As inflation (prices paid by manufacturers, consumers, etc.) rises, on the margin, profits slow

- As profits slow, hiring slows – again

This isn’t a vicious cycle anymore. It’s just a sad one to watch. How definitively insane it is to watch people make the same mistakes over, and over, and over again?

I know, I know. After they are wrong on growth, and half-baked right on how bailout policies keep market prices up for 6 week intervals, perma-bulls say “the market is up and stocks are cheap.”

Well, there’s a little fibbing in that too. Since the 2007 top (1565 SPX) and lower 2012 high (1419 SPX) that followed it, stocks are down – and they’re expensive, if you don’t use the wrong growth and earnings numbers.

So where does the great Keynesian economic vision of building bridges and railway tracks to end demand that’s slowing take us? I don’t know. And, if they tell you the truth, neither do they.

My immediate-term support and resistance risk ranges for Gold, Oil (Brent), US Dollar, EUR/USD, 10yr UST Yield, and the SP500 are now $1, $111.51-115.78, $81.19-81.98, $1.24-1.26, 1.54-1.63%, and 1, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer