Darden’s Annual Report arrived this past weekend and made for some great reading. The primary takeaway for us was that the “growth” ethos at Darden is as entrenched as ever. Against a backdrop of sustained traffic declines, it is jarring to read the following sentence: “Our brands have strong individual and collective growth profiles”. We think management is setting itself up to miss expectations.

If you have read our Darden Black Book you are aware of our conviction that the continued acceleration of Darden’s new unit growth over the past couple of years has served to mask evidence of a secular decline in the company’s two most important brands. The Letter to Shareholders in the Annual Report contains no evidence of management slowing growth any time soon. Management’s growth targets are bold to say the least. How they get there while maintaining the financial health of the company remains to be seen.

This is not the first time we’ve held a view on a stock that is diametrically opposite to that of management. MCD and SBUX were two names I went against the grain on in 2002 and 2006, respectively. Of course, we’ve been wrong before but feel strongly about our thesis on Darden. Conversations with clients and industry experts, without exception, have increased our confidence in our thesis. This thesis is not going to play out today or tomorrow; we are aware that we are early on this one.

It’s Not The Economy

Darden’s annual report suggests that management sees the economy as the biggest issue facing the company and, furthermore, sees weakness in trends at its core brands as being transitory in nature. The longer-term view, as defined by the data, suggests an altogether different story. On a very basic level, we believe that companies acknowledging their issues are generally more apt to arrive at solutions. The traffic trends at Olive Garden and Red Lobster clearly are demanding action of management. The economy is undoubtedly a factor but the poor performance of the “Big Two” versus the Knapp Track casual dining benchmark is a clear indication that the company’s sluggish traffic trends are not entirely attributable to the macroeconomic environment. The data points that we are pointing to – traffic trends – as a primary reference for our thesis are indicative of, at least in part, self-inflicted wounds.

If the company has become dependent on growth as a drug for all ailments, the Annual Report suggests that management does not seem to have freed itself from the “denial” stage of its addiction. Stating that the “core brands remain highly relevant to restaurant consumers” can be supported by pointing to the average unit volumes at Red Lobster and Olive Garden as being some of the strongest in the industry. We believe this statement to be misguided, however, when considering same-restaurant sales trends – a far more relevant metric when assessing relevance to the consumer:

- Red Lobster’s two-year average same-restaurant sales have declined over 10 of the last 16 quarters

- Olive Garden’s two-year average same-restaurant sales have declined over 8 of the last 16 quarters.

Red Lobster’s positive traffic trends in FY12 were driven largely by aggressive discounting while Olive Garden’s most recent data is deeply concerning. The charts below illustrate the cumulative price and traffic trends for Olive Garden and Red Lobster relative to FY08. Price has been taken steadily while traffic has generally trended lower with the exception of brief spurts into positive territory driven by LTO discounting. Our concern is that the core brands of Darden, whether deemed relevant or not by management, are losing appeal for consumers as time goes by.

The remedy for what ails Olive Garden, a system with 430 restaurants in need of remodeling, is not going to materialize imminently. We believe that more dramatic measures may be needed to boost the competitiveness of the “Big Two”.

What’s Consistent About Darden’s Margins?

The Darden Annual Report states, “our success will be driven by strong total sales growth and consistent margin expansion as we leverage our collective experience and an increasingly efficient support platform.” We would like to address this quote in two parts.

First: “consistent margin expansion”.

Darden’s EBIT margins are consistent in their absolute level but they are not expanding. Contributing to Darden’s strong EBIT margins are the company’s restaurant level margins which were 23% in FY12. Darden stands alone among the companies we follow in terms of its margins but we find it difficult to believe that significant expansion in that metric is likely from here given the reality of Olive Garden and Red Lobster’s traffic trends.

The outlook for margins is far more important than what is in the rear-view mirror and we contend that the need to improve the relative value proposition at Olive Garden and, to a lesser extent, Red Lobster is likely to lead to an easing in pricing trends. Maintaining restaurant operating margins under this scenario will likely be difficult. At the Analyst Meeting in February, management was vocal about lower menu prices improving traffic and allowing Darden to leverage G&A, thereby offsetting the restaurant operating margin decline and even expanding EBIT margins.

Second: “our success will be driven by strong total sales growth”.

Total sales growth has been strong but rather than focus on total sales or average unit volumes, we focus on traffic and comparable-sales trends as true indicators of top-line health. Leveraging the balance sheet to buy top line growth is not a winning strategy, particularly for a stock whose ownership seeks stability and yield. Traffic trends are expected to decline in FY13.

Operating Cash Flow Targets a Little Rich

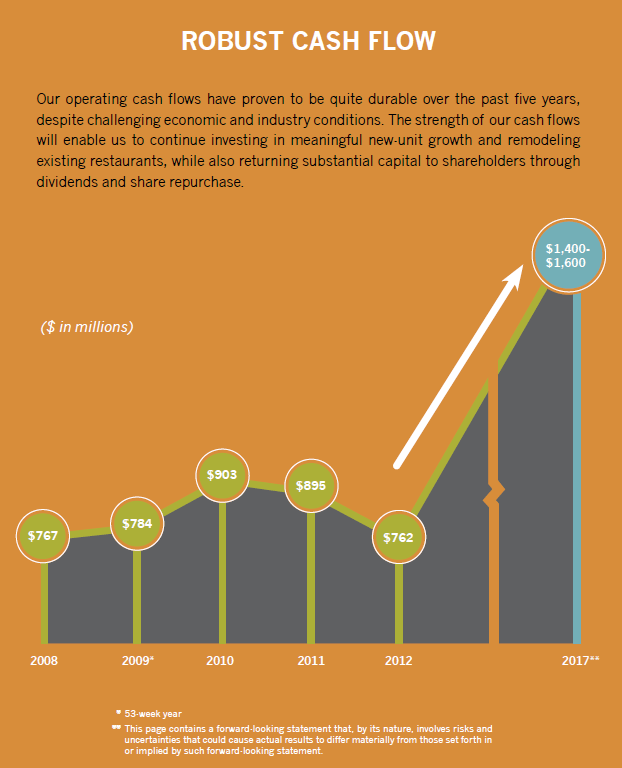

Darden is projecting a doubling of its operating cash flow over the next five years despite its best-in-industry margins being at peak levels with traffic trends slowing. This is a lofty goal when we consider that operating cash flow has declined 1% since 2008. How does the company get there?

The chart, above, taken from the company’s Annual Report, shows that the company is guiding to operating cash flow doubling to $1.4-1.6 billion by FY17. The company is also guiding to sales of $11.5-12.5 billion in the same year. Looking at operating cash flow margin over the last five years, it seems that FY17 will have to be a very good year for the company to hit its implied target of 12.5%. Over the past five years only once, in FY10, with 12.7%, did the company achieve or better the operating cash flow margin that is implied by the FY17 estimates. FY10, it is also worth remembering, saw food and beverage costs decline 6.8% in what was the only year of the last five during which this cost declined for Darden.

In order to double its operating cash flow over the next five years, the company will require a sizeable recovery in sales at its two largest brands. At a minimum, we believe that Olive Garden is two years away from a sales recovery beginning. Over the past five years, from FY08 through FY12, the company has spent $2.6 billion to generate an incremental $242 million in EBITDA.

Big Promises

The company has made the following commitments to its shareholders for the period ending FY17.

- SRS of 2-4% with 1-2% in FY13

- 500 new stores or ~$3.4 billion in capex (Hedgeye estimate)

- 2x operating cash flow to $1.5 billion

- Cumulative dividends and share repurchases of $3.2 billion

We believe these are tall orders, individually and collectively, for the company to deliver. We will address these targets below:

Same-restaurant sales of 2.4% are dependent, according to management, on “normal” economic conditions (whatever that means). Historically, the company has had pricing of 2-3% included in its comps but we believe that the primary brands’ pricing power will be diminished going forward. Traffic in the casual dining industry declined 40 basis points in 2011 and 90 basis points over the last twelve months, according to Malcolm Knapp’s Casual Dining Same-Restaurant Sales Index.

New restaurant growth is a key focus for Darden and the company has sufficient cash flow to grow 500 units over the next five years. The more salient question is whether or not the company should allocate that capital to 500 new units over the next five years. We believe the company should slow growth given decelerating Returns on Incremental Invested Capital.

Operating cash flow is unlikely to double in five years given the current run-rate of capital spending. We anticipate roughly $3.4 billion of capex between now and the end of FY17. As we highlighted earlier, operating cash flow margins need to expand significantly (300 bps) from FY12 to FY17 in order for operating cash flow targets to be made, assuming the sales guidance comes to fruition.

Returning cash to shareholders is a key Darden selling point. The 3.8% dividend yield is highly appealing to investors and, since FY08, the company has raised the dividend 150% while EPS has grown 31%. More importantly, the operating cash flow of the company has declined 1%, from $767 million to $762 million, between FY08 and FY12. In order to pay the dividend and accomplish other capital-intensive goals, the company has burned through $689 million in cash. In FY12, dividend and capital spending accounted for 113% of operating cash flow. As a result, adjusted debt/EBITDA at the beginning of FY13 was 62% (prior to the recent acquisition), leaving the company little room to maneuver from an operational perspective and raising the stakes should margins decline. The company’s long-term goal of returning $3.2 billion in cash to shareholders is dependent on expanding operating margins. If this does not materialize, either the dividend or capex will need to be cut.

Conclusion

Senior management at DRI has a very ambitious 5-year plan, where there is very little room for error. As we see it for management to accomplish this 5-year plan the following must happen:

- RL and OG need to improve traffic trends ASAP with no margin degradation.

- The company needs to leverage 2-4% same-store sales with little pricing

- Enterprise wide cost cutting is must

- Real estate site selection must be perfect and new unit sales trends must be above average

- Margin expansion is a must and there is little room for food or labor inflation (the impact of the new heath care will likely be inflationary)

- The company must overcome significant macro/demographic headwinds

- Darden must protect share against some rejuvenated competitors in EAT and BLMN

- Margins must be maintained as increased leverage is going to limit the operating flexibility of the company

We believe that Darden could, even while achieving its cash flow targets, burn through between $550-650 million in cash between FY13 and FY17. The current path for Darden looks to be fraught with risk and largely unsustainable in its current form.

Howard Penney

Managing Director

Rory Green

Analyst