“In many cases, they simply walked away.”

-Hampton Sides

That’s a quote about the Anasazi people of Chaco Canyon in Chapter 31 of Blood and Thunder. By 1150 AD, “just as quickly as they had burst upon the scene, the Chacoan culture ebbed… the Anasazi had overfarmed, overhunted, and overlogged.”

After a 200 year ( AD) “cultural boom that has no parallel in North American pre-history… archeologists have come to call this the Chaco Phenomenon… this environmental upheaval led, predictably enough, to a social upheaval.” (pages 266-267)

Whether some study history doesn’t matter. Markets do. They rise and fall. For centuries, ideologies, regimes, and civilizations have lived and died by the sword of evolution. Just when you don’t think it could never happen to yours, it starts happening.

Back to the Global Macro Grind…

How long can Keynesian governments over-spend, over-consume, and over-promise on bailout resources that they do not have?

I don’t know. And neither did Jim Rickards on our Currency Wars conference call yesterday. What we both agreed on, however, is that within the framework of considering global markets as a complex system, we’re getting real close to the tipping point.

Rickards explained it using “critical threshold” math. I always discuss it internally within the Chaos Theory of emergent properties triggering phase transitions. For those of you who are Keynesians or Monetarists, we’re talking a different risk management language here. Alongside physics, applied math, etc., we’ve chosen to think outside the Western academic box. We’ve evolved.

To simplify the complex, a “phase transition” is the transformation of a dynamic system (global markets, across asset classes) from one state to another. Pundits don’t get why they call it this, but they call it something like “risk on, risk off.”

Unfortunately, phase transitions don’t happen like the Karate Kid learning how to wax. There is no centrally timed “on, off.” There is no “smoothing mechanism” or certainty in analyzing when emergent properties (risk spreads) move into a phase transition.

In thermodynamics, you can understand what a phase transition is by reading an 8th grade Chinese textbook (they have them in English too). “For example, a liquid may become gas upon heating to the boiling point.” (Wikipedia)

What’s the market’s boiling point?

To answer that question, many people who have not evolved their process in this business would answer using the US stock market and maybe a 50-day moving average sprinkled with some storytelling dust.

*Risk Manager Note: the US stock market is not the dynamic and globally interconnected currency, commodity, bond, etc. market that our 27 multi-factor, multi-duration model is writing about every day.

Jim Rickards is very good because markets have humbled him enough over the years to answer the aforementioned question with “I don’t know.” That’s also a cornerstone of what we (Chaos and Complexity Theorists) do vs. what they (Keynesian Policy Makers) do.

We Embrace Uncertainty.

One suggestion I had to answering the most frequent question I get from clients (again, what’s the boiling point, or point when this entire centrally planned gong show of broken policy promises implodes) was measuring Spread Risk in key Global Macro relationships:

- The long-term spread between Money Supply (rising as they print money) and Velocity of Money (falling, fast)

- The long-term spread between the US Dollar and the CRB Commodities Index

- The long-term spread between the SP500 priced nominally versus priced in Gold (see Rickards’ Chart of The Day)

I’ve probably geeked out enough on the math this morning, but since Paul Ryan is going all-math on CNN’ers, I’m cool with it. I’ll also leave you this morning with more questions than any of us have answers.

But that’s cool too - if that’s the story of your professional life, you really are constantly learning and evolving.

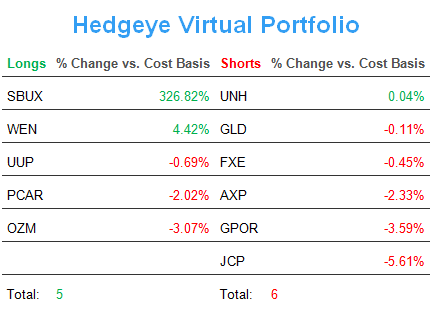

The Hedgeye Portfolio is beta adjusted net short for this morning’s US market open. We continue to think you sell stocks and commodities at VIX 14-15 and buy bonds there too.

Timing matters; especially when entire populations of investors are Walking Away from something that’s been abused and broken – the market’s trust.

My immediate-term risk ranges for Gold, Oil (Brent), US Dollar, EUR/USD, 10yr Treasury Yield, and the SP500 are now $1, $111.79-113.76, $81.11-81.97, $1.23-1.26, 1.58-1.71%, and 1, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer