If there is one thing we have noticed about tropical storms and hurricanes, it is that when they are built up aggressively by the main stream media they typically disappoint in terms of their scale. With comparisons to Katrina, tropical storm Isaac may already be in this category of being overhyped. Nonetheless, Isaac is on his way and will, at the very least, disrupt oil and natural gas production in the Gulf of Mexico for a period of time.

According to the National Hurricane Center (NHC), Isaac is very likely to evolve from a tropical storm into a hurricane over the warm waters of the Gulf of Mexico. The current projection from the NHC is that Isaac will be a Category 1 hurricane, based on the Saffir-Simpson scale of hurricane activity, with winds between 74 and 95 miles per hour. Katrina was a Cat 5 storm with winds above 157 miles per hour. The unseasonably warm temperature in the Gulf of Mexico is the wild card that could strengthen Isaac beyond Cat 1.

The computer models being run by the NHC, as outlined in the map below, show Isaac making landfall by late tomorrow evening or early Wednesday morning. By midday Wednesday, the storm will be fully landed. The likely landing location is the 300-mile stretch from the bayous of southwest New Orleans to the edge of the Florida panhandle.

Even if Isaac does take land as a more moderate storm, it appears to have a similar trajectory as Katrina and may well be on track for New Orleans by late Tuesday or early Wednesday based on its projected speed of 14 miles per hour. A key risk being touted by the NHC is that Isaac may make landfall coincident with high tide, which would lead to excessive flooding.

The larger risk, especially for an increasingly tepid consumer, is the impact of the storm on energy prices over the next couple of months. As it relates to exposure from Isaac:

- The Gulf Coast is home to 23% of U.S. oil production and 44% of refining capacity;

- In total, more than 346 oil platforms (58% of the total) and 41 rigs (54% of total) have already been evacuated;

- Currently, 1.0MM barrels per day is shut in (78% of GOM oil production) and 48% of gulf natural gas production ; and

- Based on Hedgeye’s count, more than 1.1 million barrels of refining capacity will be taken offline in Lousiana, including a 490,000 barrel facility in Garyville, Lousville.

On the positive side of the equation, most refiners are built to withstand up to Cat 2 hurricanes. Therefore, unless Isaac accelerates beyond its current Cat 1 projection, long term damage to refiners or oil production facilities is unlikely.

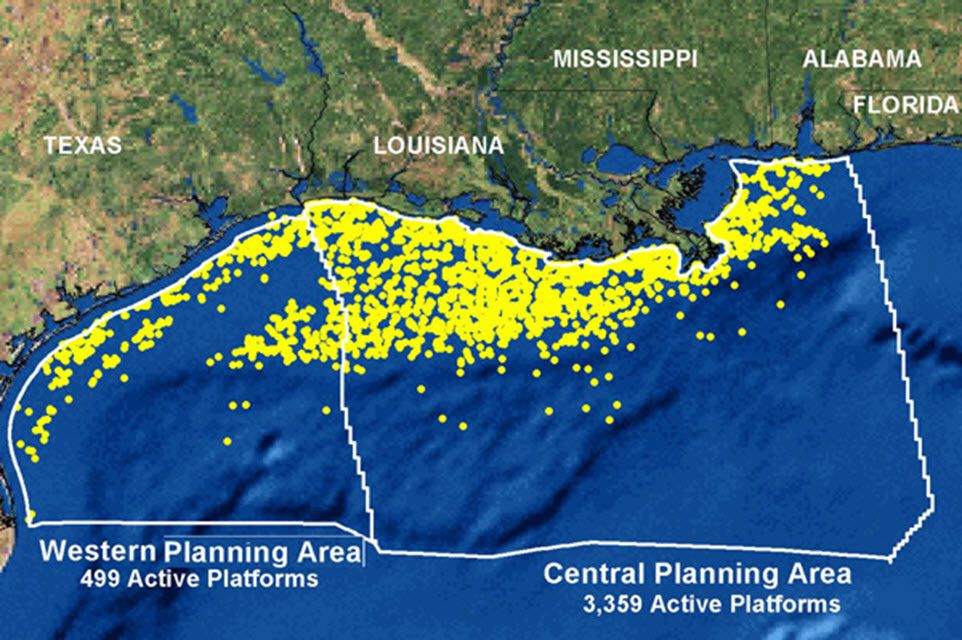

In the chart below, from Forbes, we show the active oil platforms in the Gulf of Mexico. Based on Isaac’s current path, the storm will travel directly through the heart of the oil producing region of the GOM.

In the last chart we highlight the spiking of gasoline prices that occurred in conjunction with Katrina. Gasoline prices spiked almost 50% and remained elevated for a couple of months. With national gasoline prices, according to the most recent data from the Energy Information Administration, at $3.72 per gallon, a price shock from this level would be catastrophic for the U.S. consumer. Undoubtedly, it would also create a very negative situation for the President Obama heading into the November election.

So, even if Isaac is being overhyped, the storm’s path and intensity over the next two days will be critical in assessing whether there will be long term damage and subsequently elevated energy prices in the coming months.

Daryl G. Jones

Director of Research