Mass gaming revenue has been on a tear yet visitation growth has been fairly modest. What’s going on? Aside from misleading visitation data which we will get to, the Macau Mass tables have been holding at an increasingly higher rate. As the following chart shows, average Mass hold percentage grew from around 18% in 2Q07 to over 27% in Q2 2012 – and it’s not luck.

So what’s driving hold percentage higher? The consistency of the up move suggests luck is not a factor. We believe players are playing longer (more hands) and bringing more cash with them. Our experience in Las Vegas is that hold moves higher in good economic times and down in bad. Unlike the VIP business where hold is measured as a % of roll, there is no way to measure roll in the Mass sector so the denominator in the hold calculation is simply cash converted to chips. So hold will theoretically climb if velocity of play goes up. On the other hand, if players are cautious they may still take out the same amount of chips but spend less time gambling. Thus, the denominator would be the same but the player would lose less.

There are likely other factors at work driving Mass hold higher. Refined rewards programs and customer database marketing have been providing more and better incentives for longer play. A better mix of higher end players also helps. We’ve seen this occur in other more mature markets as well.

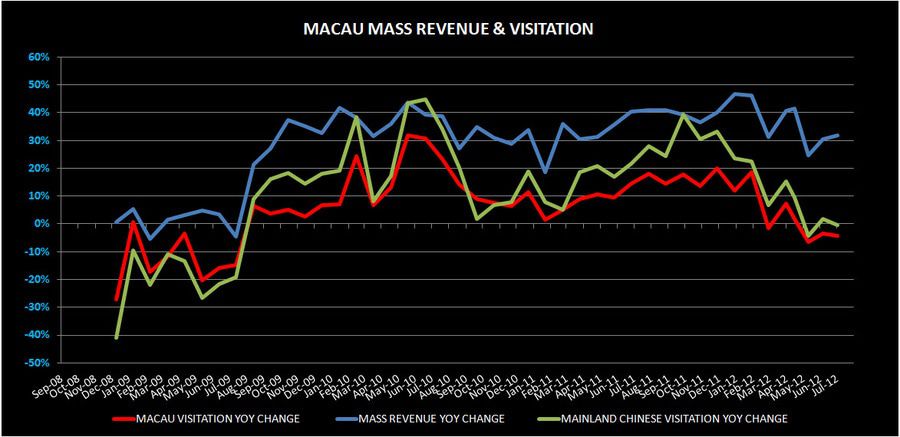

Higher hold is not the only driver. As seen in the above chart, estimate Mass volume has been growing nicely, albeit below the rate of revenue growth. Yet visitation growth remains modest as shown below:

So what’s causing this phenomenon?

- Higher Mass hold percentage discussed above

- Hotels running at high capacity on the weekends so lower-end Mass getting shut out

- Better yield management from the casinos so lower-rated players getting less

- Higher table minimums – both City of Dreams and Galaxy Macau have successfully pursued this strategy to focus on the Premium Mass business

- More of a Mass to VIP mix in the hotels – again a yield management strategy which improves margins

- Visitation data is not perfect – we’ve heard that the Macau government has cut down on its citizens crossing the borders for short visits to buy cheaper goods. Visitation data reflects re-entry back into Macau. Also potentially impacting visitation is fewer visas available for tour groups that are primarily non-gaming visitors.

- Visitation from outer provinces is growing but lower-end players in the close-in provinces are getting shut out due to yield management