Idea Alert: Keith bought WEN in the virtual portfolio this morning.

I believe that Wendy’s is a company heading in the right direction but it’s going to take years to fix. In the short run the stock will make a better “trading stock” than a long term investment. For longer-term investors we would look elsewhere for exposure to the QSR category at this point in time.

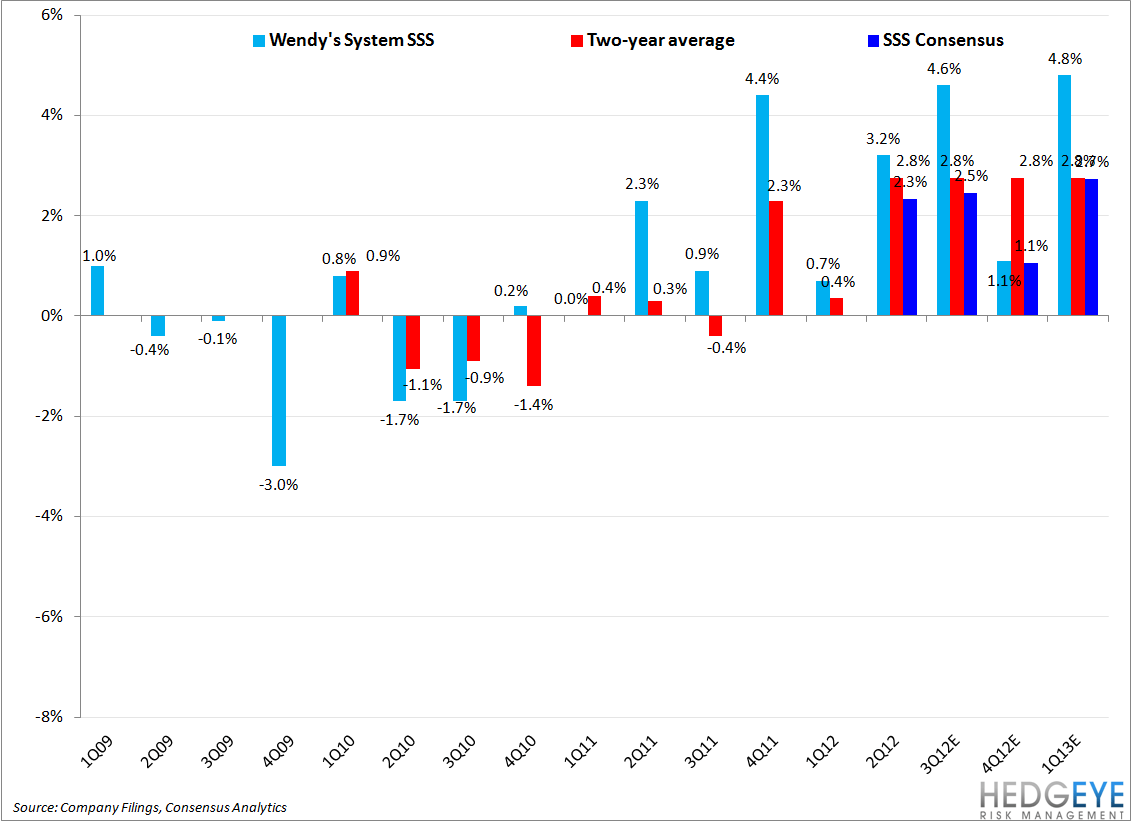

Currently, we are seeing an uptick in same-store sales since the end of the second quarter. Currently consensus estimate have WEN posting system-wide same-store sales of 2.5% (company SSS at 2.5% and franchised at 2.6%). We believe that the current trends are several hundred basis points above those numbers.

For a trade the stock could head back to $5.

Longer-term., reimaging remains a dark cloud hanging over the Wendy’s story and we expect the stock to remain range-bound until investors gain more visibility as to the timeline and the cost associated with this core component of the brand revitalization effort. There will be a time to get behind this stock but, for the foreseeable future, we will stay on the sidelines until we gain clarity on the company’s timeline and future cash flow generation.