"I know a lot of people have very strong and definite plans that they've worked out on all kinds of things, but we're subject to a tremendous number of outside influences and the vast majority of them cannot be predicted. So my idea is to stay flexible."

- Henry Singleton

I have to admit, I didn’t know who Henry Singleton was when I first read the quote above – I just really liked the quote. Then I read a little bit about Mr. Singleton and I really liked him too. He was what I would call a great American.

Singleton graduated from the Naval Academy in 1940 and went to work as an electrical engineer. As the United States upped its involvement in World War II, Singleton was eventually sent to Europe as a member of the Office of Strategic Services, which was the forerunner to the CIA.

After serving his country, Singleton returned to the U.S. to get a graduate degree in electrical engineering from MIT. He would then make his way out to California where he and a former Naval Academy roommate, with the backing of legendary venture capital investor Arthur Rock, would start Teledyne, a company that had decades of success before being acquired by Allegheny Steel. None other than Warren Buffett once said:

“Henry Singleton of Teledyne has the best operating and capital deployment record in American business.”

Lofty praise, indeed.

One of Singleton’s keys to success was his willingness to be flexible. Nothing could be more accurate for those of us that actively invest in the stock market. The ability to change your mind and change your exposures on new information is a critical to succeeding as a money manager.

Yesterday, I did a brief interview on National Public Radio. The key question they wanted answered was why August was so quiet and whether that meant things were getting better. Now perhaps I’m being a little inflexible, but my response was that they shouldn’t confuse absence of news with good news. In fact, as we look forward there are a number of major events that we need to manage risk around, such as:

- The U.S. Election – As we’ve noted, this race is basically a dead heat with Romney likely doing a bit better than many polls indicate based on higher voter engagement for Republicans. We are confident in saying, especially with the addition of Paul Ryan to the ticket, that the economic policy outcomes will be very different under a President Obama or President Romney.

- The U.S. Debt Ceiling – Do you remember this little critter last summer that led to a dramatic sell off in risk assets and a literal shutdown in Washington D.C.? Well, it’s going to become an issue again very soon. According to analysis from our healthcare team, the U.S. Treasury will issue $592 billion in debt through year end, which will put them in breach of the debt ceiling of $16.4 billion sometime before 2013.

- Fiscal Cliff – It’s funny how we are hearing less and less about the fiscal cliff these days, since the issue hasn’t gone away. In 2013, we have the toxic short term growth combination of higher taxes and lower government spending coming our way (less government spending will be good in the long run, of course). Reasonably this could be a 2% plus headwind to economic growth next year. The non-partisan CBO actually has 2013 growth pegged at an anemic +0.5% in 2013.

- Japanese Debt Ceiling Debate – Just because Japan is in a different time zone, doesn’t mean it doesn’t exist. Currently, legislation to enable the Japanese government to sell debt to finance 40% of the federal budget is stuck in the upper house as the opposition party is attempting to force Prime Minister Nodo to fix an election date. Japan’s government could run out of money by October if this legislation is not passed.

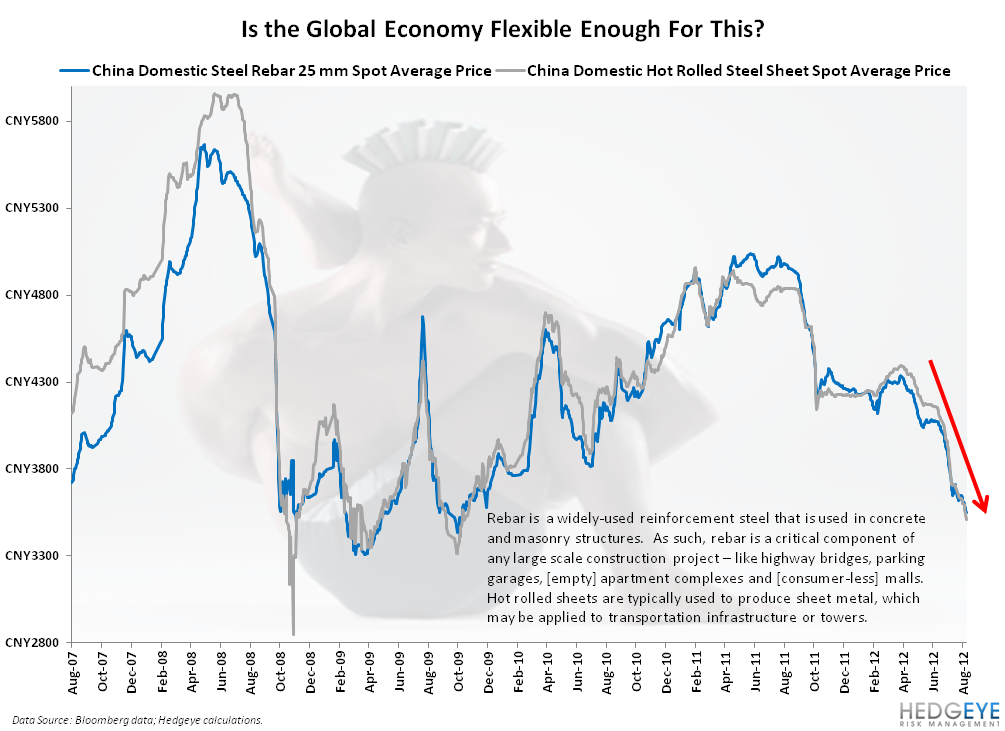

- Chinese Growth – I highlighted the Chinese flash PMIs yesterday that showed inventories building and sales declining heading. In the Chart of the Day, we show Chinese steel prices that illustrate much the same story economically. Rebar, in particular, is required for large scale construction and to the extent prices are declining it bodes poorly for economic activity and suggests the upcoming quarters will be replete with negative economic data.

- European Debt – The Eurocrats are on vacation so the news flow has been minimal and, on the margin, that’s been positive. That said, nothing has been solved and we will likely see more “solutions” and “summits” in the coming months. In fact, news out this morning has the German finance minister stating they will be preparing for a scenario in which Greece leaves the Eurozone.

It’s Friday, so I do want to leave you on a more cheery note heading into the weekend, so I decided to leave out my 7th potential catalyst, which would have been the potential for an Israeli strike on Iran this fall. Certainly, oil is signaling something along these lines lately.

On a much more cheery note, my colleague Jay Van Sciver, our Industrials Sector Head, will be joining our client call this morning to discuss his sectors and one of his favorite names, PACCAR. Van Sciver has a differentiated view on the upcoming trucking cycle, which is likely to lead to fewer truck sales and more parts sales. Get this, truck OEMs, such as PACCAR, actually make more money selling parts. If you can’t join us for the call this morning, ping and get on a call with Van Sciver. His long call on PACCAR is almost as compelling as is short case on United Airlines.

Our immediate-term support and resistance ranges for Gold, Oil (Brent), US Dollar, EUR/USD, 10yr UST Yield, and the SP500 are 1, 113.96-116.21, 81.28-82.13, 1.23-1.25, 1.62-1.75% and 1.

Enjoy the weekend!

Keep your head up and stick on the ice,

Daryl G. Jones

Director of Research