This note was originally published at 8am on August 10, 2012 for Hedgeye subscribers.

“Observe due measure, for right timing is in all things the most important factor.”

-Hesiod

Efficient market folks say they can’t time markets. Take their word for it. It’s our job, not theirs.

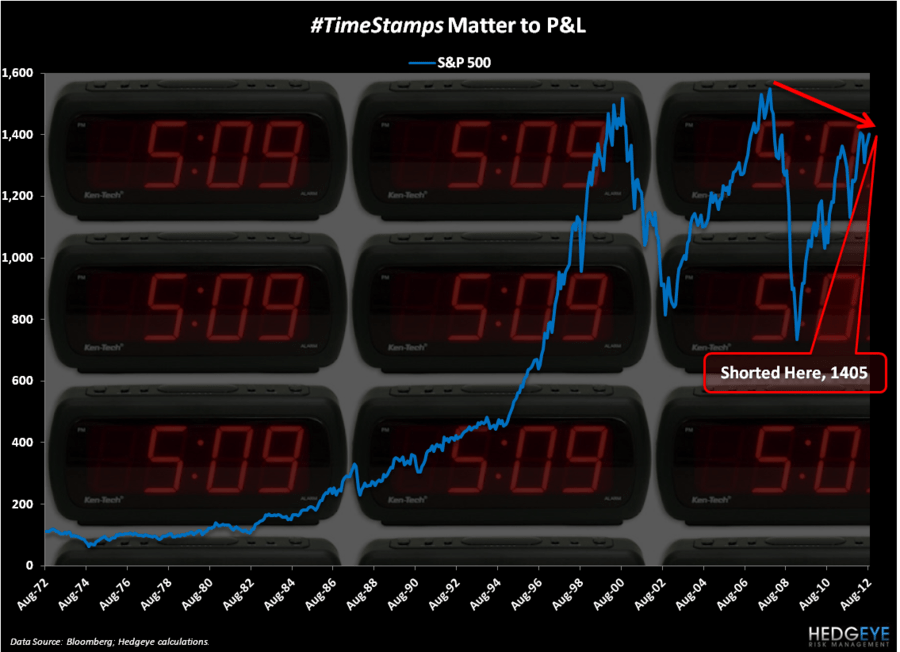

Whether you practice the art of short selling in gnomic, hymnic, or genealogical form, at some point in the decision making process we all have to do the same thing – timestamp our position.

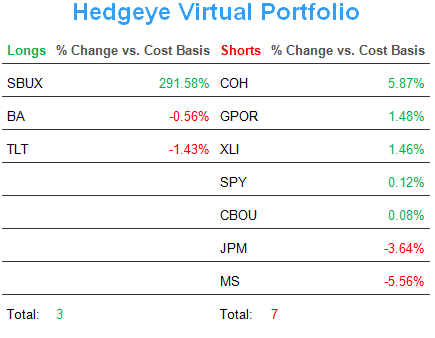

We waited, watched, and finally re-shorted the SP500 yesterday at 10:21AM EST (1405). Given all the perma-bullish narratives I’ve had to listen to for the last few weeks, I must say I enjoyed the experience quite thoroughly.

Back to the Global Macro Grind…

To timestamp or not to timestamp, remains the question. All of you who do this with real money understand the concept obviously. Timing stares at you from your P&L every day. For the Old Wall’s finest strategists, the whole accountability exercise still appears to be quite foreign.

If you’re one of the many non-timestamping strategists who had a 3% US GDP growth forecast and 1500-1600 target for the SP500 back in March, you had the entire 2012 fundamental thesis wrong. In order to remain bullish, the best move from here is to beg for bailouts and just change your thesis entirely because the “market is up year-to-date.”

Since the March 26th YTD high for the Russell2000 (+5.5% higher at 846) and the April 2nd YTD high for the SP500 (+1.2% higher at 1419) if nothing else, we’ve been consistent with both our research call (#GrowthSlowing) and our risk management process (#timestamps).

Looking back at the tapes, since February 15th this will be the 9th time we have made a risk management call on the SP500 itself without violating Rule #1 (don’t lose money). We’ve shorted it 8 times and bought it once (bought SPY on May 17th when plenty a March Perma-Bull was in the fetal position).

I’m not trying to evangelize or puff out my chest here. We haven’t killed it with all these calls. They haven’t been the worst timed calls to land in your inbox either. They aren’t meant to be anything other than immediate-term risk signals (which go both ways).

I’m just reminding you that there are some firms in this industry that have at least attempted to evolve the research and risk management process while many haven’t changed a darn thing.

Maybe this time we’ll be wrong. Maybe we’ll be right. The only thing I can tell you is that there will be no maybe when the position is closed.

Timing Matters. In some parts of this country, so does winning and losing – and being held accountable to both.

My immediate-term risk ranges (support and resistance) for Gold, Oil (Brent), US Dollar, EUR/USD, and the SP500 are now $1603-1624, $108.96-114.11, $81.95-83.01, $1.20-1.23, and 1388-1405, respectively.

Best of luck out there today and have a great weekend,

KM

Keith R. McCullough

Chief Executive Officer