How Does the Fed Measure Up as a Job Creator?

According to the Federal Reserve's website, one of its statutory objectives established by Congress is "maximum employment". The other two are stable prices and moderate long-term interest rates.

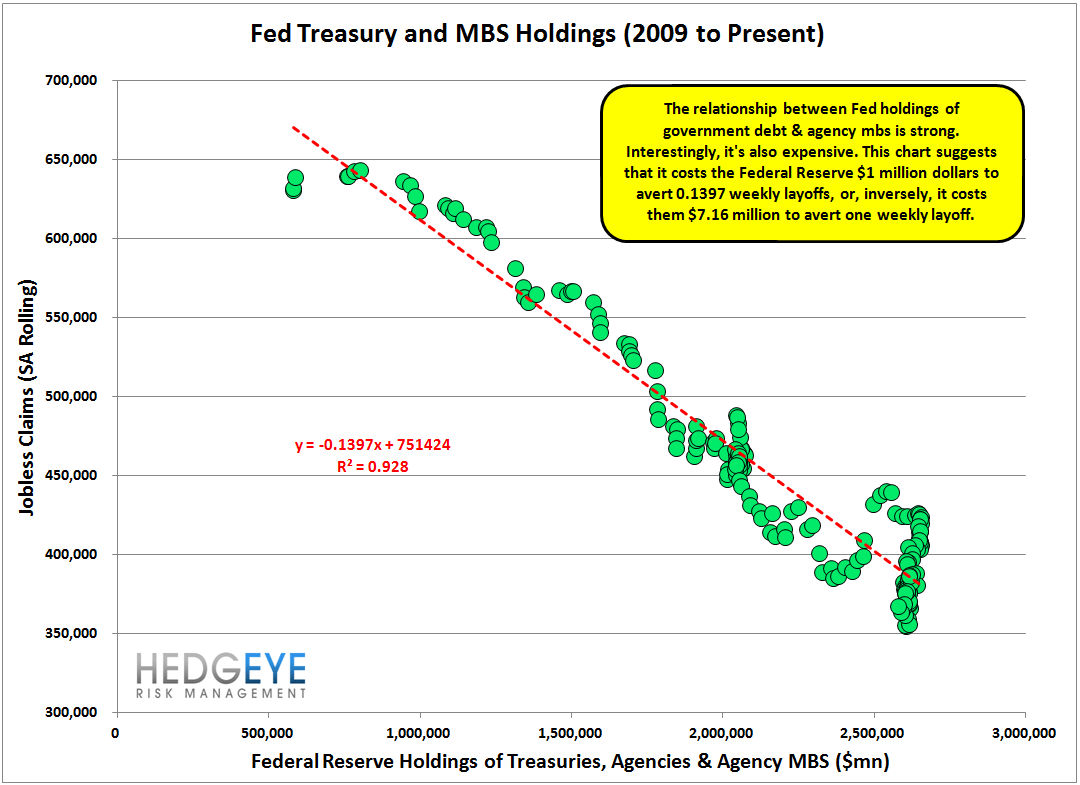

The chart below suggests a strong relationship exists between Federal Reserve securities holdings (QE) and employment. On the x-axis we're plotting Fed holdings of treasury, agency and agency MBS securities while on the y-axis we're showing rolling initial jobless claims. This is weekly data going back 42 months, which corresponds to the beginning of QE1. The R-squared is relatively high at 0.928, suggesting that if there's a causal relationship, then changes in the level of Fed holdings of government and quasi-government debt explain about 93% of the change in the level of jobless claims.

This means that it's possible to ask the question, assuming a causal relationship, how much does it cost the Fed to create a job? An important note here is that we're treating an averted layoff (i.e. a reduction of jobless claims by one) as the equivalent of a new job.

The equation reads y = -0.1397x + 751,424. This means that for every $1 million dollars (x-axis is denominated in millions), the Fed can apparently reduce weekly jobless claims by 0.1397 people. The inverse of this ($1mn / 0.1397) is $7.16mn. In other words, it costs the Fed $7.16 million dollars to reduce jobless claims by one person a week. Now, let's factor in that there are 52 weeks in a year, and that suggests that it costs the Fed $137,692 to avert one annual layoff (create one new job). That sounds like a lot of money considering that median per capita annual income for employed people was $41,663 in 2011. It costs the Fed 3.3x the average private sector annual income to prevent one private sector job loss.

It's widely held that the Federal government is inefficient, but just how inefficient is it? The Federal government spent an average of $64,781 per person in payroll on civilian employees in 2010, according to the US Census Bureau. In other words, it costs the Federal Government about 1.5x as much to employ someone as the private sector, and it costs the Fed about 2.1x as much to avert a private sector layoff as it does for the Federal government to hire someone.

QE3 expectations are running high, and the below chart should provide a framework for thinking about its potential impact on jobless claims, when and if the size of the program is unveiled. For reference, a $500 billion program could be expected to reduce weekly initial claims by 69,832. That would take claims down to around 300k from their current 370k. This would be good news for lenders on the credit front; though, curiously, we showed last week that in the last two years the correlation between the price level of the XLF and jobless claims has been effectively zero.

In the second chart below, we show the relationship between the S&P 500 and jobless claims - another tight fit. We showed last week that weekly initial claims and the S&P 500 have an R-squared of 0.8866 from 2007 through present. The equation there is y = -0.0021x + 2128.2. Assuming an initial claims level of 300k, the equation of the line would suggest an S&P 500 level of 1,498.2. Obviously, many things could cause these relationships to breakdown or decouple.

The Details on This Week's Print

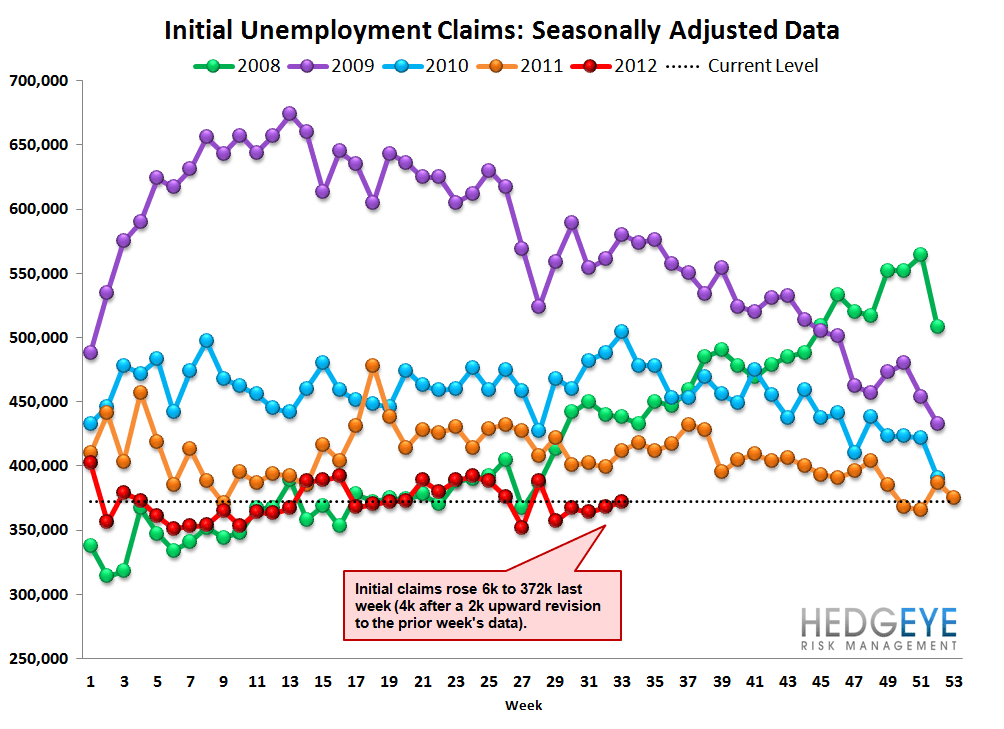

Initial claims rose 6k to 372k last week from 366k, but only 4k after incorporating the 2k upward revision to the prior week's data. Meanwhile, rolling claims rose by 3.75k to 368k.

A bright spot in this past week's print is that for the second week in a row rolling NSA claims widened their YoY improvement, this week moving to -8.3%, vs -7.8% the week prior. This is a healthy sign.

Joshua Steiner, CFA

Robert Belsky