TODAY’S S&P 500 SET-UP – August 22, 2012

As we look at today’s set up for the S&P 500, the range is 10 points or -0.30% downside to 1409 and 0.41% upside to 1419.

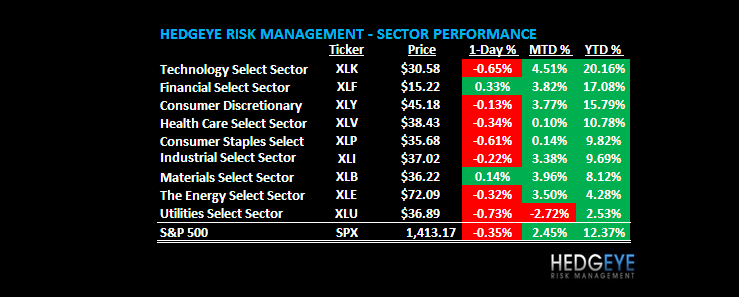

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: on 08/21 NYSE -344

- Decrease versus the prior day’s trading of -343

- VOLUME: on 08/21 NYSE 640.96

- Increase versus prior day’s trading of 16.39%

- VIX: as of 08/21 was at 15.02

- Increase versus most recent day’s trading of 7.13%

- Year-to-date decrease of -35.81%

- SPX PUT/CALL RATIO: as of 08/21 closed at 1.10

- Down from the day prior at 2.44

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: as of this morning 33

- 3-MONTH T-BILL YIELD: as of this morning 0.10%

- 10-Year: as of this morning 1.78%

- Decrease from prior day’s trading of 1.80%

- YIELD CURVE: as of this morning 1.50

- Down from prior day’s trading of 1.51

MACRO DATA POINTS (Bloomberg Estimates)

- 7am: MBA Mortgage Applications, Aug. 17 (prior -4.5%)

- 10am: Existing Home Sales, July, est. 4.51m (prior 4.37m)

- 10am: Existing Home Sales, July, est. 3.2% M/m (prior -5.4%)

- 10:30am: DoE Inventories

- 2pm: FOMC Meeting Minutes

GOVERNMENT:

- House, Senate not in session

- SEC holds meeting on disclosure rules regarding conflict minerals, payments to governments made by resource extraction issuers, 10am

- Federal Reserve Bank of Chicago President Charles Evans holds press briefing at U.S. embassy in Beijing, 11:30pm

- U.S. Census Bureau holds webinar on foreign trade rules, with ombudsman Omari Wooden, 1pm

- Commerce Dept.’s National Telecommunications and Information Administration meets on consumer data privacy codes of conduct concerning mobile application transparency, 9:30am

- NRC, FEMA hold conference call to discuss emergency preparedness plans at U.S. nuclear power plants, 2pm

WHAT TO WATCH:

- Verizon Wireless said to be planning to sell Nokia with Microsoft’s Windows 8 software this year

- UPS extends offer period for TNT to Nov. 9 from Aug. 31

- Dell says PC business deteriorated more than expected

- RBS said to be probed by U.S. over Iranian sanctions

- Carl Icahn withdraws offer to take CVR Energy private

- Jury in Apple, Samsung patent trial begin deliberations

- ATP wins prelim. approval for bankruptcy financing

- Sales of existing U.S. homes probably climbed 3.2% in July

- Exxon, BHP, other energy, mining firms may need to report what they pay each country they tap resources from under rule SEC has votes to adopt

- BHP delays $68b of project approvals, profit plunges

- Sirius directors sued by investors for failing to defend co. from potential takeover by Liberty Media

- IAC/InterActiveCorp said to have offered more than $300m to buy About.com, topping bid from Answers Corp.

- Allianz trims asset-mgmt unit targets on Europe debt crisis

- Microsoft, Samsung may face greater scrutiny of labor practices as Apple’s biggest supplier improves conditions at its Chinese plants

- Japan swings to trade deficit as Europe drags down exports

- Wet Seal hired financial advisers, adopted poison pill

- SEC should approve Nasdaq’s proposal to pay firms $62m for losses suffered in Facebook’s IPO, Citadel said

- Electronic Arts’s PopCap Games fired ~10% of staff

EARNINGS:

- Express (EXPR) 7am, $0.17

- Chico’s FAS (CHS) 7:15am, $0.30

- American Eagle Outfitters (AEO) 8am, $0.21

- Eaton Vance (EV) 8:40am, $0.47

- International Rectifier (IRF) 4pm, $(0.15)

- Kayak Software (KYAK) 4pm, $0.24

- Hain Celestial (HAIN) 4pm, $0.45

- Synopsys (SNPS) 4:05pm, $0.50

- Prospect Capital (PSEC) 4:05pm, $0.40

- Guess? (GES) 4:05pm, $0.51

- Hewlett-Packard (HPQ) 4:05pm, $0.98

- Semtech (SMTC) 4:30pm, $0.41

- Heico (HEI) 4:40pm, $0.41

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

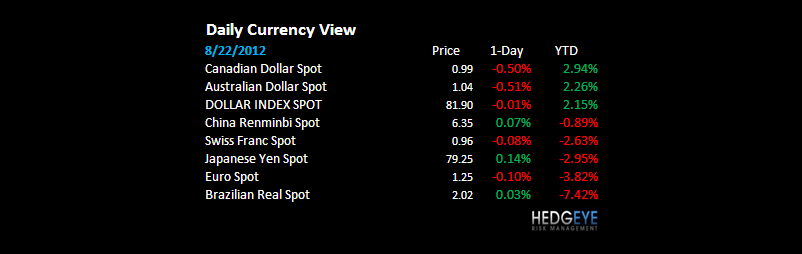

CURRENCIES

EUROPEAN MARKETS

ASIAN MARKETS

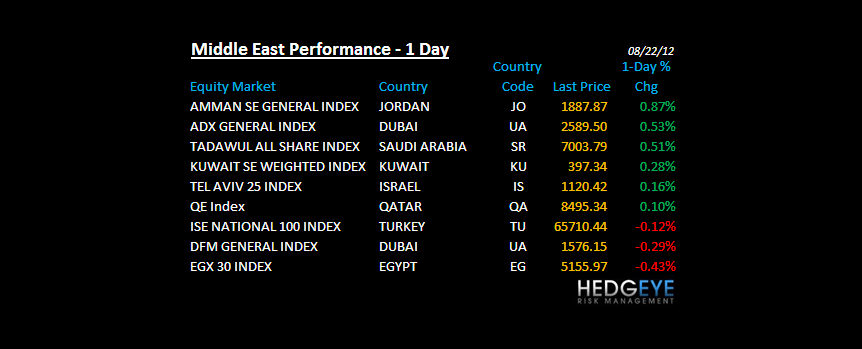

MIDDLE EAST

The Hedgeye Macro Team