Consolidation in the healthcare sector is on everyone’s mind today with Aetna (AET) buying Coventry Healthcare (CVH) for $42.08 a share – a 20.4% premium. Our Healthcare Sector Head Tom Tobin is not surprised as he sees further consolidation in the industry as a dominant trend going forward. This morning, Tobin noted:

• Consolidation and government revenue are the last reliable sources of growth, but ultimately lower quality given the volatile political landscape.

• AET’s presentation promotes increased government sourced revenue from Medicare and Medicaid.

• Forecast accretion is meaningful, as are costs, and extends for several years to 2015.

• Only a few consolidation candidates remain: HNT, HUM, CI

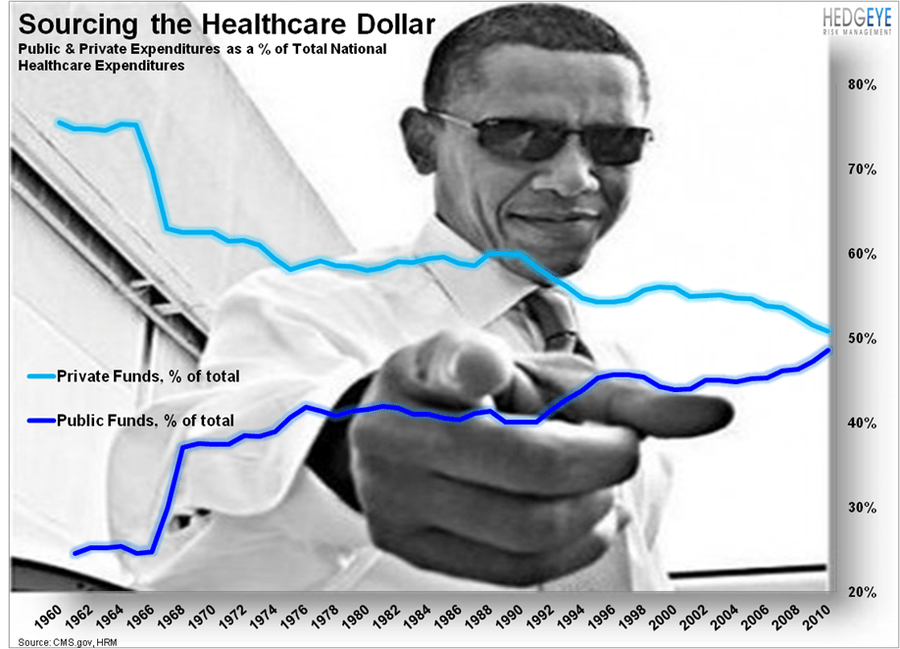

The real takeaway here is that Aetna is looking to make a Medicaid/Medicare play. Big government is big business. The company thinks that the Affordable Care Act (aka Obamacare) is going to stick around. This reform will cover millions more people under the government Medicaid umbrella, which bodes well for Aetna and others who are deriving revenues from Washington.