This note was originally published at 8am on August 03, 2012 for Hedgeye subscribers.

“Markets are increasingly distorted by central banks’ attempts to squeeze drops of growth…”

-Louis Bacon

What do Louis Bacon, Stan Druckenmiller, and George Soros all have in common? They’re some of the best players in this Global Macro game, and they’re all either giving money back to their investors or getting out of the game completely.

They think these central planners are right nuts. So do I. But does the manic media that perpetuates this entire gong show get that? Have these pundits ever traded a macro market in their life? Or, like the worst players at a poker table, are they just the suckers trying to remain relevant until their ratings and/or credibility goes to zero % too?

As the old saying goes, look around the poker table; if you can’t see who the sucker is, you’re probably it.

Back to the Global Macro Grind…

We got longer yesterday (cutting our Cash position to 58%) but it was still a clean cut example of what Louis Bacon coined in a recent letter (explaining why he is giving back $2B to his investors) as Disaster Economics: “where assets are valued based on their ability to withstand a lurking disaster as opposed to what they may yield or earn, is now the prism through which investors are pricing markets.”

Don’t think this is turning into a Q308 like disaster? Ok. What would you call this?

1. 745AM EST (yesterday), Spanish stocks rip to the upside, +2% on the day, after the ECB decides not to cut rates, but plenty of print, tv, and radio pundits proclaim their faith that “it’s at 830AM that we get the good stuff.”

2. 835AM EST (yesterday), Spanish stock stop going up, and fast, as pundits comb the release looking for “hints” that the ECB really is going to deliver the drugs, like Bernanke was supposed to in the day prior.

3. 1130AM EST (yesterday), Spanish stocks close down -5.2% on the day, a 7% (not a typo) intraday reversal. Pundits feel shame.

Or do they? 430AM EST, I get up this morning and “European stocks rally” on new news that Spain (as in the country) is going to hold a press conference about something.

I couldn’t make this up if I tried.

Notwithstanding the simple math of the matter (a market that loses 7% of its value needs to “rally” +7.5% to get whoever got suckered in at 830AM EST yesterday back to break-even), I’d say Bacon is on to something here.

Then you have the other running narrative of people who are in the business of markets going up saying “but the SP500 is up 10% for the year-to-date.” That one is just a beauty – it’s as if people think about their life-long net wealth on the same calendar as Old Wall Street’s bonus season.

Just to get the record straight – and I mean how real people with real money think about the return of their moneys:

- SP500 is not +10% YTD anyway, it’s up +8.5%

- SP500 is down -3.8% from Q1 2012 (when #GrowthSlowing started)

- SP500 is down -12.8% from its 2007 high, where almost everyone of the Q1 2012 bulls were the same people

So, lucky you – you only have to be up +4% and +15% to get back to your 2012 and 2007 break-evens. This better be one heck of a US Employment Report this morning.

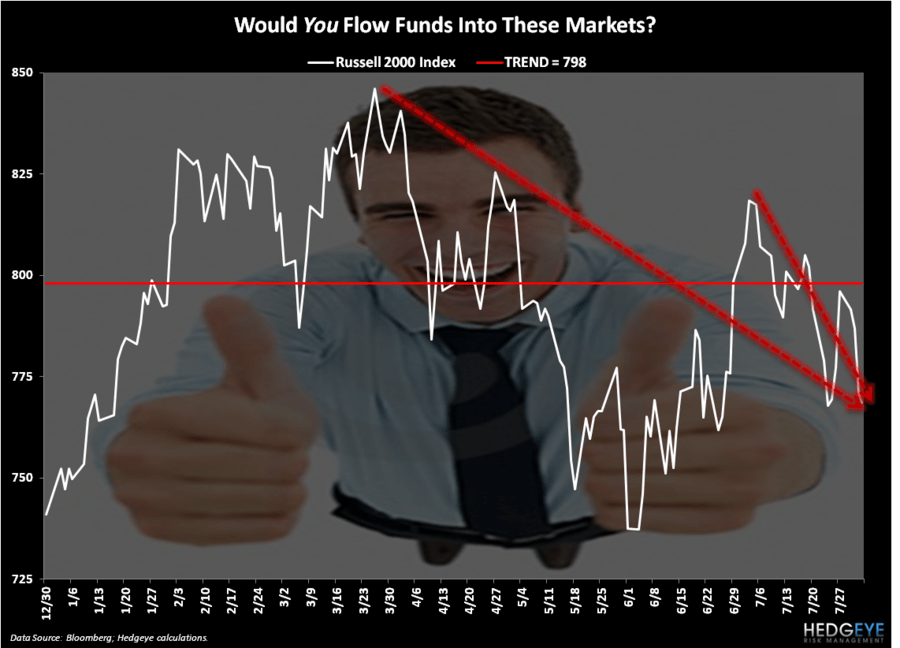

Better yet, if you’ve noticed this other little thing called a broad leading indicator (the Russell 2000 has led the SP500 the entire way):

- RUSSELL2000 is only up +3.6% YTD

- RUSSELL2000 is down -9.1% from its 2012 Perma-Bull high (March 26th, where the VIX bottomed at 14.26)

- RUSSELL2000 is down -6.1% in the last month alone

I know, I know. Don’t be spinning that storyline on us KM, we’re still living large over here on the everything fine front. Until you aren’t. What’s happened this year at MF Global, JP Morgan, and Knight Capital is an obvious reminder of Disaster Economics too.

As returns (both buy and sell-side) get tougher to concoct, we’ve created a culture on Old Wall Street of cheating and corner cutting so that people A) don’t get ridiculed by their peers internally and/or B) get paid.

That pressure is cultural. It’s also called causality. Much like central planning policies to suspend economic gravity, it’s only sustainable until it goes away.

My immediate-term support and resistance ranges for Gold, Oil (Brent), US Dollar, EUR/USD, Spain’s IBEX, and the SP500 are now $1590-1605, $105.09-107.32, $82.95-84.11, $1.20-1.23, 5811-6649, and 1356-1376, respectively.

Best of luck out there today and enjoy your weekend,

KM

Keith R. McCullough

Chief Executive Officer