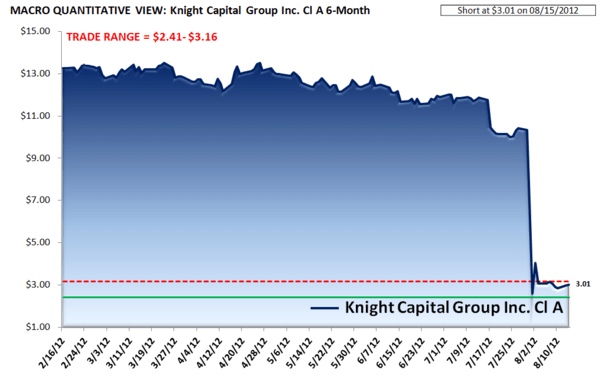

Knight Capital (KCG) has a long ways to go to recover from its near-death experience. We don’t think the event is priced into the stock properly and thus, we see further downside for KCG. Keith shorted KCG in the Hedgeye Virtual Portfolio yesterday at a price of $3.01 a share.

There are three factors affecting Knight that will push the stock down further. One risk of being short is that the company could be acquired at a premium to its current share price. Whether or not it’ll be sold off piecemeal style or just swallowed whole remains to be seen. But for now, consider this:

-Knight took a $35 million loss on Facebook during the IPO. That debacle is still being sorted out with Nasdaq and other parties.

-Trading volumes have been insanely low. Knight’s trading volume has declined sequentially over the last five quarters.

-Knight sold about 70% of the equity to a consortium of buyers in order to save itself. It got $400 million in 2% preferred stock convertible at a $1.50 strike. There is a mandatory conversion provision that says the preferred must be converted if the stock price stays above 2x the strike price for 60 consecutive days.

The stock is entirely capable of going to $1, then $0.50 then $0. CEO Tom Joyce better have an ace up his sleeve because the company is not putting enough effort into saving face. Even more concerning is whether the $400 million will be enough capital to hold the company over heading into the back half of 2012.