We’re at $0.38 for FL headed into Friday’s print before the open on a +9% comp ahead of Street estimates at $0.34E and a comp of +7%.

The stock is up +18% since we published our note “FL: We Like It Here” on June 27th versus the S&P up +6% so it’s fair to say that expectations are high headed into the print, but for good reason.

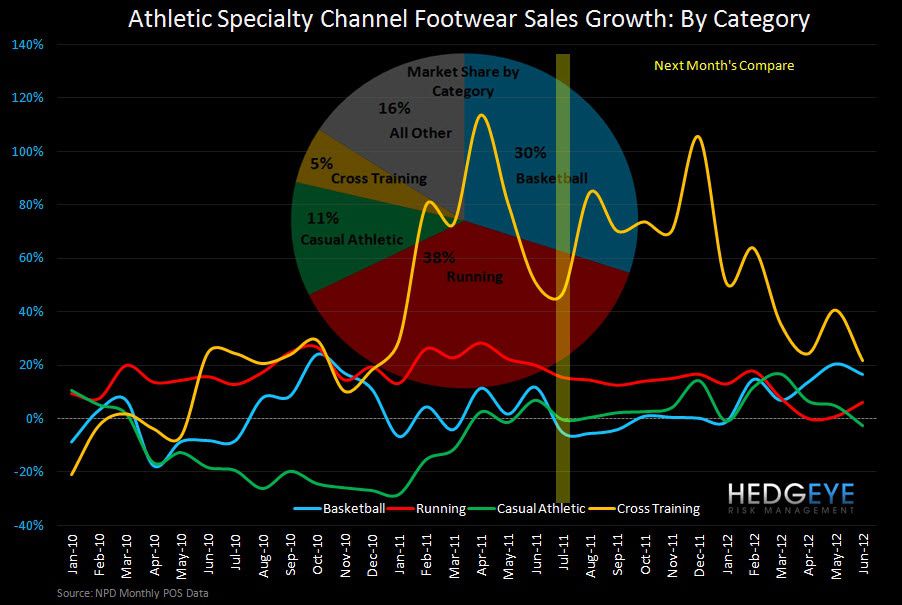

- June footwear sales in the Athletic Specialty Channel came in up +9% following +10% in May. Sales accelerated in July as expected against easing compares headed into the 2H. Given the average 400-600bps markup of weekly trends that reflect sales in aggregate (vs athletic channel), July sales appear to have come in up low-double-digits to low-teens to finish the quarter. In addition, apparel sales also picked up in July. We think this translates to comp of +9% at FL.

- Category mix remains a key driver of outperformance and upside versus peers with strength in basketball – a trend we expect to continue following strike related disruptions last year. Take a look at the chart below, basketball has steadily improved YTD with compares getting easier through the 2H. Running also reaccelerated during the quarter. While a bigger boost for FINL (more heavily indexed to the category), these improving trends headed into the 2H are clearly favorable.

- Europe remains an overhang. FL indicated a strong start to European sales in May with sales turning positive (up +LSD vs. –MSD in Q1), which is a stark contrast to most other retailers with exposure to Europe mitigating further weakness in a region that accounts for ~24% of sales. While we admittedly don’t have great visibility into how June is shaping up, there are two factors to consider re Europe, 1) early indications suggest trends are stable if not turning positive, and 2) compares here are also getting more favorable.

- We’re modeling +80bps of gross margin improvement driven primarily by occupancy leverage up +90bps offset by a modest drag on merchandise margin (-10bps). We are also modeling SG&A up +3.5% reflecting 5% growth in core SG&A including $6.5mm in incremental marketing spend offset by a ~$5mm reduction in Fx.

Bottom-line is that this story in on track. The key drivers continue to be product innovation complemented by an improving apparel assortment mix, growing international store footprint (more productive that domestic base), and expanding digital platform. Given the run into earnings, we think expectation for good numbers is largely reflected in the stock here and as such don't expect a move of the same magnitude we've seen in recent quarters. But numbers are still too low for the year. We’re at $2.49 for the year above the Street at $2.38 and $2.83 for 2013 vs. $2.64E. We continue to like the earnings visibility over the intermediate-term and this name on the long side.

Casey Flavin

Director