TODAY’S S&P 500 SET-UP – August 16, 2012

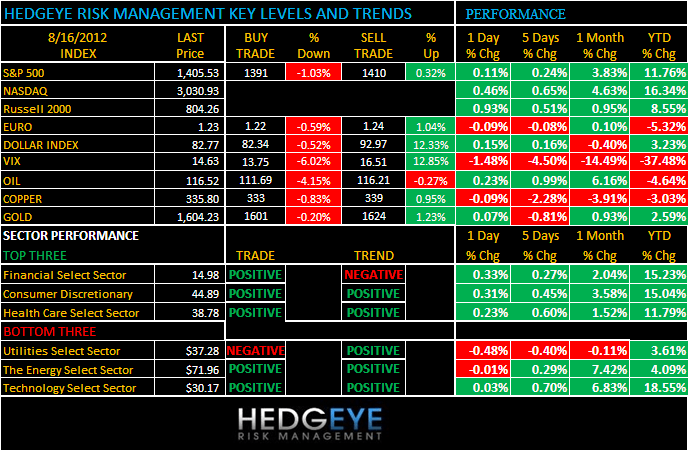

As we look at today’s set up for the S&P 500, the range is 19 points or -1.03% downside to 1391 and 0.32% upside to 1410.

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: on 08/15 NYSE 799

- Increase versus the prior day’s trading of -41

- VOLUME: on 08/15 NYSE 497.83

- Decrease versus prior day’s trading of -12.15%

- VIX: as of 08/15 was at 14.63

- Decrease versus most recent day’s trading of -1.48%

- Year-to-date decrease of -37.48%

- SPX PUT/CALL RATIO: as of 08/15 closed at 1.12

- Down from the day prior at 1.52

CREDIT/ECONOMIC MARKET LOOK:

10YR – talk about ripping; massive short-term rip in bond yields this week looks almost identical to the pace of gains in stocks vs bonds at the March highs; at 14-15 VIX, that was not the buy stocks signal; higher lows in bonds now as stocks make lower highs.

- TED SPREAD: as of this morning 35

- 3-MONTH T-BILL YIELD: as of this morning 0.08%

- 10-Year: as of this morning 1.81%

- Decrease from prior day’s trading of 1.82%

- YIELD CURVE: as of this morning 1.52

- Down from prior day’s trading of 1.53

MACRO DATA POINTS (Bloomberg Estimates)

- 8:30am: Jobless Claims, Aug. 11, est. 365k (prior 361k)

- 8:30am: Housing Starts, July, est. 756k (prior 760k)

- 8:30am: Building Permits, July, est. 769k (prior 760k)

- 9:45am: Bloomberg Consumer Comfort, Aug. 12 (prior -41.9)

- 10am: Philadelphia Fed., Aug., est. -5 (prior -12.9)

- 10am: Freddie Mac mortgage

- 10:30am: EIA Natural Gas

- 8pm: Fed’s Kocherlakota speaks on the Fed in Williston, N.D.

GOVERNMENT:

- House, Senate not in session

- Paul Ryan attends campaign event in North Canton, Ohio. 9:55am

WHAT TO WATCH:

- Lock-up on insider sales of Facebook expires

- U.S. home construction probably held near 4-yr high

- Verizon-cable agreement is said to win antitrust approval today

- Apollo is said to seek up to $12b for flagship LBO fund

- Spain said to speed EU bank bailout after collateral limits

- U.K. retail sales unexpectedly rise as discounts boost fuel

- Apple said to talk with cable industry about set-top TV devices

- Dish is said to plan nationwide satellite broadband service

- JPMorgan, Barclays said among banks to get N.Y. Libor subpoenas

- Morgan Stanley unit fined over junior trader’s $1.3b bet

- AMR’s American denied court approval to cancel pilot contract

- Foreign direct investment in China fell to lowest level in 2 yrs in July

- PepsiCo Gatorade Chief O’Hagan said to leave after sales revamp

- Spotify, Pandora spur U.S. digital music sales past CD purchases

- Pfizer’s experimental arthritis drug works in Ulcerative Colitis

- Cisco 4Q adj. EPS, rev. top ests.; Applied Materials’ 4Q sales may miss est.

EARNINGS:

- Soufun (SFUN) 5:45am, $0.41

- Sears Holdings (SHLD) 6am, $(0.86)

- Children’s Place (PLCE) 6:30am, $(0.66)

- Buckle (BKE) 7am, $0.49

- Cato (CATO) 7am, $0.57

- Wal-Mart Stores (WMT) 7am, $1.17

- Dollar Tree (DLTR) 7:30am, $0.47

- Perrigo (PRGO) 8am, $1.27

- GameStop (GME) 8:30am, $0.16

- Ross Stores (ROST) 8:30am, $0.81

- Gap (GPS) 4pm, $0.48

- Aeropostale (ARO) 4:01pm, $0.01

- Marvell Technology (MRVL) 4:02pm, $0.27

- Brocade Communications Systems (BRCD) 4:05pm, $0.12

- Avago (AVGO) 4:05pm, $0.66

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

OIL – ripping humanity a new one here w/ Brent Oil charging to $116/barrel; Oil is up +32% since June, but that’s not inflationary – take the government’s word for it while it continues to slow real (inflation adjusted) GDP growth.

CURRENCIES

EUROPEAN MARKETS

ASIAN MARKETS

CHINA – If you thought this week’s India Export reports (-15% y/y) was bad, take a peek at the Foreign Direct Investment (FDI) print out of China at -9% y/y #awful; Chinese stocks down for 3rd day out of 4 on that this wk; media begs for stimuli.

MIDDLE EAST

The Hedgeye Macro Team