TODAY’S S&P 500 SET-UP – August 15, 2012

As we look at today’s set up for the S&P 500, the range is 10 points or -0.56% downside to 1396 and 0.15% upside to 1406.

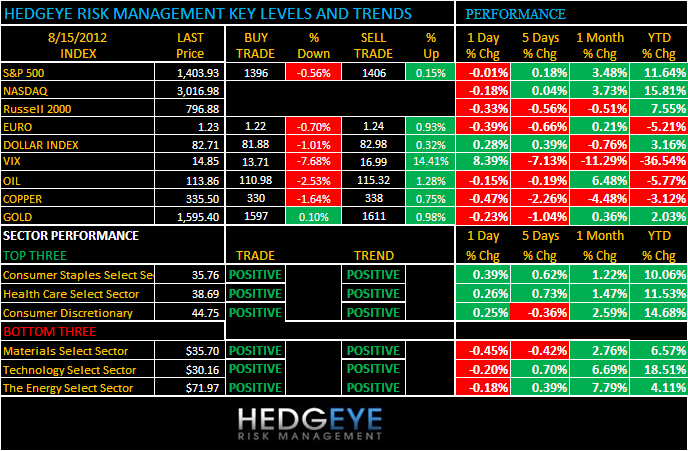

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: on 08/14 NYSE -41

- Increase versus the prior day’s trading of -799

- VOLUME: on 08/14 NYSE 566.69

- Increase versus prior day’s trading of 17.07%

- VIX: as of 08/14 was at 14.85

- Increase versus most recent day’s trading of 8.39%

- Year-to-date decrease of -36.54%

- SPX PUT/CALL RATIO: as of 08/14 closed at 1.87

- Up from the day prior at 1.54

CREDIT/ECONOMIC MARKET LOOK:

QE – Gold doesn’t like this Romney/Ryan ticket calling the “Feds Qe as inflation risk”; USD stabilizing at TREND line 81.68 support as Gold fails again at 1624 TREND resistance; 10yr bond yields put on one heck of a move too; imagine life without Bernanke leaning on the curve…

- TED SPREAD: as of this morning 33

- 3-MONTH T-BILL YIELD: as of this morning 0.11%

- 10-Year: as of this morning 1.76%

- Increased from prior day’s trading of 1.74%

- YIELD CURVE: as of this morning 1.48

- Up from prior day’s trading of 1.46

MACRO DATA POINTS (Bloomberg Estimates)

- 7am: MBA Mortgage Applications, Aug. 10 (prior -1.8%)

- 8:30am: Consumer Price Index M/m, July, est. 0.2% (prior 0.0%)

- 8:30am: Empire Manufacturing, Aug., est. 7 (prior 7.39)

- 9am: Total Net TIC Flows, June (prior $101.7b)

- 9:15am: Industrial Production, July, est. 0.5% (prior 0.4%)

- 9:15am: Capacity Utilization, July, est. 79.2% (prior 78.9%)

- 9:15am: Manufacturing (SIC) Production, July, est. 0.5%, (prior 0.7%)

- 10am: NAHB Housing Market Index, Aug., est. 35 (prior 35)

- 10:30am: DOE inventories

- 11am: Fed to sell $7b-$8b notes due 9/15/14-4/30/15

- 8pm: Fed’s Kocherlakota speaks on the Fed in Minot, North Dakota

GOVERNMENT:

- House, Senate not in session

- First Lady Michelle Obama joins President Obama for campaign events in Dubuque, Davenport, Iowa

- Paul Ryan attends campaign event in Oxford, Ohio. 6pm

- HHS Secretary Kathleen Sebelius makes Affordable Care Act announcement in Jacksonville, Fla. 11:30am

- NLRB holds closed meeting on unfair labor practices. 2:30pm

- Thompson edges out Hovde in Wisconsin Republican Senate primary

WHAT TO WATCH:

- U.S. consumer prices probably rose for 1st time since March, forecast 0.2% gain in CPI

- Retailers to start payments network to take on Google: WSJ

- Standard Chartered rises, pays $340m to settle a N.Y. money laundering probe

- Australia to become 1st nation to require cigarettes to be sold in uniform packages; watch Philip Morris International

- Soros, Cohen’s SAC, Moore among Facebook holders at June end

- Berkshire adds National Oilwell, cuts P&G stake

- Ackman’s Pershing sells Kraft to buy stake in P&G

- Moore leads funds avoiding “dead money” in JPMorgan sales

- Carlyle Group said to be leading bidder to buy Getty Images

- Facebook testing service to include more ads in user news feeds

- Forest Labs holders vote on Icahn nominees at annual meeting

- Credit-card delinquencies, charge-offs to be released

- BMW’s U.S. sales queried after July 31 “discount day": WSJ

- Samsung witness says Apple knew of his ‘‘tablet’’ long before iPad

- MSCI index quarterly rebalancing

EARNINGS

- Staples (SPLS) 6am, $0.22

- Abercrombie & Fitch (ANF) 7am, $0.17

- Deere (DE) 7am, $2.32

- Target (TGT) 7:30am, $1.01

- NetApp (NTAP) 4pm, $0.38

- PetSmart (PETM) 4:02pm, $0.66

- Agilent Technologies (A) 4:05pm, $0.83

- Applied Materials (AMAT) 4:05pm, $0.22

- CACI International (CACI) 4:05pm, $1.50

- Cisco Systems (CSCO) 4:05pm, $0.46

- Ltd Brands (LTD) 4:30pm, $0.48

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

COPPER – the Doctor has been prescribing the same economic message throughout this 6 wk no volume squeeze in everything equities; no support to $3.30/lb; if/when that snaps, copper could go a lot lower on fundamentals (Chinese, German, US demand).

- Paulson Steps Up Gold Bet to 44% of Hedge Fund’s Equity Assets

- Rusal Beating Metal as Near-Record Reserves Elusive: Commodities

- Oil Declines in New York Amid Signs of Increasing U.S. Supplies

- China’s Corn Harvest Set for Smaller Increase on Pest Attack

- Soybeans Rise on Signs Demand Remains Robust After Record Rally

- Gold Seen Declining in London on Reduced Fed Stimulus Outlook

- Copper Seen Falling as China May Struggle to Sustain Growth Pace

- Wilmar Falls After Posting 70% Profit Drop: Singapore Mover

- Cocoa Climbs on Speculation El Nino Is Developing; Sugar Rises

- Palm Oil Drops as Output Gains Set to Boost Malaysian Reserves

- Hermes Sees Crops Extending Gains From Record on Lower Supply

- Cotton Set to Climb 9% as China May Absorb Global Surplus

- Aluminum Premiums Set to Extend Gains as Buyers Wait for Metal

- Natural Gas Futures Decline After Rebounding From Six-Week Low

- China Said to Ask Cooking-Oil Suppliers to Report Prices

- Paulson, Soros Add to Gold Hoard as Prices Drop Most Since 2008

- China Nickel Pig Iron Makers Cut Output by Half as Prices Slump

CURRENCIES

EUROPEAN MARKETS

ASIAN MARKETS

CHINA – headline media “news” last wk was don’t worry about the economic data (#GrowthSlowing) because China is going to cut rates and provide stimuli – reality: PBOC says no on both ($114 Brent Oil crushes consumption), and Chinese stocks are down -2% this wk.

MIDDLE EAST

The Hedgeye Macro Team