Conclusion: We’ve been KORS agnostic since we issued our Black Book on March 12th. But today we don’t think we can call KORS expensive – even after the pop. Every line of the P&L is on fire, and share gain from COH is unmistakable. We don’t love the inventories, and think that people will need to appropriately model occupancy for when comps slow, but for now it does not matter. This name is unshortable at this price.

Straight 'A's for KORS this quarter. Every line of the P&L flies in the face of every global macro headwind the rest of the world is seeing. We don’t love the inventories, and think that people will need to appropriately model occupancy for when comps slow, but for now it does not matter. The only super bearish factor relates to COH, not KORS. The share shift is unmistakable.

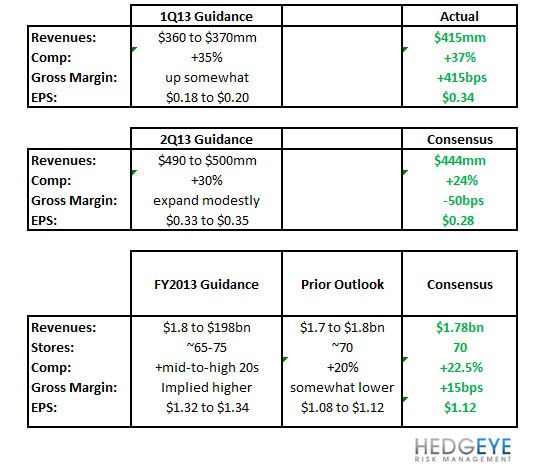

Check out the math:

The clear takeaway from KOR’s Q1 results is simply the share it’s taking from COH. The contrast between the KORS results and what we saw out of COH is startling. Given the magnitude of the beat, margin trajectory, and more constructive outlook for F13, the intermediate-term tailwind behind this story remains firmly intact. As such, this story will remain expensive as great brands with robust earnings momentum and conservative expectations often do. We’d still rather buy FNP than KORS.

What We Liked:

- Every line on the P&L came in better than expected with the top-line accelerating on both a 1 and 2-year basis by over 1000bps (to 71% yy). KORS levered that to +149% EBIT and +156% EPS growth.

- Growth was driven by solid performance across all channels driven by Retail with +31pts from comp stores and +7pts from new stores along with Wholesale contributing +30pts and another +3pts from Licensing. With 23 stores opened in the quarter, KORS is tracking ahead of its plan for ~70 stores in F13. In fact, management suggested that it could be tracking closer to 75 stores for the year. In addition, store productivity continues to improve and is now approaching a run-rate of $1,600/sq. ft. With the retail channel accounting for nearly 2/3 of F13 growth in our model the incremental rate of door growth and productivity continues to be positive.

- Unlike its major competitor, KORS is experiencing solid growth at wholesale with comps up double-digits driven by category expansion (small leather goods, footwear, etc.) in addition to shop-in-shop conversions, which are running ahead of plan and the company’s target of 100 for the year. At this rate we think they are likely running ahead of our expectation of 150 conversions, which would account for at least 5pts of total revenue growth in F13 alone.

- Gross margins: While the mix shift towards retail remains a key gross margin driver over a multiyear period, less discounting/markdown activity also contributed to the +415bps increase. This is in stark contrast to COH which was impacted by an increasingly promotional environment and re-instated couponing just a quarter after eliminating the practice.

- European strength: It's been a while since we've heard a U.S. company note that its European business is ahead of expectations. Well, that’s exactly what KORS did. Yes, Europe still accounts for just under 10% of business so the bar is low, but KORS stores are comping up +23%. We don’t care how small of a footprint they have, demand is there for more – which is exactly what they got.

What We Didn’t Like:

- Inventory growth was the biggest item we flagged last quarter and that continues to be the case. The sales/inventory spread eroded 30pts to -31% with inventories up +102% outpacing sales growth of +71%. Given the rate of store growth, we’re willing to give the company a pass to a point, but it will be important to see this spread shift direction over the next quarter or two.

- For those of you who are modeling out beyond a couple of quarters, keep in mind KORS’ occupancy costs. We think that the comp needed to leverage occupancy is 2x that of other high-end retailers. In other words, KORS could print an 8% comp and still barely leverage occupancy. This is often the case with retailers that are in a hyper-comp stage, as this is partly because of a mix shift towards very expensive real estate, which carries much higher sales per square foot. With comps up so strong, an increase in the hurdle rate of a few points is un-noticeable. But if and when comps revert back to something below 10%, remember that leverage works both ways.

All in, the intermediate-term tailwind behind KORS remainsfirmly intact. We’re shaking out at $1.50 and $1.95 in FY13 and FY14, respectively. That’s about 96% EPS growth this year, and 31% next year. We can complain til we’re blue in the face that KORS is too expensive, but for a high end brand with this kind of share gain and growth trajectory, we could argue that 25x next year’s earnings are cheap. We wouldn’t buy it here on the pop, but we think that it is absolutely unshortable right now.

Share Shift - Youtube:

(KORS Q1cc) “Retail segment, we have experienced strong double-digit comp increases and we believe that we can

continue at double-digit sales pace in our North American Wholesale channel”

(COH Q4cc) “Sales were driven by international wholesale shipments, while shipments into U.S. department stores declined…While in U.S. department stores, sales decreased moderately on a y-over-y basis in the quarter”

Casey Flavin

Director

Accountability and Outlook: Here’s a look at KORS’s variance between guidance and actual, as well as outlook

for F13 vs expectations: