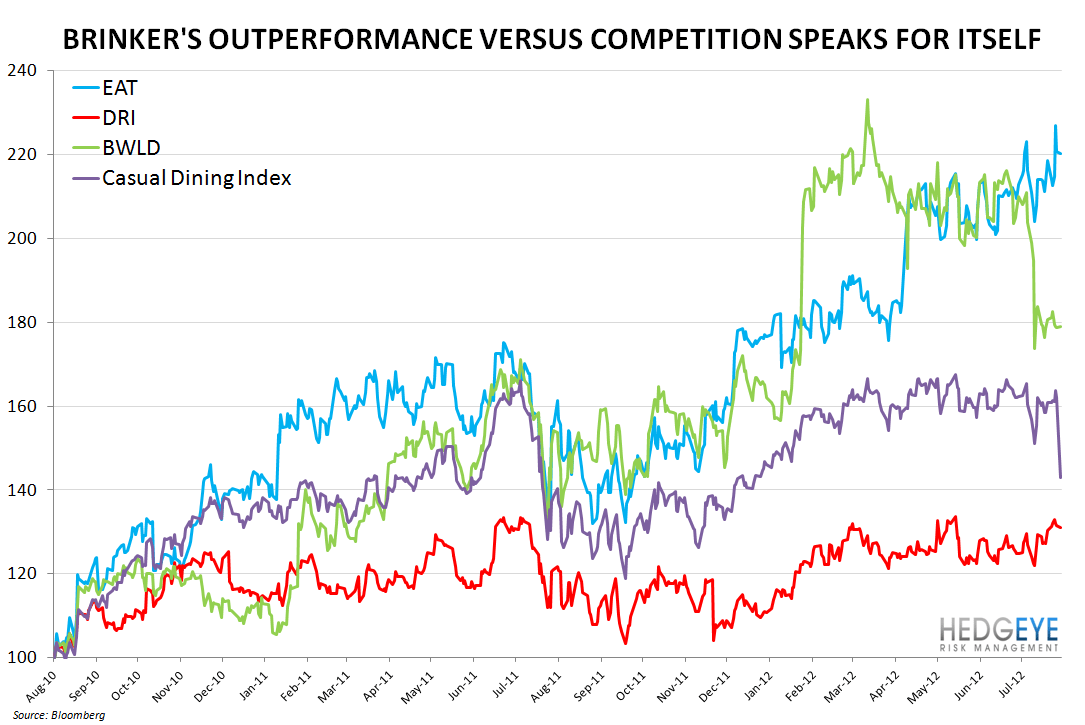

Within the casual dining category, we have been heavily focused on three names this year: EAT, BWLD, and – more recently – DRI. We are positive on Brinker and bearish on Buffalo Wild Wings and Darden. Our view on these stocks is based on the companies’ respective earnings potential versus expectations as dictated by current trends and sentiment in the investment community.

Below, we offer a quick recap of our thoughts on each name:

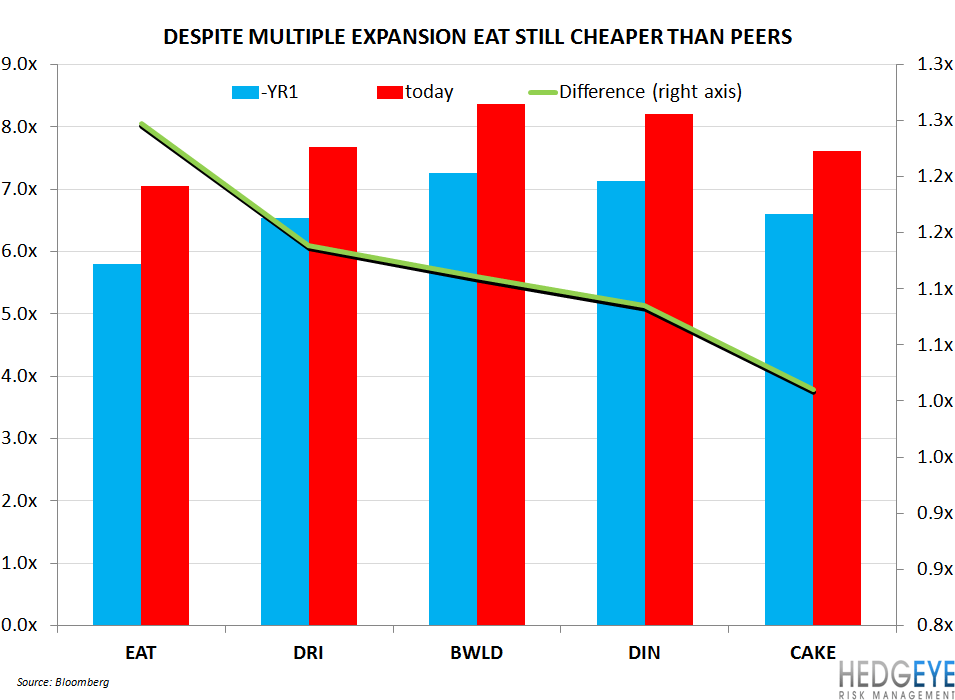

EAT (LONG): Brinker’s strategy over the last couple of years has been focused on “better not bigger” and this mantra has led to Chili’s transitioning from an industry-laggard to an industry-leader (versus industry benchmark Knapp Track Casual Dining Index. This has led to strong earnings growth and, we believe that FY13 has the potential to be another 20+% EPS growth year for the company as Chili’s leverages its superior kitchen technology to roll out additional platforms with far greater efficiency than the competition. Despite having outperformed from a price perspective, the street is still valuing EAT below its casual dining peers on an EV/EBITDA basis.

BWLD (SHORT): Buffalo Wild Wings is a company that we have been bearish on since early 2012. We were concerned by the possibility of a short-term pop in the stock price on 2Q EPS as Wingstop, whose comp-store sales had correlated tightly with BWLD’s (0.96), had posted strong numbers for the quarter. All in all, our FY12 EPS estimate for $3.07 is well below the Street at $3.19 (low estimate is $3.13). The bullish case in April, on the post-earnings sell-off, was that the conversation was set to turn from higher wing prices to lower wing prices. At the time, we said such a stance was premature and that our view of the food processor industry and USDA data was indicative of a persistence of elevated wing costs that would pressure EPS growth in FY12. Given our view that EPS expectations remain overly positive, we are bearish on this stock. While the EV/EBITDA multiple has come in considerably, we believe that consensus EBITDA remains too high.

DRI (SHORT): Darden is the inverse of Brinker in that it is attempting to become bigger first and better second. Rarely, in this industry, do companies become bigger and better at the same time when running multiple chains in one portfolio. Darden’s stock price has diverged dramatically from EPS expectations and, not expecting a reversal in revision trends any time soon (given fundamental trends at Olive Garden and Red Lobster), we would posit that the risk profile of the stock is skewed to the downside. Our continuing concerns about Darden’s long-term outlook are centered on the company’s accelerating capital spending and declining traffic trends at its core concepts. Email Howard for a copy of our recent Black Book on Darden which outlines out thoughts in detail. Unless you think FY13 EPS estimates are heading dramatically higher, you should consider joining the Darden bear-camp.

General Casual Dining Thoughts

When thinking about the casual dining group and the restaurant industry more broadly, we are trying to keep two things in mind for the longer-term: demographics and consumer spending. Given that casual dining is among the most discretionary components of the consumer economy, tracking the population growth of the demographic with the highest propensity to spend (55-65), is instructive for generating an informed view of the group over the longer term. This age cohort's population growth, shown in the chart below, is important for casual dining because of this base of consumers' high frequency use of casual dining chains. The quote below (from Brinker’s CFO no less) provides an insight into how exogenous tailwinds made the industry fat and happy in good times while also conditioning many industry operatives to focus too much on growth.

“It all gets back to this realization or admission of maturity in the space. What got you to win historically in casual dining was demographics in trade area and real estate. That's how you won. We all built many, many restaurants over many, many years and that's how you won. And in many ways we open the doors and they came because there were a lot of macroeconomic tailwinds who were contributing to that. I think when you realize that your space gets more mature, it puts a whole different filter on how you manage your business because you have to do it so much better.

You can't just rely on organic growth to drive improvements in your business. Now you are looking at your existing box and you're saying, how am I going to make this more profitable. And you start to get much, much closer to the consumers. I think that's the biggest realization we came to that the more mature you get, the closer you get to consumers, the more you understand how they use your brand, what really matters to them.”

– Guy Constant, Brinker CFO, 6/4/12

Howard Penney

Managing Director

Rory Green

Analyst