This note was originally published at 8am on July 30, 2012 for Hedgeye subscribers.

“Asset price inflation is not growth.”

-me

I know. You probably need something more profound than a quote from me to kick off your morning. As Bernanke and Draghi unite this week, how about we all take a deep breath and channel our inner Shakespeare? Since in neither the short nor the long run we aren’t all yet dead, we’re best served to always remember that “expectations are the root of all heartache.”

When it comes to performing day-to-day in our centrally planned markets, those expectations obviously go both ways – and fast. On Thursday morning at 5AM EST, US Equity Futures were down 5 handles and Spain’s IBEX was crashing (-33% from its YTD top). This morning, the SP500 is +4% (53 points) higher, and Spain is still crashing (now only down -25%).

Great short-term inflations of asset prices are awesome, right? So is pretending the Fed and ECB can “smooth” and suspend economic gravity. As we continue to make a series of lower long-term highs versus those established when #GrowthSlowing started, globally, again in March 2012, our governments continue to A) shorten economic cycles and B) amplify market volatility.

Back to the Global Macro Grind …

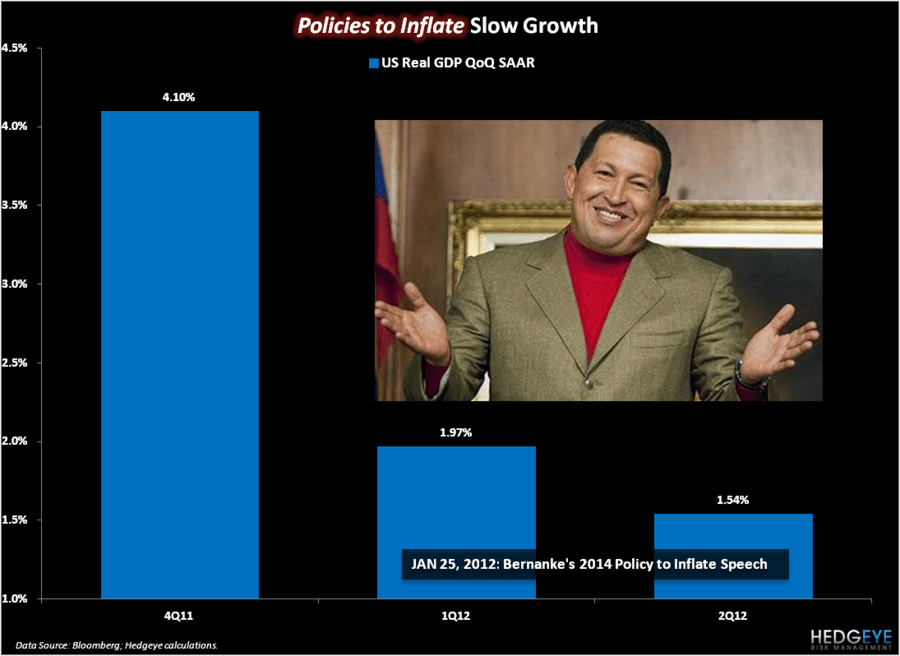

First, let’s go through that ‘inflation slows growth’ thing again with a real life example, US GDP:

- Q4 2011 US GDP Growth = 4.10%

- Q1 2012 US GDP Growth = 1.97%

- Q2 2012 US GDP Growth = 1.54%

So, let’s do more of what has not worked (whatever it takes really), to make sure we keep that asset price speculation (stocks and commodities) in play. Just so that we end up with no real (inflation adjusted) economic growth at all!

Look on the bright side, even though your run of the mill sell-side anchoring “economist” has been off by 33-57% so far with their 2012 US GDP Growth estimates, the stock market went up for the last 48 hours, so they can say they were right on the bull case anyway.

That line of storytelling is as ridiculous as the assumption that begging for Bernanke to give you $1700 Gold and $100 Oil is a “growth” policy for the economy.

That doesn’t mean I can’t be completely wrong here. Evidently this market isn’t short-able, until it is. Meanwhile the Correlation Risk signals are starting to go hog wild (again), doing exactly what they did in February/March.

Got Great Expectations? Here’s last week’s CFTC data on commodity contracts leaning to the long side:

- Oil +6% wk-over-wk to 140,636 contracts

- Sugar +17% wk-over-wk to 128,093 contracts

- Ag (farm goods basket) +4% wk-over-wk to 856,446 contracts

All in, we’ve crossed the proverbial Rubicon again of > 1.0 million CFTC contracts (1.17M this past week), where the entire Street is expecting Great Inflations from Bernanke and Draghi. *Note: these are all time highs in contracts outstanding.

As most of these perma-commodity bulls learned in April/May, what is expected to keep going up, comes down – and hard. Maybe this time is different though? Maybe this is going to be like Venezuela where a centrally planned stock market (up +109% YTD) is governed by explicit currency debauchery?

I am hearing the Venezuelan commoner’s life is mint these days. Also hearing that if Bernanke goes all-in Obama with Qe3, life for the 71% is going to be just rosy too.

Who knows. All we know is that the biggest loser in all of this is what were our “free” markets. Sadly, some still think the stock market is the real-time economy. All the while, these Great inflations continue to deflate both growth and The People’s trust.

My immediate-term support and resistance ranges for Gold, Oil (Brent), US Dollar, EUR/USD, Spain’s IBEX, and the SP500 are now $1590-1624, $105.18-108.26, $82.40-83.26, $1.20-1.23, 6351-6852, and 1360-1392, respectively.

Best of luck out there this week,

KM

Keith R. McCullough

Chief Executive Officer