TODAY’S S&P 500 SET-UP – August 13, 2012

As we look at today’s set up for the S&P 500, the range is 17 points or -1.13% downside to 1390 and 0.08% upside to 1407.

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: on 08/10 NYSE 195

- Down versus the prior day’s trading of 300

- VOLUME: on 08/10 NYSE 566.08

- Decrease versus prior day’s trading of -1.68%

- VIX: as of 08/10 was at 14.74

- Decrease versus most recent day’s trading of -3.53%

- Year-to-date decrease of -37.01%

- SPX PUT/CALL RATIO: as of 08/10 closed at 1.64

- Down from the day prior at 1.82

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: as of this morning 33

- 3-MONTH T-BILL YIELD: as of this morning 0.10%

- 10-Year: as of this morning 1.66%

- Unchanged from prior day’s trading

- YIELD CURVE: as of this morning 1.40

- Unchanged from prior day’s trading

MACRO DATA POINTS (Bloomberg Estimates)

- 11am: Fed to purchase $1.5b-2b notes due 2/15/36-5/14/42

- 11am: U.S. Treasury announces plans for auction of 4-wk bills

- 11:30 am: U.S. to sell $32b 3-mo. bills, $28b 6-mo. bills

- 4pm: USDA weekly crop condition

GOVERNMENT/POLITICS:

- House, Senate in recess

- President Obama begins three-day bus tour through Iowa

- State primary elections in Minn., Conn., Fla., Wis.

- EPA advisory panel meets on methods for estimating emissions from animal feeding operations. 1pm

WHAT TO WATCH:

- Google said to cut ~4k employees in its Motorola unit

- Standard Chartered said to work on New York’s monitor demand

- Julius Baer agreed to pay $880m for Bank of Americas Merrill wealth management business outside U.S.

- Electronic Arts sees new Windows as central mobile game platform

- Peltz said to win board seat at Ingersoll-Rand, WSJ says

- Japan 2Q GDP rose annaulized 1.4%, less than median forecast 2.3% growth and 5.5% in 1Q

- Greece 2Q GDP contracted 6.2%

- “Bourne Legacy” tops weekend NA box office with $40.3m

- Quarterly mutual fund/hedge fund disclosure deadline this week

- Mitt Romney picks Paul Ryan as running mate for Republican ticket

- NBC says weekday daytime Olympic viewership a record, Up 31%

- Guggenheim Partners in talks to buy Aviva stake: Telegraph

- Kodak is scheduled to disclose in bankruptcy court the winners of an auction of >1k patents

- Tech cos. spend more on fewer acquisitions: PwC

- Egypt President Mursi removes military aides

- Europe GDP, Standard Chartered, Wal-Mart: Week Ahead Aug. 13-18

EARNINGS:

- Sysco (SYY) 8am, $0.54

- AuRico Gold (AUQ CN) Pre-Mkt, $0.09

- Groupon (GRPN) 4:01pm, $0.03

- Wuxi PharmaTech (WX) 4:30pm, $0.32

- Uranium One (UUU CN) 4:37pm, $0.02

- InterOil (IOC) 4:45pm, $0.06

- SouthGobi (SGQ CN) 5pm, $(0.04)

- Iamgold (IMG CN) 5:40pm, $0.20

- B2Gold (BTO CN) Post-Mkt, $0.04

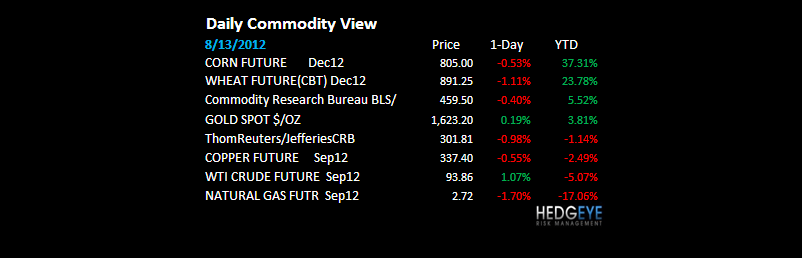

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Hedge Funds Reduce Wagers After Longest-Ever Rally: Commodities

- Oil Bulls Boost Bets Most in More Than 17 Months: Energy Markets

- Copper Declines in New York as Japanese Growth Misses Estimates

- Oil Advances Amid Concern Middle East Tensions May Curb Supply

- Corn, Soybeans Fall as Rain May Aid U.S. Crop Amid Demand Threat

- Iron Ore Drops to Lowest Since 2009 as Chinese Purchases Decline

- Gold Gains on Stimulus Bets as Holdings Climb to All-Time High

- Robusta Coffee Rises as Stockpiles Decline Further; Cocoa Climbs

- China Daily Steel Output Falls in July as Prices at 33-Month Low

- Cooking-Oil Imports by India to Decline on Record Stockpiles

- Rubber Drops to Lowest in Almost Three Years on Slowing Growth

- Noble Profit Rises 39 Percent on Record Metals, Energy Sales

- Japan’s Utilities Lose $46 Billion as End of Era Nears: Energy

- Obama to Urge Agriculture Bill as USDA Buys $170 Million of Meat

- Palm Oil Declines on Increasing Output, Weak El Nino Forecasts

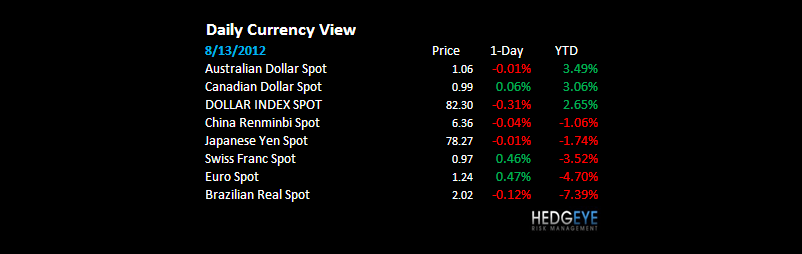

CURRENCIES

USD – on the margin, Paul Ryan is USD bullish – not only will he likely keep Bernanke in a box through September (no Qe), but he’ll bring some much needed focus to the fiscal debate pre debt-ceiling. If intermediate-term TREND support of $81.79 on the USD holds, a whole whack of correlation risk comes back online 2H AUG and into September.

EUROPEAN MARKETS

ASIAN MARKETS

JAPAN – another big country w/ another big miss on the #1 factor that we think will continue to surprise these Keynesian quacks on the downside in the coming months and years – GROWTH; in other Asian Equity news, Chinese stocks fell another 1.5% after not delivering any said stimuli that the media was calling for last wk.

MIDDLE EAST

ISRAEL – something is going on; not sure what it is – but the TelAviv25 just snapped its only line of TRADE support, down 1% this morning and Oil is ripping (+1% to $114 Brent), despite the Dollar not being down a bunch. Geopolitical risk is hard to put our finger on, so we let markets tell us when someone might know something.

The Hedgeye Macro Team