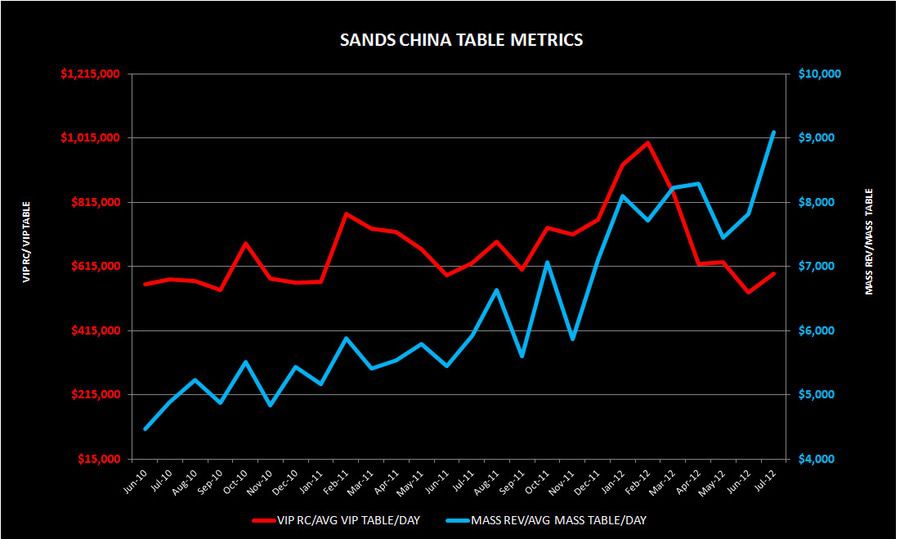

Mass win per table per day popped to an all-time high in July despite the additional SCC tables

- Following a disappointing opening of SCC in April, win per table is moving in the right direction

- Mass continues to set all-time highs for table productivity which bodes well for LVS margins

- Amid the hysteria, VIP productivity is only down to September levels but should start climbing again in September with the opening of the Sheraton rooms