-- For specific questions on anything Europe, please contact me at to set up a call.

No Current Positions in Europe

Asset Class Performance:

- Equities: The STOXX Europe 600 closed up +1.6% week-over-week vs +0.6% last week. Top performers: Portugal +4.5%; Spain +4.3%; Greece +3.4%; Poland +3.2%; Finland +3.1%; Czech Republic +3.0%; Italy +3.0%. Bottom performers: Romania -1.5%; Cyprus -1.2%; Russia (RTSI) -0.4%; Sweden -0.1%. [Other: France +1.8%; Germany +1.1%; UK +1.0%].

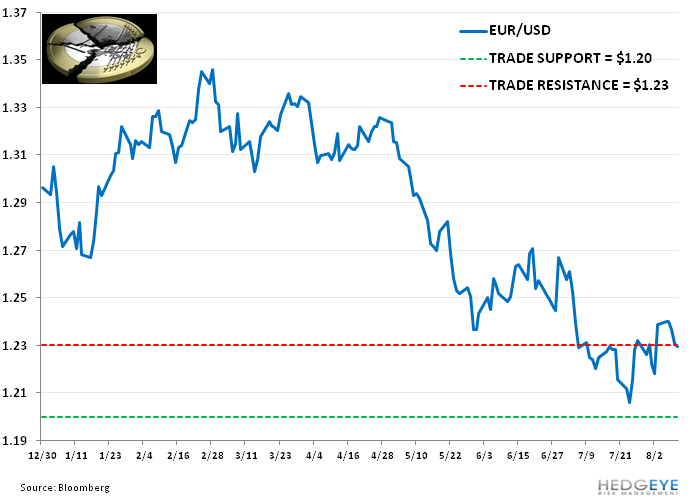

- FX: The EUR/USD is down -0.73% week-over-week vs +1.04% last week [-5.14% YTD]. W/W Divergences: NOK/EUR +1.81%; SEK/EUR +1.40%; RUB/EUR +1.21%; TRY/EUR +0.41%; HUF/EUR +0.09%; CHF/EUR +0.07%; DKK/EUR -0.01%; PLN/EUR -0.23%.

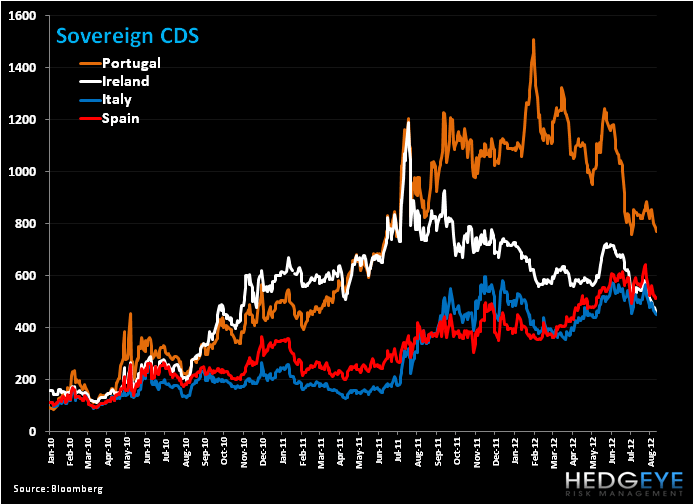

- Sovereign CDS: Sovereign CDS followed yields, down across the periphery this week. On a week-over-week basis Portugal declined the most, down -85bps to 767bps, followed by Spain -49bps to 513bps, Italy -45bps to 450bps, and Ireland -36bps to 462bps.

- Fixed Income: The 10YR yield for sovereigns across the region were mostly down this week. Greece saw the largest decrease week-over-week by -129bps to 24.35%, followed by Portugal at -95bps to 9.99%. Italy and Spain fell -21bps and -12bps to 5.88% and 6.87%, respectively. Germany gained +5bps on the week to close at 1.38%.

Germans On Deck

For a positive week of equity performance from Europe (the STOXX Europe 600 was up +1.6%) there was little material evidence of shifting policy or further clues towards programs to limit the region’s sovereign and banking risks. Interestingly, the market sold off last Thursday as Draghi did not deliver on his “whatever” promise, however seemingly the market was bullish this week on his same comments from the conference call (8/2) in which he said that the ECB “may undertake” non-standard measures, hinting at a reactivation of the SMP to buy bonds on the secondary market and a re-engagement of the EFSF to buy bonds on the primary market. There was still no hint that the SMP has been re-activated. We’ll look to data to be released on Monday for last week’s buying to see if the trend of 21 straight weeks of zero buying from the ECB has been bucked.

We’re also a bit surprised by the market’s move because as it relates to the political risk unfolding (and don’t forget many Eurocrats are on vacation this month), we’d expect more of an impasse as we wait for 12 September and Germany’s Constitutional Court ruling on the constitutionality of the ESM and Fiscal Compact. Interestingly, on Monday the German court was pressed to also rule on the constitutionality of a banking license of the ESM. Arguably this adds another hitch in the German court signing off on the ESM. If it is not passed Eurocrats are back to square one, which leaves the region further in stitch as the EFSF funding ticks down (and is massively undercapitalized to deal with potential sovereign and banking bailout needs/risks on the horizon). On Thursday an important hurdle was cleared in France’s Constitutional Council ruling that the EU Fiscal Compact did not require changes to the constitution.

Please note that as of now, even if the German Court passes, there is no specific language governing the scope of the ESM, namely if it has a banking license, as the only clarity on the program is three vague paragraphs issued at the June 28-9 EU Summit meeting. Said shortly, there’s a lot of political runway left in tying up some of the programs expect to suspend economic reality and provide financial assistance to the periphery.

Given this environment, we’ll work to keep you abreast of the most important calendar catalysts that we think large expectations will be built into.

Calendar Catalysts:

12 September - Germany’s Constitutional Court rules on the constitutionality of the ESM and Fiscal Compact.

12 September - Dutch General Election

Late September - According to La Tribune, Moody's will evaluate the consequences of the Eurozone crisis on France's AAA rating by the end of Q3. We think a downgrade to AA is a real probability.

October - Final discussions expected between Troika and Eurozone finance ministers to determine if Greece is eligible for €31B in new aid, including €25B to recapitalize the banking sector.

Mid October - There’s a possibility of a German Sovereign credit rating downgrade, especially should France be reduced by a notch beforehand.

29 & 31 October - Spain’s debt maturity schedule scares as the Treasury is bumping up against sovereign debt maturities of €20.27 of debt maturing on two days.

Call Outs:

Greece - S&P cuts outlook from Stable to Negative. Sees Greece likely to need additional EU/IMF funding in 2012.

UK - The Bank of England slashed its outlook for British economic growth to 0% for this year, as Eurozone "storm clouds" cast a long shadow and scars from the world's financial crisis appear deeper than previously thought.

- On Stimulus: Governor Mervyn King said there was no urgent need to print more money

- On Rate Cut: King said there’s even less of a case to cut interest rates

- CPI Forecasts: at ~1.7% in 2 years time, ~1.8% in 3 years time

- GDP Forecasts: slashes 2012 growth forecasts to 0% and +1.9% in 2013 (vs May forecast of ~+0.8% and ~+2%, respectively). King warned that the economy would grow at sub-par speed for at least the next three years

EUR/USD:

We remain highly sensitive around our trading ranges of $1.20 to $1.23. We reiterate that below $1.20 we see no material levels of support.

Data Dump:

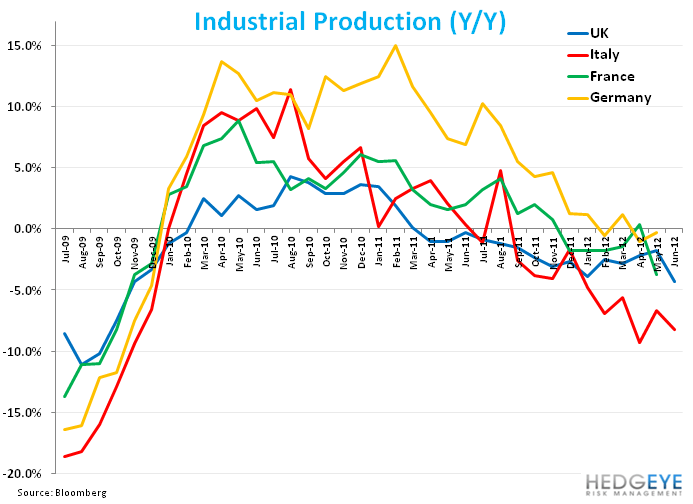

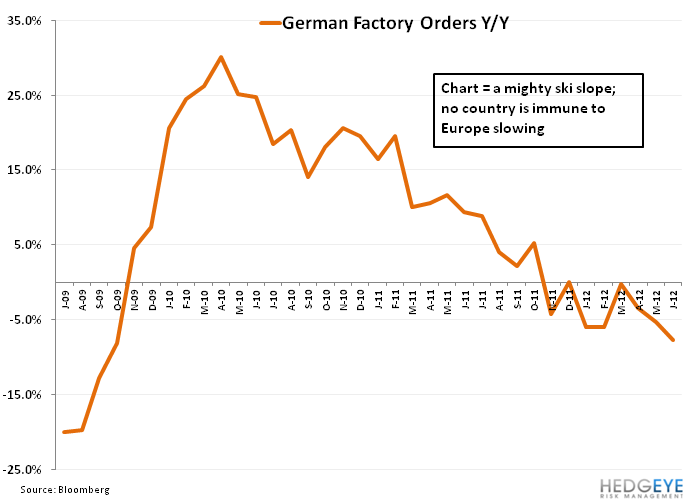

---We saw another week of weak data from Europe. In the charts below we highlight bombed out industrial production figures, and note that even the perceived economic stalwart of Germany has slid substantially as shown in the German Factory Orders chart.

Eurozone Sentix Investor Confidence -30.3 AUG vs -29.6% JUL

Germany Factory Orders -7.8% JUN Y/Y (exp. -7.0%) vs -5.3% MAY [-1.7% JUN M/M (exp. -0.8%) vs 0.7% MAY]

Germany Exports -1.5% JUN M/M (exp. -1.3%) vs 4.2% MAY

Germany Imports -3.0% JUN M/M (exp. -2.0%) vs 6.2% MAY

Germany Industrial Production -0.3% JUN Y/Y vs -0.3% MAY

Germany CPI FINAL 1.9% JUL Y/Y (vs prev estimate of 2.0%)

France Industrial Production -2.3% JUN Y/Y (exp. -1.8%) vs -3.7% MAY

France Manufacturing Production -2.6% JUN Y/Y (exp. -2.1%) vs -4.6% MAY

Bank of France Business Sentiment 90 JUL vs 91 JUN

UK Halifax House Price -0.6% JUL Y/Y (inline) vs -0.5% JUN [-0.6% JUL M/M (exp. -0.5%) vs 0.8%]

UK New Car Registrations 9.3% JUL Y/Y vs 3.5% JUN

UK Industrial Production -4.3% JUN Y/Y (exp. -5.3%) vs -1.8% MAY

UK Manufacturing Production -4.3% JUN Y/Y (exp. -5.7) vs -1.8% MAY

UK PPI Input 1.3% JUL M/M (exp. 1.3%) vs -2.9% JUN [-2.4% JUL Y/Y (exp. -1.5%) vs -3.0% JUN]

UK PPI Output 0.0% JUL M/M (exp. 0.0%) vs -0.6% JUN [1.7% JUL Y/Y (exp. 2.0%) vs 2.0% JUN]

Italy Q2 GDP Preliminary -0.7% Q/Q (exp. -0.8%) vs -0.8% in Q1 [-2.5% Y/Y (exp. -2.5%) vs -1.4% in Q1]

Italy Industrial Production -8.2% JUN Y/Y vs -6.6% MAY

Italy CPI FINAL 3.6% JUL Y/Y (prev. est. 3.7%)

Spain Industrial Output NSA -6.9% JUN Y/Y vs -5.7% MAY

Spain Housing Transactions -11.4% JUN Y/Y vs -11.6% MAY

Portugal Industrial Sales -3.2% JUN Y/Y vs -1.1% MAY

Portugal CPI 2.8% JUL Y/Y vs 2.7% JUN

Portugal Construction Works Index 55.4 JUN vs 59.3 MAY

Switzerland Unemployment Rate 2.9% JUL vs 2.9% JUN

Switzerland CPI -0.8% JUL Y/Y vs -1.2% JUN

Netherlands Industrial Production -2.4% JUN Y/Y vs 0.0% MAY

Netherlands CPI 2.6% JUL Y/Y vs 2.5% JUN

Austria Wholesale Price Index 1.2% JUL Y/Y vs 0.2% JUN

Norway Industrial Production 7.7% JUN Y/Y vs 13% MAY

Norway CPI including oil -0.6% JUL Y/Y vs -0.2% JUN

Finland Industrial Production -1.0% JUN Y/Y vs -1.4% MAY

Denmark CPI 2.1% JUL Y/Y vs 2.2% JUN

Ireland CPI 2.0% JUL Y/Y vs 1.9% JUN

Ireland Consumer Confidence 67.7 JUL vs 62.3 JUN

Ireland Industrial Production 9.2% JUN Y/Y vs 4.6% MAY

Greece CPI 1.3% JUL Y/Y vs 1.3% JUN

Greece Unemployment Rate 23.1% MAY vs 22.5% APR

Czech Republic Unemployment Rate 8.3% JUL vs 8.1% JUN

Czech Republic CPI 3.1% JUL Y/Y vs 3.5% JUN

Hungary Industrial Production 0.6% JUN Y/Y vs 2.4% MAY

Bulgaria Industrial Production 1.5% JUN Y/Y vs 0.4% MAY

Latvia Q2 GDP Preliminary 1.0% Q/Q vs 1.0% in Q1 [5.1% Y/Y vs 6.8% in Q1]

Turkey Industrial Production NSA 2.7% JUN Y/Y vs 5.9% MAY

Interest Rate Decisions:

(8/9) Serbia Repo Rate HIKED 25bps to 10.50%

The Week Ahead:

Monday – Jul. Germany Wholesale Price Index; UK Jul. RICS House Price Balance; Italy Jun. General Government Debt; 2Q Greece GDP - Advance

Tuesday – Aug. Eurozone ZEW Survey Economic Sentiment; Jun. Eurozone Industrial Production; 2Q Eurozone GDP – Advance; Aug. Germany ZEW Survey Current Situation and Economic Sentiment; 2Q Germany GDP – Preliminary; Jul. UK CPI, RPI; Jun. UK ONS House Price; Jul. France Consumer Price Index; 2Q France Gross Domestic Product – Preliminary, Non-Farm Payrolls, Wages; Jul. Spain Consumer Price Index - Final

Wednesday – UK BoE Minutes; Jul. UK Claimant Count Rate, Jobless Claims Change; Jun. UK Average Weekly Earnings, ILO Unemployment Rate,

Employment Change

Thursday – Jul. Eurozone CPI; Jul. UK Retail Sales; Jun. Spain Trade Balance

Friday – Jun. Eurozone Current Account, Trade Balance; Jul. Germany Producer Prices

Matthew Hedrick

Senior Analyst