Keith shorted JCP again today on the short squeeze around what what was a quarter that can be characterized as none other than Horrendous.

We won't bother with the full financial review. Comps down -22%, dot.com down 33% and a ($0.67) loss pretty much sims that up.

But that's the past. We invest for the future. One thing that matters in investing for the future is believing in who is running the ship. We initially figured that Johnson's Apple halo would have lasted 18-24 months. But about 5-minutes into his commentary today, his credibility stood up, ran out the door, and got hit by a bus.

Last quarter, his level of arrogance around communicating the message was bothersome. He spoke to the Street like we were toddlers, or at least retail novices. He glossed over the bad, and played up whatever positive statistic he could find. A JV mistake for a new CEO.

We #timestamped our view in the Twittersphere this morning that the key thing we were looking for today from RJ was humility, and a realistic view as to how he portrayed what challenges lie ahead.

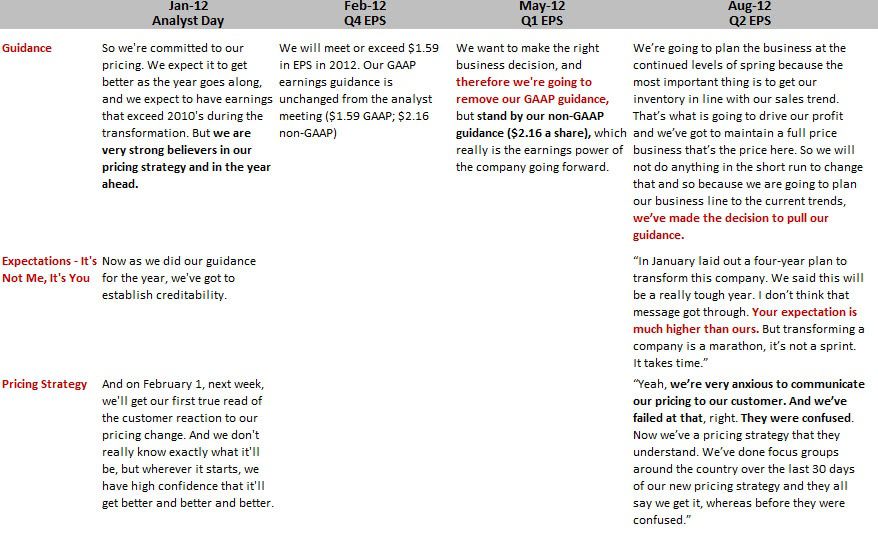

In the first 2 minutes, he started off great by highlighting 2 mistakes he's made. Pricing and marketing. But then he fowled it up by saying -- in a very firm tone -- "In January we laid out a four-year plan to transform the company. We said this will be a really tough year. I don't think that message got through. Your expectation is much higher than ours."

Really Ron? You sent through a pretty definitive message when you said the following...

Feb 24th Q4 earnings call: "We will meet or exceed $1.59 in EPS in 2012. Our GAAP earnings guidance is unchanged from the analyst meeting ($1.59 GAAP; $2.16 non-GAAP)"

May 15th Q1 earnings call: "We want to make the right business decision, and therefore we're going to remove our GAAP guidance, but stand by our non-GAAP guidance ($2.16 a share), which really is the earnings power of the company going forward." But the catch is that they did not let us know what the restructuring charges were. So there was no way we could really tell if they were on track.

Aug 10 Q2 earnings call: "We've made the decision to pull our guidance."

Also, can you explain why you sold your stock just before that last earnings release? You have better information than everybody else, and you bailed. Someone was on the other end of that trade. Ever think of that?

This is an execution story. Execution requires trust. Trust needs to be earned, not gifted. This team has zero. And what's sad is that it was all very avoidable. Simply be up-front and honest with your shareholders, and you generally will be ok. But a bad reputation will take a long time to recover from.