TODAY’S S&P 500 SET-UP – August 10, 2012

As we look at today’s set up for the S&P 500, the range is 17 points or -1.06% downside to 1388 and 0.16% upside to 1405.

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: on 08/09 NYSE 300

- Up versus the prior day’s trading of 62

- VOLUME: on 08/09 NYSE 575.75

- Decrease versus prior day’s trading of -9.56%

- VIX: as of 08/09 was at 15.28

- Decrease versus most recent day’s trading of -0.26%

- Year-to-date decrease of -34.70%

- SPX PUT/CALL RATIO: as of 08/09 closed at 1.82

- Up from the day prior at 1.52

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: as of this morning 34

- 3-MONTH T-BILL YIELD: as of this morning 0.11%

- 10-Year: as of this morning 1.64%

- Decrease from prior day’s trading of 1.69%

- YIELD CURVE: as of this morning 1.38

- Down from prior day’s trading at 1.42

MACRO DATA POINTS (Bloomberg Estimates)

- 8:30am: Import Price Index (M/m), July, est. 0.2% (prior -2.7%)

- 8:30am: USDA crop forecast

- 11am: U.S. Fed to sell $7b-$8b notes in 7/15/2013 to 1/31/2014 range

- 1pm: Baker Hughes rig count

- 2pm: Monthly Budget Statement, July, est. -$93b

GOVERNMENT/POLITICS:

- House, Senate not in session

- CFTC holds closed meeting on enforcement matters, 10am

- NOAA Acting Deputy Director Tracy Dunn, Greenpeace campaigner Phil Kline discuss U.S. ocean, coastal law enforcement at Environmental Law Institute, 12pm

WHAT TO WATCH:

- U.S. won’t prosecute Goldman Sachs, employees over CDO deals

- Yahoo strategy review may result in changes to cash plans

- RIM said to draw interest from IBM on enterprise-svcs unit

- Corn near record as USDA to report on drought damage

- Manchester United raises $233m as IPO prices below range

- RBA highlights currency risk as 2012 growth forecast raised

- Standard Chartered’s fitness is key grounds on shutdown decision in N.Y. law, not laundering

- Knight says it may suffer more losses from trading error

- Knight Investors face funding options with Hotspot, Direct Edge

- WellPoint CEO faces ire of investor who says she must go

- Citigroup offers to buy back bonds in plan to use “excess cash”

- China export growth collapses as World recovery slows

- Hong Kong economy grows at close to slowest pace in 3 years

- Gold bulls strengthen on outlook for more stimulus

EARNINGS:

- Calfrac Well Services (CFW CN) 6am, C$(0.046)

- Enerplus (ERF CN) 6am, C$(0.02)

- J.C. Penney (JCP) 6am

- ioCan REIT (REI-U CN) 7am, C$0.37

- Rentech Nitrogen Partners (RNF) 7am, $0.98

- Brookfield Asset Management (BAM/A CN) 7:06am

- Harman International (HAR) 7:30am, $0.64

- Celtic Exploration (CLT CN) 8am, C$(0.14)

- Emera (EMA CN) 12:30pm, C$0.27

- Pengrowth Energy (PGF CN) Post-Mkt, C$(0.04)

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

COPPER – the Doctor sees this Chinese slowdown for what it is – too big to bail. Copper fails fast at 3.43 TRADE resistance, down -1.2% this morning; CRB Index fails at my TAIL risk line of 307.

- Rig Shortage Means Record $4.5 Billion Blowout Binge: Energy

- Sugar Poised for Two-Year Low After Rains Ease: Chart of the Day

- Cocoa Poised for Rally as Investor Bets Climb: Chart of the Day

- Gold Bulls Strengthen on Outlook for More Stimulus: Commodities

- Corn Advances to Record as USDA Set to Report on Drought Damage

- Oil Pares Weekly Gain on China, IEA Sees Demand Growth Slowing

- Gold Declines With Stocks, Euro as China Data Tempers Risk Mood

- Copper Drops as China Export Collapse Adds to Slowdown Signs

- Sugar Rises as India’s Set to Import From Brazil; Cocoa Advances

- Oil May Rise on Refinery Runs, Middle East Tension, Survey Shows

- Sugar Output in India Set to Fall on Dry Weather, Kingsman Says

- China Soybean Imports Gain for Fifth Month Even as Prices Soar

- China’s Iron Ore Imports Drop to 3-Month Low on Falling Prices

- India’s Green-Energy Providers May Struggle After Power Blackout

- Rises to Record on U.S. Drought Damage

- Oil-Equities Link Nears Record as Stimulus Looms: Energy Markets

- India to Import Sugar From Brazil on Dryness, White Premium

CURRENCIES

EURO – snapping my 1.23 TRADE line again; that puts a boat load of correlation risk back in play, at lower-highs, for a lot of big beta trades (stocks and commodities).

EUROPEAN MARKETS

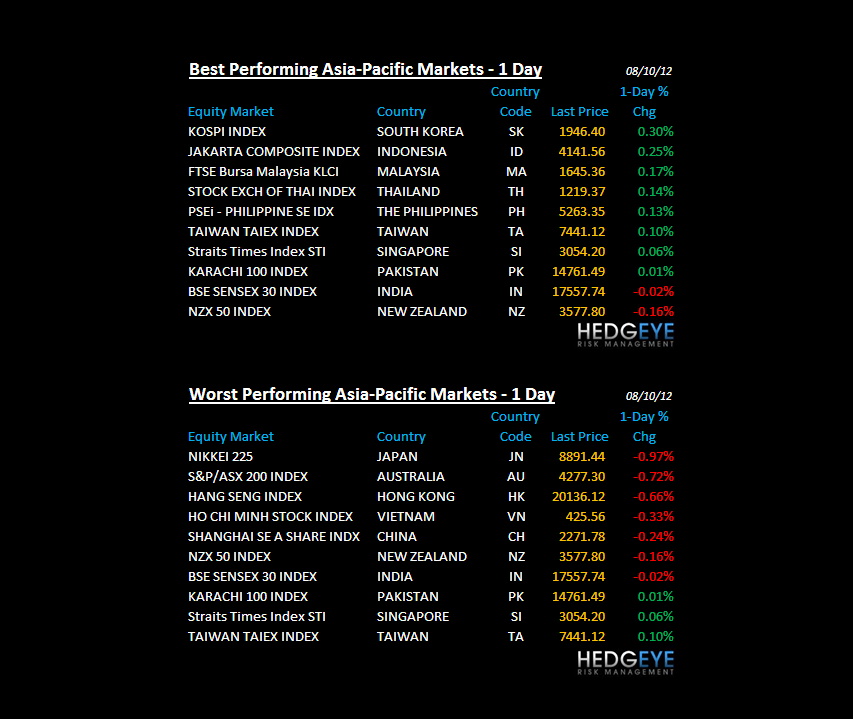

ASIAN MARKETS

CHINA – exports falling like hot knife through butter, but do not worry – bailouts coming, allegedly. No stimuli announced overnight; both Chinese and Japanese stocks fail at big TRADE and TREND lines of resistance, respectively.

MIDDLE EAST

The Hedgeye Macro Team