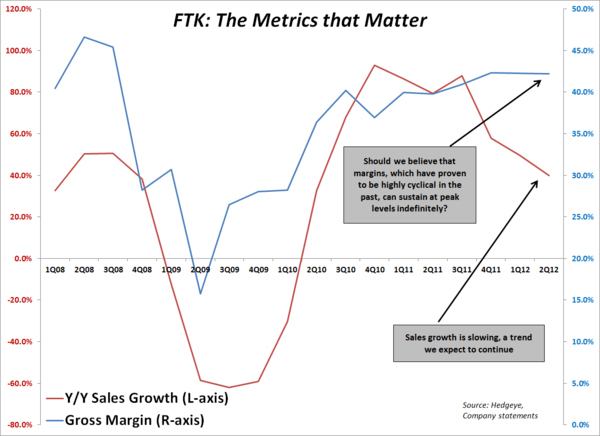

For months we have been bearish on Flotek Industries (FTK). The case we’ve made is that large oilfield services (OFS) players have seen their revenue come under pressure from lower energy prices. When cost cutting measures come into play, chemical suppliers like Flotek will be the first to undergo price renegotiations, which in turn hits their margins.

Flotek reported its second quarter results today. It missed on the top line ($78MM vs. $81MM estimate) but beat on headline EPS ($0.25 vs. $0.22 consensus). That headline number is noisy, skewed mostly by a change in the fair value of warrant liability. Operating income (does not include unusual items) was a big miss, which was largely ignored this morning. Operating income came in at $15.6MM vs. $17.3MM expected.

Yet after reporting second quarter results, Flotek enjoyed a +15% pop in their stock. We were not short FTK in the Hedgeye Virtual Portfolio but after this pop, we will look to short again when price and timing line up accordingly. Hedgeye Energy Analyst Kevin Kaiser outlines his two-fold bearish thesis on FTK below:

1. Top line growth is slowing faster-than-expected as drilling activity slows onshore North America;

2. Gross margins would contract sequentially as pricing power slips and input costs remain sticky in the Company’s Chemical and Drilling business lines.

We were spot on for the first point, but the second point we missed. Apparently the Street is willing to take the company’s word on guidance for gross margins despite our case with regard to pressure on large OFS players like Haliburton (HAL) and Baker Hughes (BHI). We think that margin guidance + the high short interest (18%) is why the stock is so strong this morning.

In essence, this quarter is being spun very well by market participants. On our quantitative model, FTK has broken out above our TREND line of $10.82, so we will wait and watch here.