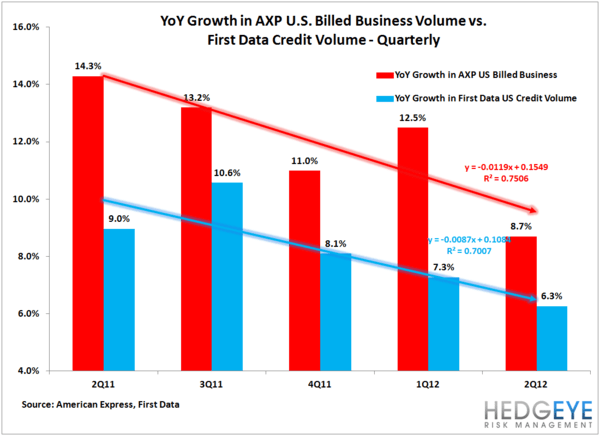

It should come as no surprise that our call on Growth Slowing has come into fruition over the first half of the year. More and more companies are putting up numbers, metrics and comments that reflect the state of today’s economy. The latest company to own up to this theme is American Express (AXP).

American Express hosted its semi-annual Investor Day this week and the commentary from management was not positive to say the least. July billing numbers have slowed sequentially versus Q2 and only provided updates on an FX-adjusted basis, saying that global billed business grew 6% year-over-year in July, 2012 vs. 9% in 2Q12 and 13% in 1Q12. In other words, there’s a -7% of slowing growth in only four months.

While 93% of Street analysts have a buy/hold call on AXP, Hedgeye Financials Sector Head Josh Steiner has taken the contrarian route and remains bearish on the stock. The comment below from AXP CEO Ken Chenault backs up Steiner’s thesis:

“…there is no one specific driver of the recent trend; the Company’s billed business in July appears to reflect a weak overall economic environment, which shows up in a number of areas, including small business and corporate spending.”

The problem is obvious at this point to most people. Consumers are still worried about the economy and until we get some form or indicator that things have stabilized and are improving, they are more hesitant to go out and use their charge card for purchases. Some merchants are hoping that they’ll enjoy strong Back To School numbers for August but as we’ve said before: hope is not a risk management process.

The next quarter and back half of 2012 does not look good for AXP. When the time and price is right, we’ll be shorting it.