Real Employment Improvements Continue to Slow

Non-seasonally adjusted claims, on a 4-week rolling average, were down 6% this week vs. last year. That's consistent with the trend over the past few weeks. Importantly, this is a significant change from where we were 14 weeks ago. Going back roughly 3 months, the rolling NSA claims series was improving at ~12% on a YoY basis. Six hundred basis points of improvement deceleration in 3 months is notable. Extrapolating that trend, the positive economic tailwind from claims will have run its course by the end of October.

As a reminder, YoY changes in rolling NSA claims are our preferred measure of the true underlying health in employment as there are substantial errors in the seasonal adjustment factors making them unreliable.

The headline initial jobless claims print fell 4k to 361k last week. Incorporating the 2k upward revision to the previous week's data, claims fell by 6k. On a rolling basis, initial claims rose by 2.25k to 368k. We're not aware of any distortions to last week's print, making it largely uneventful.

That Said, An Illusory Tailwind Is Coming Soon

As a reminder, August should represent the peak for the seasonal adjustment factor headwind, and should begin turning into a tailwind beginning in September, i.e. on the fourth anniversary of Lehman's bankruptcy. Since the market tends to focus on the SA data's week to week change, the perception of the jobs environment should turn increasingly more favorable in the coming months. This comes with the obvious caveat that this is solely the seasonal adjustment factor we're describing. The real underlying data, as we pointed out above, is showing signs of decelerating improvement.

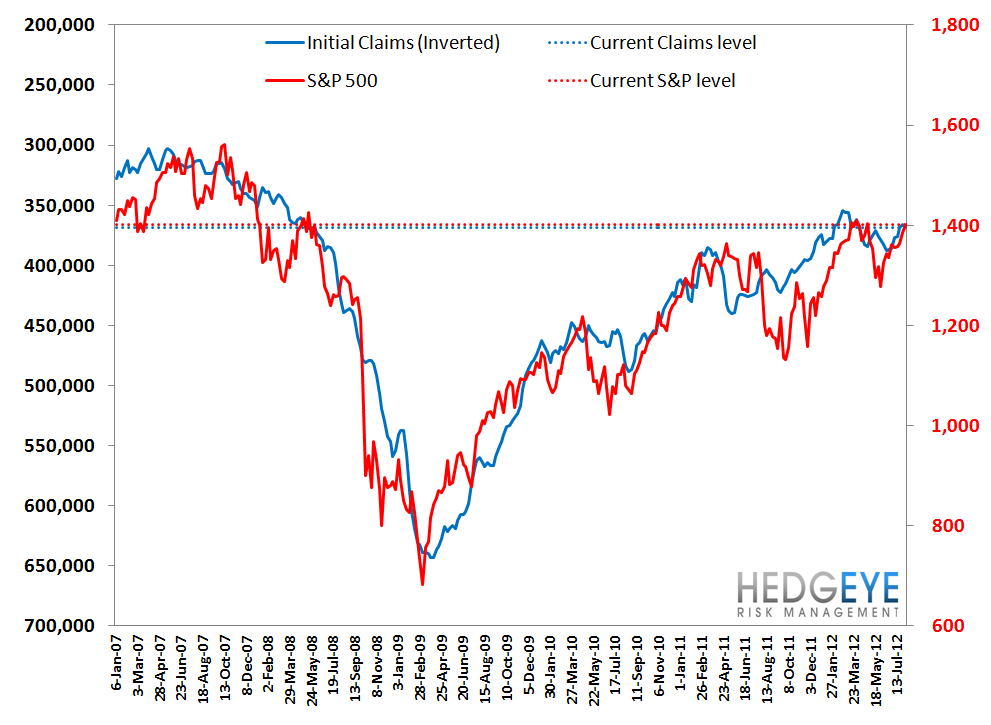

It's also worth noting that with last week's print and the recent market rally, the market is now back in equilibrium with claims, as we show in our fifth chart below.

The 2-10 Spread

The 2-10 spread widened 9 bps WoW to 138 bps. The ten-year treasury yield rose 12 bps to 165 bps.

Financial Subsector Performance

The table below shows the stock performance of each Financial subsector over four durations.

Joshua Steiner, CFA

Robert Belsky

Having trouble viewing the charts in this email? Please click the link at the bottom of the note to view in your browser.