TODAY’S S&P 500 SET-UP – August 9, 2012

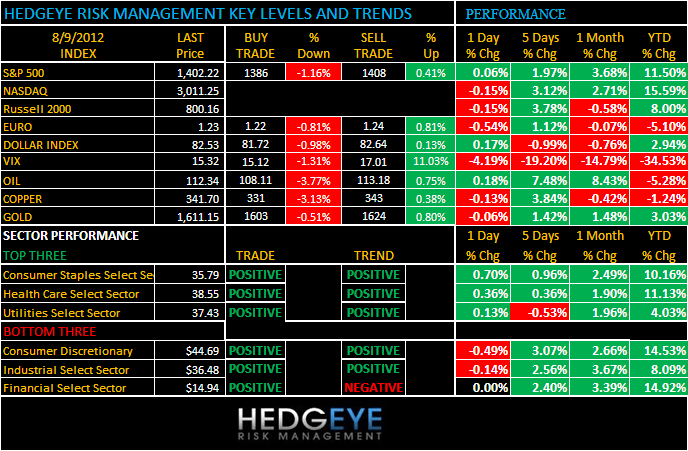

As we look at today’s set up for the S&P 500, the range is 22 points or -1.16% downside to 1386 and 0.41% upside to 1408.

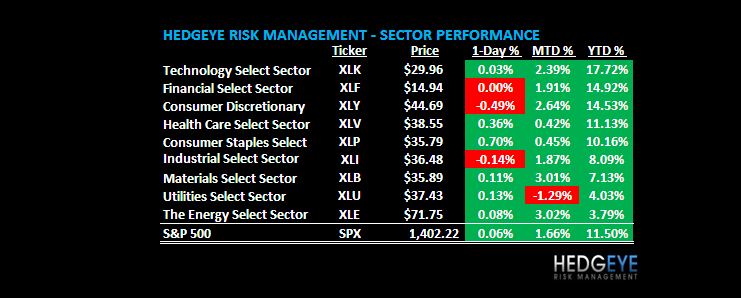

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: on 08/08 NYSE 62

- Down versus the prior day’s trading of 888

- VOLUME: on 08/08 NYSE 636.63

- Decrease versus prior day’s trading of -12.54%

- VIX: as of 08/08 was at 15.32

- Decrease versus most recent day’s trading of -4.19%

- Year-to-date decrease of -34.53%

- SPX PUT/CALL RATIO: as of 08/08 closed at 1.52

- Up from the day prior at 1.33

CREDIT/ECONOMIC MARKET LOOK:

10YR – this has happened plenty of times in 2012 – bonds down hard in 1-2wk moves, presenting you w/ a buying opp in bonds or 1 more chance to tell yourself this time is different and growth is not slowing. There’s a TREND wall of resistance for the 10yr at 1.71%.

- TED SPREAD: as of this morning 33

- 3-MONTH T-BILL YIELD: as of this morning 0.11%

- 10-Year: as of this morning 1.68%

- Increase from prior day’s trading of 1.65%

- YIELD CURVE: as of this morning 1.40

- Up from prior day’s trading at 1.38

MACRO DATA POINTS (Bloomberg Estimates)

- 8:30am: Trade Balance, June, est. -$47.5b (prior -$48.7b)

- 8:30am: Initial Jobless Claims, week Aug. 4, est. 370k (prior 365k)

- 9:45am: Bloomberg Consumer Comfort, week Aug. 5 (prior -39.7)

- 10am: Wholesale Inventories, June, est. 0.3% (prior 0.3%)

- 10am: Freddie Mac mortgage rates

- 10:30am: EIA natural gas change

- 11am: U.S. Fed to purchase $1b-$1.5b TIPS in 1/15/2019 to 2/15/2042 range

- 1pm: U.S. to sell $16b 30-year bonds

GOVERNMENT/POLITICS:

- House, Senate not in session

- NOAA updates hurricane forecast. In May agency predicted near-normal season with from nine to 15 named storms, 11am

- Board of governors of U.S. Postal Service, which on Aug. 1 skipped a required $5.5b payment to U.S. Treasury, meets to discuss third-quarter financial results, 8:30am

- CFTC meets on customer protection requirements for futures commission merchants, 9:30am

- Commerce Dept. panel meets on technical questions that affect materials, technology export controls, 10am

WHAT TO WATCH:

- Trade Deficit in U.S. Probably Narrowed in June on Cheaper Oil

- Goldman Sachs Tops Corporate Split With Obama, GE Jilts Him Too

- Apple Patent Faceoff With HTC Pivots on Dueling Pinch Videos

- Profits at Fannie Mae, Freddie Mac May Ease Wind-Down Pressure

- Standard Chartered CEO Says ‘No Grounds’ to Revoke License

- Nokia to Sell App Unit Amid Increasing Microsoft Dependence

- U.S. foreclosure filings in July fell 10%: RealtyTrac

- Restaurant operator CKE expected to price IPO after close

- Amgen Halts Pancreatic Cancer Study After Drug Fails to Work

- Manchester United seeks to raise $333m in IPO

- U.K. Goods-Trade Deficit Widens to Record as Exports Decline

- World Food Prices Jump as U.S., Russia Droughts Spark Crop Rally

- China Adds Scope to Cut Rates as Japan, S. Korea Hold

EARNINGS:

- Bombardier (BBD/B CN) 6am, $0.10

- Manulife Financial (MFC CN) 6am, C$(0.49)

- Quebecor (QBR/B CN) 6am, C$0.97

- Kohl’s (KSS) 7am, $0.96

- Metro (MRU CN) 7am, C$1.36

- Elizabeth Arden (RDEN) 7am, $0.20

- Wendy’s (WEN) 7am, $0.05

- Windstream (WIN) 7am, $0.12

- Brinker International (EAT) 7:15am, $0.58

- Tim Hortons (THI CN) 7:30am, $0.69

- Hillshire Brands Co (HSH) 7:30am, $0.38

- AMC Networks (AMCX) 8am, $0.58

- Magna International (MG CN) 8am, $1.28

- Royal Gold (RGLD) 8am, $0.44

- Canadian Tire (CTC/A CN) 8:05am, C$1.52

- Advance Auto Parts (AAP) 8:30am, $1.39

- Teekay (TK) 8:30am, $(0.45)

- Teekay Offshore Partners (TOO) 8:30am, $0.37

- Crescent Point Energy (CPG CN) 9am, C$0.07

- Kronos Worldwide (KRO) Premkt, $0.44

- ViroPharma Inc (VPHM) Premkt, $0.21

- CI Financial (CIX CN) 11:17am, $0.32

- CareFusion (CFN) 4pm, $0.49

- DeVry (DV) 4:01pm, $0.44

- Open Text (OTC CN) 4:01pm, $1.16

- Nordstrom (JWN) 4:05pm, $0.74

- Fusion-io (FIO) 4:05pm, $0.04

- NVIDIA (NVDA) 4:19pm, $0.22

- Osisko Mining (OSK CN) 4:19pm, C$0.07

- Pembina Pipeline (PPL CN) 4:30pm, C$0.31

- ShawCor (SCL/A CN) 5:01pm, C$0.35

- Silver Wheaton (SLW CN) After-mkt, $0.37

- Lions Gate Entertainment (LGF) After-mkt, $0.18

- Assured Guaranty (AGO) After-mkt, $0.52

- Arena Pharmaceuticals Inc (ARNA) After-mkt, $(0.11)

- Scotts Miracle-Gro (SMG) After-Mkt, $1.99

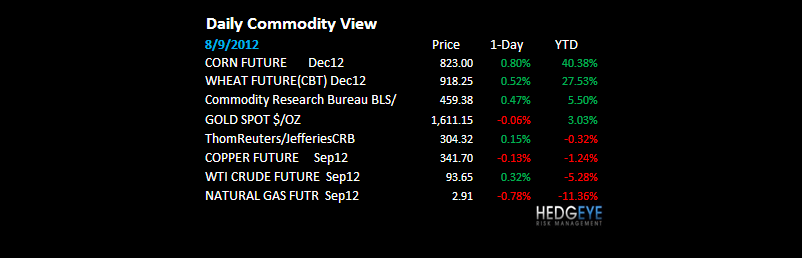

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Global Food Reserves Falling as Drought Wilts Crops: Commodities

- Iraq Oil Tops 3 Million Barrels for First Time Since 2002

- Rubber Poised for Third Surplus in 2013, Helping Bridgestone

- Oil May Retreat on Fastest Stockpiling Since ’98: Energy Markets

- World Food Prices Jump as U.S., Russia Droughts Spark Crop Rally

- Corn Advances to Record as Drought Spurs Surge in Food Costs

- Gold Seen Advancing as Slowing Growth Fuels Stimulus Optimism

- Oil Trades Near Three-Month High Amid China Stimulus Speculation

- Sugar Rises on Speculation Prices Fell Too Far; Coffee Gains

- Copper Seen Falling on Weaker-Than-Estimated Chinese Production

- Rubber Near Lowest Level in Three Years Amid Supply Surplus

- Rusal Sees Aluminum Premiums Rising for 12-18 Months on Rates

- Europe’s Sugar Producers Set to Gain as EU Faces Third Shortage

- Palladium May Stall Near $608 Before Falling: Technical Analysis

- Food Prices Surge as Droughts Spark Rally

- Palm Oil Rallies From Seven-Week Low as U.S. Set to Cut Soy Crop

- Billionaire Fredriksen’s Golar Gets Record to Store LNG at Sea

CURRENCIES

EUROPEAN MARKETS

GERMANY – again, news headlines running w/ “Europe up on China stimulus” (even though Europe is flat and Germany is down); watch the DAX here – German industrials hurting when Chinese demand continues to slow; lower-highs in the DAX from the 7154 high established in March. To get above that would require Draghi walking on water.

ASIAN MARKETS

CHINA – good thing pig prices collapsed in July, helping the Chinese print a completely random inflation reading in the face of slowing growth – bailout media took that as “another sign for stimulus”; China up a whopping +0.6%, India down on the day after missing industrial production growth too.

MIDDLE EAST

The Hedgeye Macro Team