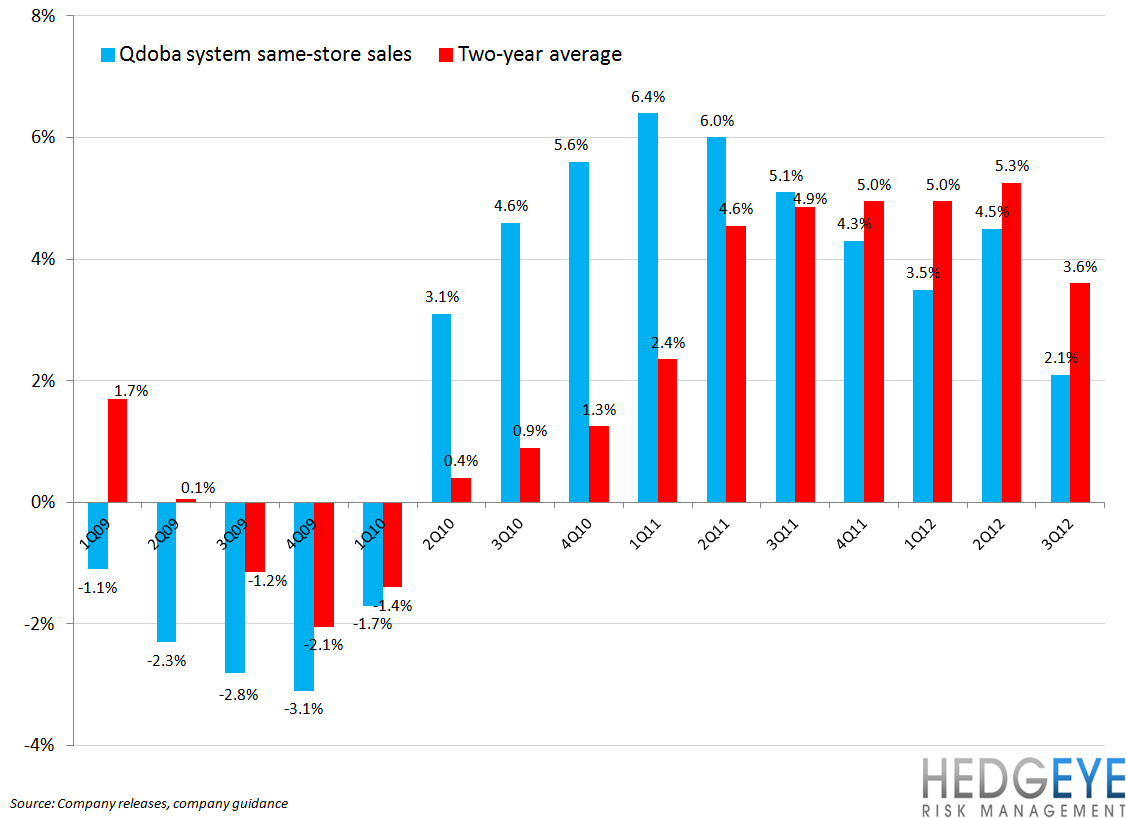

Jack in the Box reported a solid quarter, albeit one that caused confusion in after hours trading, beating EPS on an adjusted basis and raising FY12 EPS guidance. The only slight disappointment was Qdoba same-restaurant sales, particularly among the franchised locations. JACK remains one of the “cheapest” companies in the space from a valuation perspective. We expect this multiple to be revised higher over the next three years.

Restaurant level operating margins were particularly robust, increasing by 4% year-over-year. The most important news from the quarter was the company’s decision to outsource its distribution business. While there are little details about the impact on financials, our initial reaction would be positive; selling non-core assets currently used in this business will be positive for returns and margins.

During the first four weeks of 4QFY12, according to the press release, same-restaurant sales have tracked above 3Q results. For the full fiscal year 2012, management raised the mid-point of the EPS guidance range by 10% to $1.53 (consensus $1.43) on the back of higher Jack in the Box same-restaurant sales guidance slightly offset by lower Qdoba same-restaurant sales guidance.

We continue to believe that this company is well positioned to continue to produce results worthy of a higher valuation multiple as the restructuring of the company enhances future profitability, margins, and returns. At 7.2x EV/EBITDA, with EBITDA growth accelerating ahead of expectations, we believe that JACK could see 2-3 turns in multiple expansion. On this basis alone, Jack in the Box has $10-15 in upside from the current stock price.

Howard Penney

Managing Director

Rory Green

Analyst