We see Brinker as a leader in the casual dining category over the next several years as investments in technology and the introduction of new platforms should continue to differentiate Chili’s versus its most direct competitors.

We are cautious on casual dining as the group has strongly outperformed over the last year and consumer fundamentals have broken down. Our call on 4/20/12, for “CASUAL DINING CAUTION”, was ill-timed from a price perspective; despite sales trends breaking down as anticipated, management teams effectively squeezed other parts of the P&L to manufacture beats in 2Q which helped sustain the casual dining outperformance longer than we had anticipated.

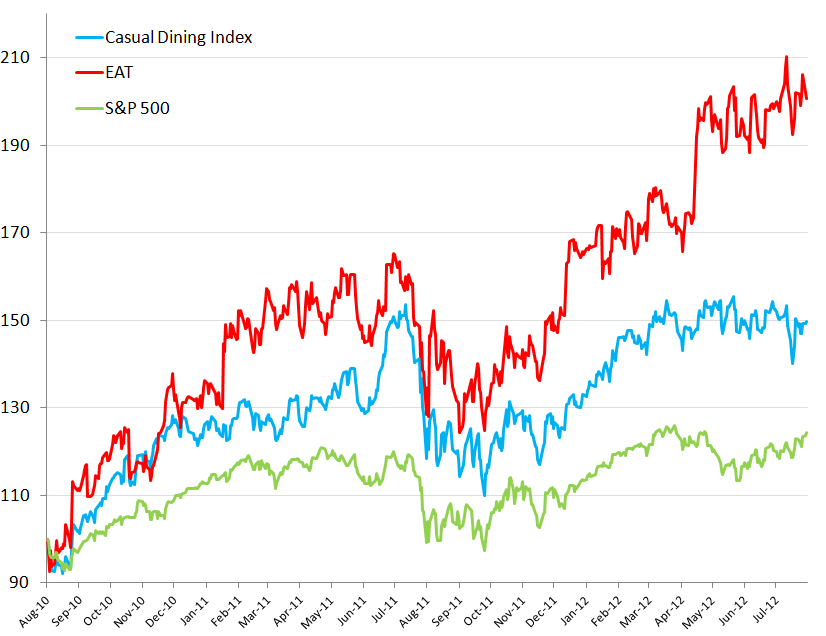

That said, we currrently favor QSR over Casual Dining at this point but strictly on a relative basis. There is one stock, within casual dining, that we do like over the intermediate-term trend: Brinker. EAT, as the chart below illustrates, has been leading the casual dining space in its outperformance but we believe that this outperformance was largely down to real market share gains and operational efficiencies achieved through investment in technology. The company’s Plan to Win is working and, we believe, constitutes a compelling reason to own the stock.

Below we present three reasons to own Brinker in to the quarter and three reasons to wait until after the event or, alternatively, stay away completely. Either way, we believe this stock presents the most attractive opportunity in casual dining on the long side.

Reasons to be long into the quarter:

The comparisons are easy from an earnings growth perspective

As the charts below illustrate, the company has been comfortably comping difficult earnings growth numbers and we expect 4QFY12 to present an easier comparison for Brinker. With Chili’s taking share from competitors, we see this aspect of the story as being a potential positive for the 4Q release.

The company is taking share from its competitors via expanded programs supported by technological investments (little incremental labor, if any)

Much of the recent concern on the bearish side of the Chili’s debate has been centered on allegedly overly aggressive cost cutting by management within the four walls. We would point out, as long-term (since 2Q10) bulls on the stock, that the bear thesis has shifted from costs to sales and back again but our confidence level is high, having taken the time to visit several different locations and understand the investment Brinker has made in the restaurant, that the market share being gained by the introduction of steak, flatbread, and other platforms, is highly accretive to earnings. Technological improvements in the Chili’s kitchen, such as the impinger oven, have allowed restaurant managers to broaden the selection of offerings available to customers without incurring significant increases in labor costs.

The stock returns a healthy yield and will likely continue to return significant levels of cash to shareholders

This stock currently carries a 2% dividend yield and management continues to buy back shares. The company’s payout ratio has been increasing and we see Chili’s, with industry-leading top-line performance, holding appeal for investors seeking dividend-yielding safety plays in the consumer space going forward. That sentence may not sit well with many investors out there that have baggage when it comes to Brinker: past management teams have disappointed investors and many cannot bring themselves to get behind the name. That’s why, despite the bullish sell-side sentiment, we think there is further room for this stock to go higher.

Reasons to wait until after the quarter/not be long the stock period:

The stock has been on a tear (see chart 1)

Brinker has been a massive outperformer over the past couple of years and this has begun to cause some concern among investors. The stock underperformed the S&P 500 by -2.1% and -2.3% over the past one-week and one-month periods, respectively. We believe that any material disappointment could be met with a decline in the share price but would be buyers of the stock for the intermediate term on any significant sell off.

Being bullish is consensus and the uncertain macro outlook could present a sizeable downside risk to the stock price

The sell-side is bullish on this name but, on a relative basis, remains more bullish on Darden and as bullish on Buffalo Wild Wings. The macro environment (particularly employment) poses a big risk to casual dining trends but we see Brinker as the strongest player in the category.

The strength in the P&L has been down to overly aggressive cost-cutting and this will catch up with the company

We have visited numerous stores in different regions of the country and are confident that the margin improvement seen at Chili’s over the last couple of years has been down to improvements in labor efficiency and store productivity on the back of, primarily, sound investment in technology in the back of the house and, secondarily, in improvements in store operations – such as team service – that have benefitted both Brinker and employees alike while providing customers with better service. The Gap-to-Knapp, which we estimate to have been 250 basis points in 3QFY12, is testament to that.

Conclusion

The most significant risk to owning this stock into earnings is mean reversion. By virtue of the strong outperformance of the stock over the last couple of years, any disappointment in sales could cause the stock to decline materially. However, we are confident that the company will continue to take share, outperform the industry benchmark, and return plenty of cash to shareholders via dividends and repurchases.

Howard Penney

Managing Director

Rory Green

Analyst