“Another thing that freaks me out is time. Time is like a book. You have a beginning, a middle and an end. It’s just a cycle.”

-Mike Tyson

This week I enjoyed a few days off in the Banff and Lake Louise region of Alberta in the heart of the Canadian Rockies. As part of my tour, I hiked up to view the Takakkaw Falls in Yoho National Park. The falls are the second highest natural falls in Canada at 245 metres. In Cree, the word Takkakaw is loosely translated to mean “it is magnificent” and is an apt description of this natural wonder.

Interestingly, while much of North American is being adversely impacted by record hot temperatures, Western Canada seems to be thriving. Specifically, the crops appear to be in excellent condition. In fact, the Canadian Wheat Board issued its first crop outlook for the 2012 – 2013 season and in it said the following:

“Wheat fundamentals are favorable to prices. World wheat production is forecast to fall by over 40 million tonnes to 646 million tonnes. A weather-related shortfall in Russia, Ukraine, and Kazakhstan is the main driver behind the global production decline. The U.S. corn belt has been hit by a severe drought, resulting in dramatic declines in corn and soybean production potential.”

We Canadians are known for our subtleness and this report from the Canadian Wheat Board is no exception. To translate: it is going to be a record year for Canadian farmers because of shortage of supply of both wheat and corn globally. This shortage of supply is primarily being supported by drought like conditions in both the U.S. and key growing areas in Europe. As a result, many agricultural commodity prices have been in a mini bull market. As an example, the corn ETF, aptly named CORN, is up more than 50% in the last two months. Being on the right side of a trade like this is what I would call: Magnificent Investing.

Personally, I haven’t studied global warming enough to either be a proponent or opponent, although this year certainly gives some credence to the concept. That said, Keith and I have at times discussed our longer term investment view of Canada and even presented this view to various municipal governments across Canada. A key component of this view is obviously the vast resources of Canada as typified by the agricultural production capabilities and the Saudi Arabia like oil resources in Alberta. But another important potential tailwind for Canada is weather patterns.

UCLA Geography Professor Laurence C. Smith has done much of the work that underscores our long term investment view of Canada. In his book, “The World in 2050: Four Forces Shaping Civilization’s Northern Future”, Smith highlights some of the key forces driving economic share gains of the Northern Rim Countries, or as he calls them NORCs. A key point in his thesis related to NORCs is that their share of crop production will increase dramatically if and when the world becomes warmer because they will be less directly impacted by an increase in temperature. His prediction is for this trend to really have an impact by 2050, even though it sounds a little like 2012 . . .

No doubt climate cycles can be challenging to invest around, though industrial cycles can be much more predictable and create longer term (in our models TAIL duration) investable fundamentals. Our recently hired Industrials Sector Head Jay Van Sciver has spent more than a decade on the buy-side and a key component of his investing framework is that if you get the industrial cycle right, you’ll get a lot of other things right. An example he uses in his presentation is being on the right side of U.S. electrical transmission infrastructure investment cycle. A couple of points to consider:

- In the down cycle from Q1 1992 to Q1 2000, the SP500 returned 243%. In that same period, the primary players in this industry, Copper Industries, Hubbell, and Thomas & Betts, returned on average 25%.

- In the up cycle from Q1 2001 to Q1 2012, when investment in transmission infrastructure was accelerating, the SP500 was up 51%. Meanwhile, the key players noted above were all up more than 300%.

I’ll say it again, if you get the cycle right, you’ll get a lot of other things right.

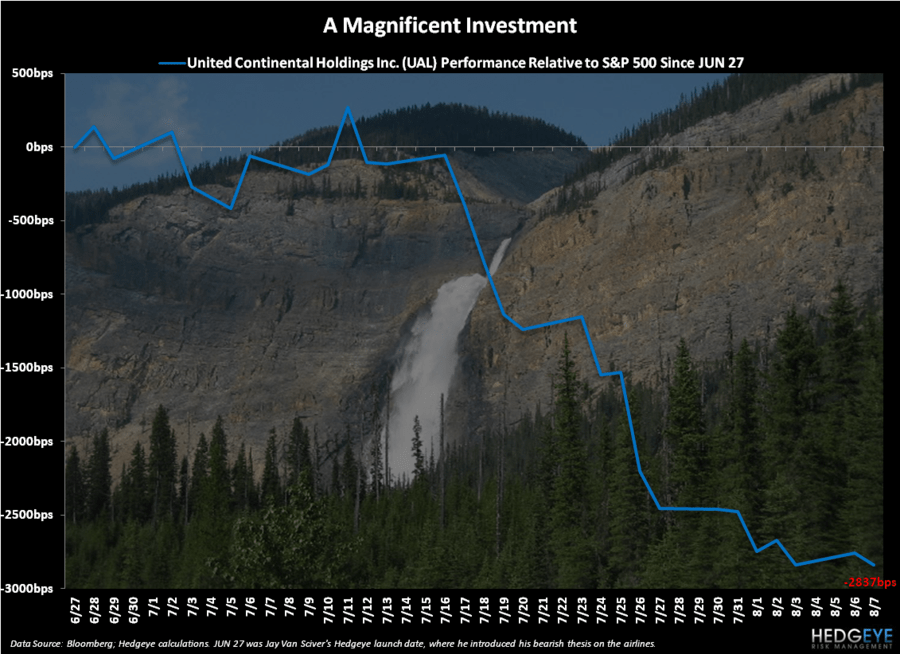

Van Sciver’s launch presentation on June 27th was a bearish call on the airline cycle. Call him lucky or good, but as we highlight in the Chart of the Day, airline stocks have basically been in free fall since he launched. In fact, speaking of Magnificent Investing, one of his least favorite names, UAL, is down almost -20% in that period. His next deep dive will be on the global truck OEM market and he will be hosting a conference call on August 16th to discuss. Ping us at or contact your sales person if you are an eligible institution and would like to join this call and review Van Sciver’s work.

In our global macro research, a key theme we’ve been hammering on for the last few years has been the global debt super cycle. An important point of this cycle is that as government debt accelerates past 90% debt-to-GDP, economic growth slows. This morning’s data from Europe does little to change our debt cycle thesis. Spanish 10-year yields are back pushing that 7% line at 6.98% and so there’s no surprise that the IBEX 35 is down -1.9%. Further, German June exports were down -1.3% year-over-year and German industrial production was down -0.3%. Clearly, even a relatively well situated country like Germany cannot escape the growth slowing debt cycle.

Our immediate-term support and resistance ranges for Gold, Oil (Brent), US Dollar, EUR/USD, and the SP500 are now $1, $107.34-111.83, $81.89-82.69, $1.23-1.24, and 1, respectively.

Keep your head up and stick on the ice,

Daryl G. Jones

Director of Research