On its last earnings call, the McDonald’s management team did not strike a positive tone, saying that “persistent unfavorable economic conditions are weighing on consumer sentiment and spending”.

We wrote on April 24th that we saw “plenty to be concerned about” regarding the outlook for McDonald’s top-line trends. Many of those concerns are persisting; weak economic conditions in Europe and the U.S. are front and center while our thesis on McDonald’s value proposition in the US weakening has not changed. The company is now pricing – at roughly 3% – in line with Food Away from Home CPI whereas last year that difference was roughly -50 basis points. Even with price of that level on the menu, we are unconvinced that traffic trends will be sufficient to bring the overall July comp in line with consensus for the U.S. division.

Macro Growth Slowing Matters

We called this out on July 20th in our 2Q preview note but it is worth posting again. We won’t be using the charts below to make month-to-month calls, but in terms of the trends that we can expect to see in McDonald’s U.S. and APMEA businesses over the next few months, it is worth referring to these charts.

Sales Preview

Below we go through what we would view as good, bad, or neutral comparable restaurant sales numbers for McDonald’s three regions. For comparison purposes, we have adjusted for historical calendar and trading day impacts (but not weather).

Compared to July 2011, July 2012 had one less Saturday, one less Friday, one additional Monday and one additional Tuesday. Ramadan starting early – impacting 10 days of July versus 0 last year – will also contribute to the shift that management has guided to as -1.8%.

U.S. – facing a compare of 4.4%, including a calendar shift of between -0.4% and +0.7%, varying by area of the world.

GOOD: A print above 2.5% would be considered a good result, as it would imply a sequential acceleration in calendar adjusted, two-year average trends. It is important to note that this would imply negative traffic but, as management noted on the 2Q12 earnings conference call, a trading day shift and the year-over-year change in the timing of Ramadan will result in the headline number understating actual business trends. We are anticipating a print of 2% for MCD U.S. comparable restaurant sales in July.

NEUTRAL: Same-restaurant sales growth of between 1.5% and 2.5% would be considered neutral by investors as it would imply calendar-adjusted two year average trends roughly level with June. While June’s trends were at (historically) trough levels, we believe that the market is expecting the underlying business in July to have fared similarly to June.

BAD: A print below 1.5% would imply a sequential deceleration in calendar-adjusted two-year average trends and could spur some analysts to further lower their FY12 EPS expectations.

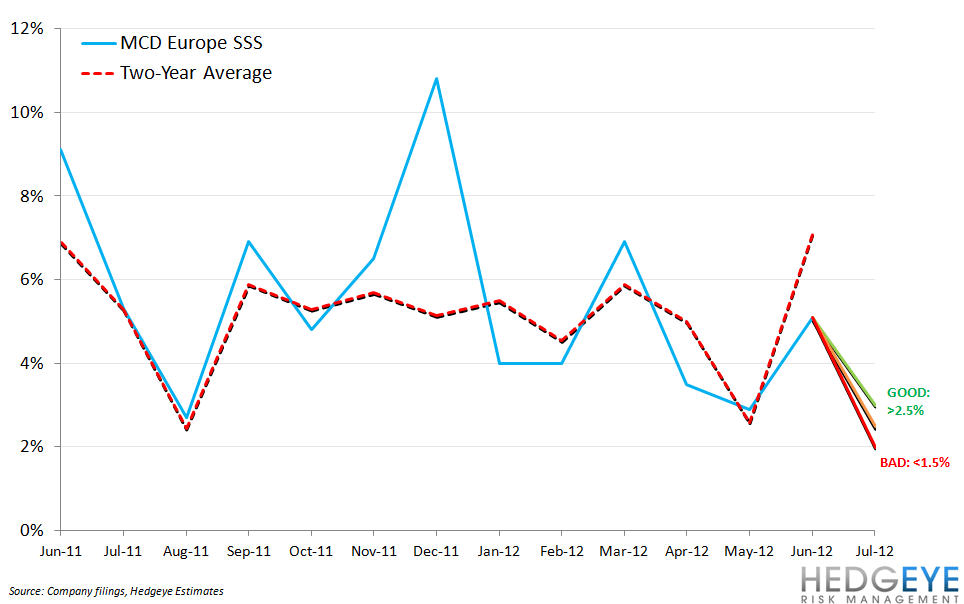

Europe – facing a compare of 5.3%, including a calendar shift of between -0.4% and +0.7%, varying by area of the world.

GOOD: A same-restaurant sales number in excess of 2.5% would be considered a strong result because it would imply, on a calendar-adjusted basis, two-year average trends roughly in line with those seen in June and above the weaker trends seen in May.

NEUTRAL: 1.5-2.5% would be a neutral result for Europe as it would imply trends roughly in line with the year-to-date average. While this is not a positive, given the commentary management provided on the earnings call on July 23rd, it seems likely July was another difficult month for MCD in Europe.

BAD: A print below 1.5% would imply a significant sequential deceleration in calendar-adjusted, two year average trends.

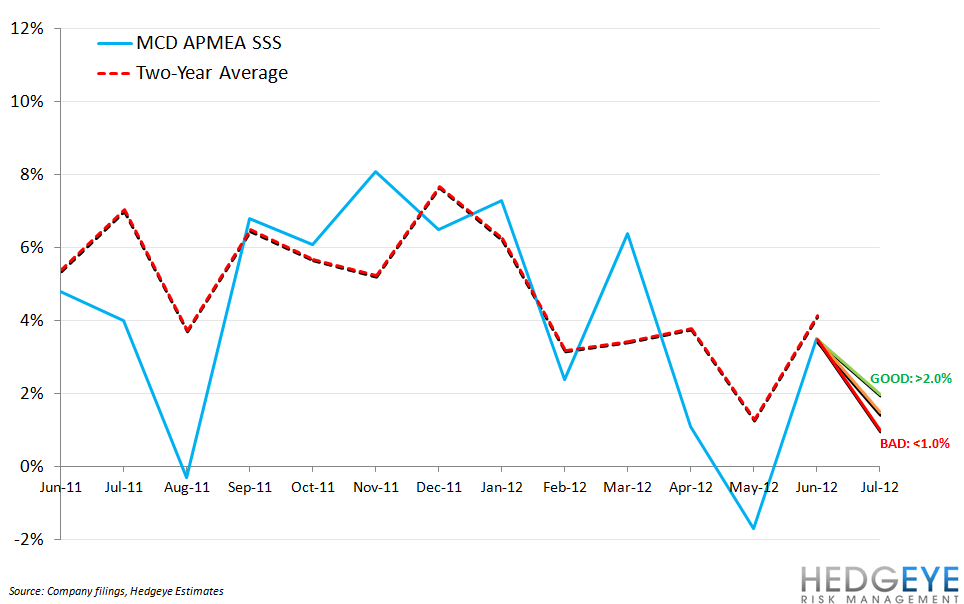

APMEA – facing a compare of 4.0%, including a calendar shift of between -0.4% and +0.7%, varying by area of the world:

GOOD: Same-restaurants sales growth of 2.0% or more would be received as a good result as it would imply a sequential acceleration in calendar-adjusted two-year average trends. On July 23rd, management cited weakness in Japan and consumer caution in China, particularly in tier-one cities where McDonald’s stores are most heavily concentrated.

NEUTRAL: A print between 1.0% and 2.0% would be considered neutral for investors as it would imply calendar-adjusted two year average trends roughly flat with June.

BAD: Below 1.0% would imply a sequential deceleration in calendar-adjusted two-year average trends from June to July. While expectations are low, at 1.56% according to Consensus Metrix, we believe that further deceleration would be a red flag for investors.

Howard Penney

Managing Director

Rory Green

Analyst