TODAY’S S&P 500 SET-UP – August 7, 2012

As we look at today’s set up for the S&P 500, the range is 34 points or -1.45% downside to 1374 and 0.99% upside to 1408.

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: on 08/06 NYSE 765

- Down versus the prior day’s trading of 1998

- VOLUME: on 08/06 NYSE 647.20

- Decrease versus prior day’s trading of -14.12%

- VIX: as of 08/06 was at 15.95

- Increase versus most recent day’s trading of 1.98%

- Year-to-date decrease of -31.84%

- SPX PUT/CALL RATIO: as of 08/06 closed at 1.54

- Up from the day prior at 1.27

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: as of this morning 36

- 3-MONTH T-BILL YIELD: as of this morning 0.08%

- 10-Year: as of this morning 1.59%

- Increase from prior day’s trading of 1.57%

- YIELD CURVE: as of this morning 1.35

- Up from prior day’s trading at 1.33

MACRO DATA POINTS (Bloomberg Estimates):

- 6am: EFSF to sell up to EU1.5b 91-day bills

- 7:45am/8:55am: ICSC/Redbook retail sales

- 10am: JOLTs Job Openings, June, est. 3717 (prior 3642)

- 11am: U.S. Fed to purchase $4.25b-$5b notes in 8/15/2018 to 5/15/2020 range

- 11:30am: U.S. to sell 4-week bills

- 1pm: U.S. to sell $32b 3-year notes

- 2:30pm: Fed’s Bernanke speaks by video on financial education in Washington

- 3pm: Consumer Credit, June, est. $10.5b (prior $17.118b, revised)

- 4:30pm: API inventories

GOVERNMENT/POLITICS:

- House, Senate meet in pro-forma sessions

- Senate Majority Leader Harry Reid, D-Nev., Center for American Progress host National Clean Energy Summit, with speakers include Interior Secretary Ken Salazar, former President Bill Clinton

- FCC Chairman Julius Genachowski, Ben Hecht, chairman of Connect2Compete announce launch of nationwide computer recycling, donation effort, 11am

WHAT TO WATCH:

- Standard Chartered plunges; faces New York suspension on Iran

- HTC extends decline to 2008 low after forecast of sales drop

- Pfizer-J&J drop Alzheimer’s drug trials after second failure

- Chesapeake posts record profit as asset-sale goals expand

- Knight Capital’s three new board members will be picked by Blackstone, General Atlantic, the board w/ Jefferies approval

- SEC freezes another $6m in Nexen insider-trading case

- Icahn seeks talks to buy remaining CVR Energy shrs, $29 ea.

- Second TSE system error in seven months halts derivatives

- Italian economy contracts for 4th straight quarter amid slump

- CFA Level III exam results due today

- Hedge funds gained 0.2% last month, trailing stocks

- U.S. CEOs less confident on economy: survey

EARNINGS:

- Emerson Electric (EMR) 6:30am, $1.00

- CVS Caremark (CVS) 6:45am, $0.80; Preview

- Church & Dwight (CHD) 7am, $0.55

- Fossil (FOSL) 7am, $0.79

- Marsh & McLennan (MMC) 7am, $0.58

- Sirius XM Radio (SIRI) 7am, $0.02

- TransDigm Group (TDG) 7am, $1.70

- MGM Resorts (MGM) 7:30am, $(0.15)

- Molson Coors Brewing (TAP) 7:30am, $1.20

- Oaktree Capital (OAK) 7:30am, $0.61

- Tenet Healthcare (THC) 7:30am, $0.05

- Pepco Holdings (POM) 7:35am, $0.31

- Melco Crown (MPEL) 7:40am, $0.17

- Brookfield Renewable Energy (BEP-U CN) 8am, $0.10

- Charter Communications (CHTR) 8am, $(0.21)

- Cablevision Systems (CVC) 8:30am, $0.19

- FirstEnergy (FE) 8:30am, $0.64

- PG&E (PCG) 9:01am, $0.82

- Primaris Retail REIT (PMZ-U CN) 4pm, C$0.36

- Rackspace Hosting (RAX) 4pm, $0.18

- TW Telecom (TWTC) 4pm, $0.14

- Priceline.com (PCLN) 4:01pm, $7.36

- XL Group (XL) 4:01pm, $0.55

- Alterra Capital Holdings (ALTE) 4:04pm, $0.58

- Live Nation Entertainment (LYV) 4:04pm, $0.06

- Express Scripts Holding (ESRX) 4:05pm, $0.82; Preview

- Walt Disney (DIS) 4:14pm, $0.93

- Energy Transfer Equity (ETE) 4:40pm, $0.38

- Energy Transfer Partners (ETP) 4:40pm, $0.46

- Renren (RENN) 5pm, $(0.04)

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

OIL – ripping humanity a new one this morning on the real (inflation adjusted) consumption growth front. At $110, Brent is up +25% since June! So get ready for every CPI and PPI report to accelerate, after they’ve deflated for the last few months; economic tailwind is now a big headwind.

- Iron-Ore Rout Seen Curbing Losses for Commodity Ships: Freight

- Rice Hoard Offers World Respite as Food Costs Surge: Commodities

- SovEcon Says Russian Wheat Harvest May Be Lower Than in 2010

- Soybeans Gain as Rains Seen Failing to Revive Drought-Hit Crop

- Barrick Gold Studies Acquiring Assets as It Reviews Costly Mines

- Chinese Smelters May Boost Copper Exports After Tolling Tax Cut

- Gold Increases on Speculation a Weaker Dollar Will Spur Demand

- Japan Seeks to Buy 106,530 Tons of Milling Wheat in Tender

- Copper Gains for Third Day Before China Inflation Data This Week

- CBH Says Western Australia Grain Shipments May Climb to Record

- Crude Supplies Fall to Three-Month Low in Survey: Energy Markets

- Palm Oil to Drop on Weak Demand, Stockpiles, TransGraph Says

- Asteroid Mining Venture Adds Google-Backed Billionaire Investors

- Richest Family Offices Seeing Fastest Growth as Firms Oust Banks

- Cotton Harvest in India to Tumble as Dry Weather Hurts Crops

- China Overtakes South Africa on Ferrochrome Output, Merafe Says

CURRENCIES

EUROPEAN MARKETS

ITALY – good news, Italy is experiencing a stagflating recession (Q2 GDP -2.5% y/y), youth unemployment just hit 36%, but “the stock market is up.” So is Venezuela’s. This short squeeze has been impressive.

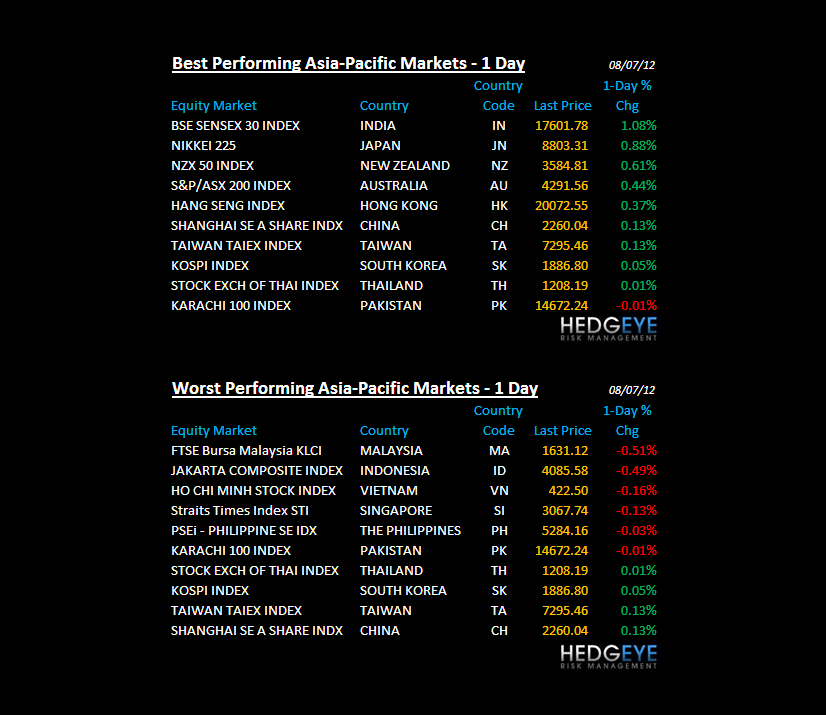

ASIAN MARKETS

ASIA – Asia’s 2-day equity rally ends on a whimper w/ China closing +0.13%, KOSPI +0.05%, and Singapore -0.14% (Japan was up +0.88%, failed right at immediate-term TRADE resistance of 8813). Where do we go from here? Australia said no more rate cuts for you. Brent Oil at $110 is not good for whatever is left of Eastern consumption growth.

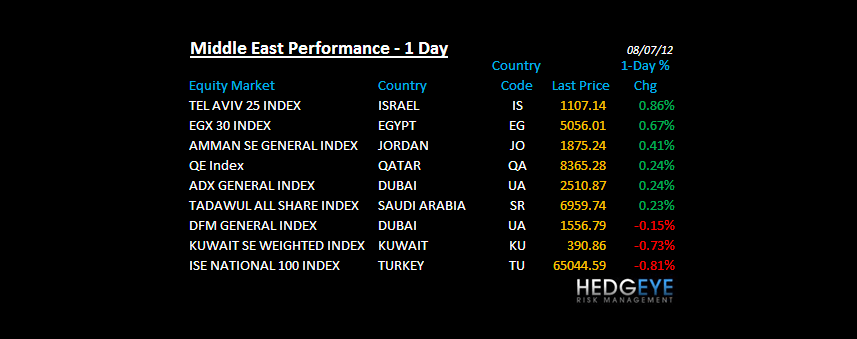

MIDDLE EAST

The Hedgeye Macro Team