“Your father doesn’t believe in magic.”

-Elinor

This weekend I took my son Jack to Pixar’s latest animation, “Brave.” The original story, set in the 10th century Scottish highlands, was called “The Bear and The Bow.” Since the McCullough Clan genuinely loves bears, we thoroughly enjoyed the movie.

Brave’s King Fergus doesn’t like bears anymore than modern day Eurocrats do. In fact, the King’s entire life is centered around fighting one demon bear in particular by the name of “Mor’du.”

I won’t ruin this European short squeeze (or the rest of the movie for you), but having gone to French Canadian school until the 5th grade, I must give you a hint – “mordu”, en Francais, is the past participle of “death.”

Back to the Global Macro Grind…

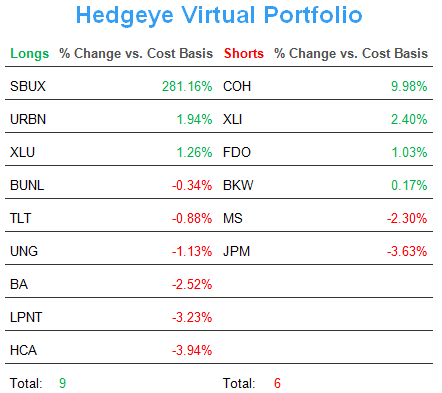

No worries, no short sellers from New Haven, CT actually died in Friday’s latest no-volume squeeze (we cut the SHORTS in the Hedgeye Portfolio to only 5 by Friday morning). Evidently, neither did as many people perish in the government’s now infamous “birth/death adjustment” for US payrolls.

In today’s Chart of the Day, Darius Dale contextualizes the July 2012 Jobs Report with a picture that nets out the effects of the NSA’s “birth/death adjustment” from the NSA Non-Farm Payroll month-over-month figure.

In addition to that picture telling you 1,000 words, here are some other quick hits on the jobs report:

- For June (last month’s report), the government revised non-farm payrolls down to 64,000 vs 80,000 prior

- For July, the “birth/death adjustment” of +52,000 jobs was the highest “adjustment” on record (since July 2000)

- For July, the actual unemployment rate ticked up +10bps (month-over-month) vs June to a very elevated 8.3%

But, but… provided that you believe in magic during an Election Year, America’s jobs crisis is over and it’s time to buy stocks with both hands at VIX 15, again. *Note, every time you’ve bought US Equities at VIX 14-15, in the last 5 years, you’ve been killed.

Killing the shorts is cool, until it isn’t. Don’t forget that short covering is one of the only ways left for these markets to go up. Inflows into US Equities remain dead. So is trust.

While it was funny to see the perma-bulls of the manic media blame Europe for the April-June US stock market declines, I don’t see too many of these cats championing Europe as the reason for a US stock market rally. #weird

Looking at the short squeezes we’ve seen off the June 2012 lows, here are some noteworthy ones:

- Oil (Brent) = +23%

- EuroStoxx50 Index = +15%

- SP500 = +8.7%

Centrally planned black magic or not, Americans of the 30th Olympiad better be thanking Europe for hosting one mother of a short squeeze in commodity and stock prices, even if the volume of fans is low.

The commodity side of this Reflation Rally to lower-highs is worth wasting a few more bullets on:

- CFTC (US Commodities Futures Trading Commission) contracts ripped another +5% wk-over-wk to 1.22 million contracts

- Agricultural bets (net long contracts) were up another +3% wk-over-wk at a new high of 884,477 contracts

- Gold bets put on their biggest wk-over-wk move (+36%) since November of 2008 (96,200 contracts)

Got Inflation Expectations? Brooksley Born, do you hear her now?

How about causality (central planning policies) and correlation (US Dollar Correlation Risk to stock and commodity prices)? Yep, Obama and Axelrod understand this full well. So did Bush and Bernanke. If you want commodity and stock market inflations to re-flate those political chances, you just need to spend like mad and debauch that US Dollar.

With the US Dollar down another -0.4% last week (down for 2 consecutive weeks), this keeps Oil (and Energy stocks) leading the latest charge. Oh, wait. The US stock market is down 8 of the last 11 days, and the Russell2000 was down another 1% last week…

So you better be either a Brave Bear when covering those shorts on Thursdays, or just get right loaded to the gills in commodity leverage and, at the same time, say there’s no inflation at the pump. Jack’s Dad tells him magical fairy tales at bedtime too.

My immediate-term support and resistance ranges for Gold, Oil (Brent), US Dollar, EUR/USD, Russell2000, and the SP500 are now $1, $106.05-110.84, $82.06-82.95, $1.20-1.23, 779-791, and 1, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer